- Introduction

- The Origins of Press Note 3: A Pandemic-Era Protective Shield

- Expert Insight

- The New Beneficial Ownership Framework: The Three-Tiered Test

- The Aggregation Rule: Collective LBC Exposure Cannot Be Fragmented

- The Look-Through Approach: Seeing Beyond the Immediate Investor

- The Missing 60-Day Timeline: A Gap Between Policy Indication and Legal Reality

- Additional Reporting Requirements: A New Compliance Laye

- Implications for Start-Ups, Private Equity, and Manufacturing

- The Law Commission of India's Perspective on FDI Screening

- Key Snippets

- Conclusion

Frequently asked questions (FAQs)

1.Introduction

Foreign Direct Investment (FDI) is one of the most powerful engines of economic growth in any developing nation. For India, building a credible, clear, and investor-friendly FDI regulatory framework has been a long-standing policy priority. However, since April 2020, a particular subset of FDI rules has remained a persistent source of regulatory strain, transactional delays, and investor hesitation. That subset is governed by Press Note 3 of 2020 (referred to hereafter as "PN3"), which was introduced by the Department for Promotion of Industry and Internal Trade (DPIIT) to regulate investments from countries sharing a land border with India, commonly referred to as Land Border Countries or "LBCs."

PN3 was born out of extraordinary circumstances. The COVID-19 pandemic had created widespread economic distress, and the Indian government was concerned that foreign investors, particularly from China, might exploit weakened valuations to acquire Indian companies in a predatory manner. The intent was protective and timely. However, the policy was broadly worded, left critical terms undefined, and ended up casting a wider net than anticipated. Over the subsequent five years, transactions worth thousands of crores of rupees were delayed or abandoned simply because neither investors nor authorised dealer banks could clearly determine what "beneficial ownership" meant under PN3.

The long-awaited clarification appears to have arrived in March 2026. The Union Cabinet approved proposed amendments to PN3 on March 10, 2026, and the DPIIT formally notified these changes through Press Note No. 2 of the 2026 Series (referred to hereafter as "PN2/2026") on March 15, 2026. As per these recent policy developments, the amendments seek to amend Paragraph 3.1.1 of the Consolidated FDI Policy, 2020, and appear to introduce a formal, PMLA-anchored definition of beneficial ownership, create a threshold-based automatic route for non-controlling LBC investments, and establish reporting requirements for investments that proceed without prior government approval. It bears noting, however, that the corresponding amendment to the Foreign Exchange Management

(Non-Debt Instruments) Rules, 2019 remains pending, and PN2/2026 will attain full statutory effect only upon such notification.

This article provides a comprehensive analysis of the legal changes notified by PN2/2026, the background context of PN3, the new three-tiered beneficial ownership test, aggregation and look-through considerations, the significant gap regarding the 60-day approval timeline, and the implications of these developments for investors, startups, funds, and manufacturing companies. The article also presents the perspective of the Law Commission of India in relation to the broader FDI regulatory framework and concludes with key takeaways and frequently asked questions. This article adopts a doctrinal and policy-analysis approach, examining the interplay between announced regulatory intent and the current state of applicable law.

2.The Origins of Press Note 3: A Pandemic-Era Protective Shield

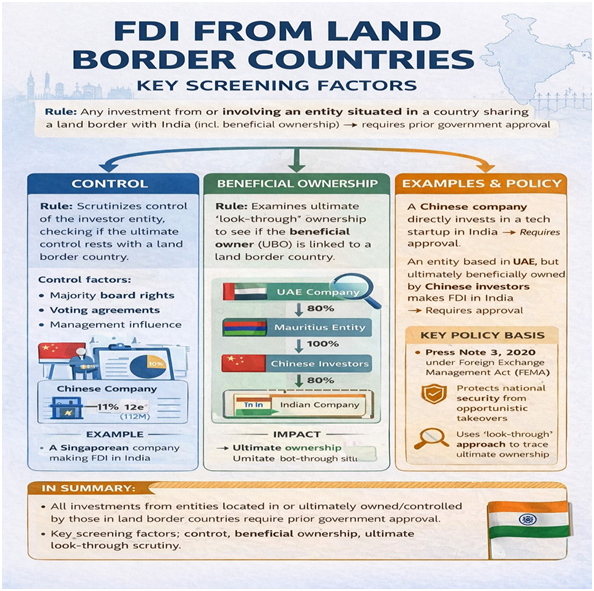

To understand why PN2/2026 matters, it is essential to appreciate the environment in which PN3 was introduced and the operational challenges it later created. In April 2020, India was dealing with the dual shock of the COVID-19 pandemic and heightened border tensions following the Galwan Valley standoff with China. In response, the government issued PN3, mandating that any investment from countries sharing a land border with India (LBCs) would require prior government approval across all sectors. These LBCs included China (along with Hong Kong and Macau), Pakistan, Bangladesh, Nepal, Bhutan, Myanmar, and Afghanistan.

Before PN3, only investments from Bangladesh and Pakistan required approval, while others, including China, could invest through the automatic route where permitted. PN3 fundamentally altered this regime by placing all LBC investments under the government approval route. It introduced two key triggers: first, where the investing entity itself was based in an LBC; and second,where the “beneficial owner” of an investment was situated in or a citizen of an LBC. The second trigger proved far more contentious due to the absence of a clear definition of “beneficial ownership.” This lack of clarity forced market participants lawyers, banks, investment bankers, and compliance teams to rely on interpretations from other statutes, such as the Significant Beneficial Ownership rules under the Companies Act, 2013, or the PML Rules, 2005. The result was regulatory inconsistency, with different Authorised Dealer Banks applying varying thresholds. Consequently, cross-border transactions involving even minimal LBC linkages faced delays and heightened scrutiny, often exceeding the intended scope of the policy. Media reports from 2024 highlight that out of 526 FDI proposals under PN3, only 124 were approved while 201 were rejected, with many still pending indicating a clear bottleneck and a chilling effect on investment flows.

India’s Economic Survey 2023–24 further underscored this impact, noting that FDI from China constituted just 0.37% of total inflows between April 2000 and March 2024. This suggests that while PN3 was driven by legitimate security concerns, its implementation may have produced unintended economic consequences in several cases.

For further reference on India's broader FDI framework, see the Foreign Exchange Management Act, 1999 , which governs all cross-border capital flows and forms the statutory bedrock of FDI regulation in India.

3.Expert Insight

As senior practitioners and scholars in the FDI advisory space have consistently noted, the absence of a defined beneficial ownership threshold under PN3 was perhaps its most consequential structural flaw. A policy designed to screen out genuinely risky investments inadvertently captured passive, non-strategic investors whose participation posed no credible national security concern. The alignment of the beneficial ownership criteria with the PMLA framework as indicated through PN2/2026 reflects a recalibration that the legal community had long advocated. The PMLA-based threshold provides not only definitional clarity but also coherence with India's anti-money laundering architecture, which has been internationally benchmarked and domestically interpreted by regulators and courts over nearly two decades. It represents a rational convergence of two regulatory systems that had, until now, operated in parallel but without cross-reference.

Furthermore, the apparent introduction of an aggregation rule requiring that shareholdings of all LBC citizens and entities be clubbed together irrespective of whether they are acting in concert reflects a legally sophisticated measure designed to preempt structured circumvention. This approach is consistent with the foundational principle of Indian corporate law that regulatory analysis must look through form to substance.

4.The New Beneficial Ownership Framework: The Three-Tiered Test

The most significant policy development notified through PN2/2026 is the introduction of a structured, three-tiered test for determining whether the beneficial ownership of an investment into India is to be treated as vesting in an LBC. This test is anchored in Section 2(1)(fa) of the Prevention of Money Laundering Act, 2002 and Rule 9(3) of the PML Rules.

As per PN2/2026, beneficial ownership is understood to vest in a Land Bordering Country (LBC) where a citizen of an LBC, or an entity incorporated or registered in an LBC, has the ability to hold rights or entitlements directly or indirectly, individually or cumulatively, and whether acting alone or

in concert through three identified mechanisms. First, the quantitative limb applies where such a person holds rights exceeding the thresholds prescribed under Rule 9(3) of the PML Rules in an investor entity incorporated outside an LBC. For companies, this generally means ownership of more than 10% of shares, capital, or profits, with different benchmarks for partnerships and trusts; crucially, this test is applied at the level of the investing entity rather than the Indian investee company.

Second, the qualitative control limb captures situations where, even below the numerical threshold, the LBC-linked person possesses rights enabling control over the investor entity. This includes board nomination rights, veto powers over key decisions, or similar governance rights that effectively confer control, thereby triggering the approval requirement despite limited shareholding. Third, the look-through limb extends the analysis further by examining whether such rights enable ultimate effective control over the Indian investee entity, requiring a holistic assessment across the ownership chain.

Collectively, this three-tiered framework marks a significant improvement over the earlier regime by introducing structured criteria for determining LBC exposure. However, while the first limb is largely objective, the latter two involve interpretative judgment, placing greater responsibility on investors, advisors, and regulators to carefully evaluate control dynamics and ensure compliance.

5.The Aggregation Rule: Collective LBC Exposure Cannot Be Fragmented

One of the most practically significant features of PN2/2026 is the apparent introduction of an explicit aggregation rule. The policy indicates that for the purpose of applying the quantitative threshold under the first limb of the three-tiered test, all shareholding held by LBC citizens and LBC entities in the investing entity must be aggregated even where those LBC persons are entirely unrelated to each other and are not acting in concert.

This has direct and material implications for fund-based investment structures. Consider an offshore private equity fund incorporated in Singapore with ten limited partners drawn from various jurisdictions. If two of those limited partners happen to be Chinese nationals citizens of an LBC and their combined holding in the fund exceeds 10%, the fund's investment in India would be treated as having LBC beneficial ownership exceeding the threshold. This remains the case even if those two Chinese investors have no relationship with each other and no active role in the fund's management or investment decisions.

The aggregation approach is designed to prevent circumvention of the beneficial ownership rules through deliberate fragmentation of LBC interests across multiple unrelated persons. It is consistent with the broader policy objective of ensuring that no LBC entity or citizen can exercise influence over Indian companies through structural dispersion.

In practice, this rule carries significant compliance implications for global institutional investors. Many large global funds routinely include participation from investors across multiple jurisdictions, including LBCs. Such funds will now need to conduct detailed analysis of their limited partner composition and maintain updated records of the same before making or expanding investments in India.

6.The Look-Through Approach: Seeing Beyond the Immediate Investor

The third limb of the beneficial ownership test introduces what practitioners have begun to describe as the "look-through approach." PN2/2026 indicates that LBC exposure at any level of the ownership chain not only at the level of the immediate investor may attract the government approval requirement.

This has direct implications for multi-layered investment structures. An investment vehicle incorporated in Mauritius, Luxembourg, or Singapore may not itself be an LBC entity. However, if the ultimate beneficial owners of that vehicle include LBC citizens or entities with the ability to exercise ultimate effective control, the investment into India may still fall under the government approval route as per the notified framework.

The phrase "ultimate effective control" is drawn from the PMLA framework, where it has been interpreted by regulators to mean the ability to exercise dominant influence over the management or policies of an entity. Significantly, such control need not be exercised through formal equity ownership alone contractual arrangements, side letters, shareholder agreements, and informal mechanisms have all been recognized as potential conduits of effective control.

For investors operating through regional financial hubs such as Singapore and Hong Kong the latter itself being an LBC this look-through analysis adds a layer of structural complexity. It requires examination not only of the formal ownership chart but also of the substantive governance arrangements at every level of the investment structure, a task that demands both legal precision and factual diligence.

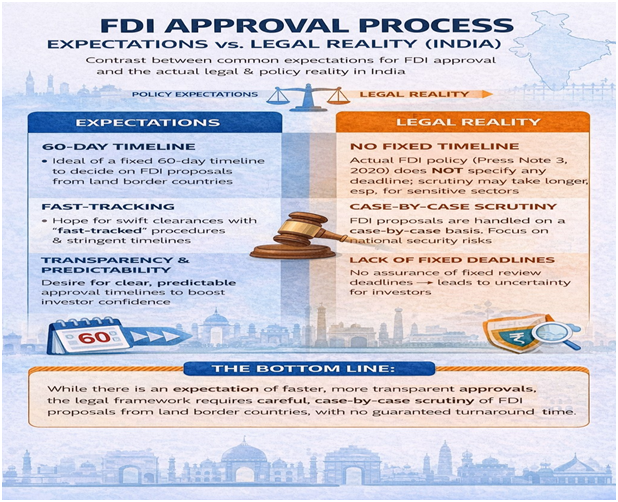

7.The Missing 60-Day Timeline: A Gap Between Policy Indication and Legal Reality

One of the most notable divergences between the Union Cabinet's press release dated March 10, 2026, and the text of PN2/2026 as notified by the DPIIT is the absence of any reference to a 60-day expedited approval timeline.

The Cabinet's press release had indicated that investment proposals from LBCs for companies engaged in specified priority manufacturing sectors would be processed and decided within 60 days. The sectors identified for this expedited treatment include capital goods manufacturing, electronic capital goods, electronic components, and polysilicon and ingot-wafer manufacturing. This announcement was widely seen as a signal of the government's intent to actively facilitate LBC investment in strategic manufacturing.

However, this 60-day commitment has not been incorporated into the formal text of PN2/2026. As it stands, until such a commitment is formally adopted whether through an amendment to the FEMA (Non-Debt Instruments) Rules, 2019 or through a revised Standard Operating Procedure (SOP) the 60-day timeline remains a policy indication rather than a binding legal obligation enforceable by investors.

This gap is worth flagging clearly. Investors in the manufacturing sector who have relied on the Cabinet's announcement as a basis for structuring timelines should exercise caution until the commitment attains formal legal status. The government's broader credibility on ease of doing business reform will be tested, in part, by how promptly this policy direction is translated into a legally operative framework.

Separately, the FEMA amendment required to give full statutory effect to PN2/2026 itself remains pending. Until the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 are formally amended, the beneficial ownership framework notified by PN2/2026 has policy authority but not yet complete statutory force. Market practice has begun aligning with its provisions, but legal certainty will require the pending FEMA notification.

For reference, the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 form the operational backbone of India's FDI regulatory framework and must be amended to give full statutory effect to the policy changes introduced by PN2/2026.

8.Additional Reporting Requirements: A New Compliance Layer

Even for investments that appear to qualify for the automatic route under the new beneficial ownership framework that is, where LBC beneficial ownership does not exceed the prescribed thresholds and does not involve control PN2/2026 introduces an additional reporting obligation.

As per the notified policy, investee Indian entities will be required to report to the DPIIT any investment involving any direct or indirect ownership by a citizen or entity of an LBC, even where that ownership is non-controlling and sub-threshold. This creates what may be described as a post-transaction monitoring regime a mechanism through which the government retains regulatory visibility over all FDI with LBC linkage, even that which does not require prior approval.

For institutional investors and fund managers, this development carries an important practical implication: the composition of their investor base including the identity and nationality of limited partners may become more transparent to Indian regulators through the reporting chain, regardless of whether government approval was sought or required for the transaction itself.

The existing SOP dated August 17, 2023, was designed to govern investments requiring government approval and does not currently address this new category of automatic route reporting. The DPIIT will need to issue revised or supplementary guidance including the format, timelines, and channel for such reporting before the monitoring regime can function in practice. AD Banks will correspondingly require operational guidance on how to treat these disclosures at the transaction level.

9.Implications for Start-Ups, Private Equity, and Manufacturing

The practical significance of PN2/2026 varies considerably depending on the type of investor and the nature of the transaction.

For start-ups and early-stage companies, the policy developments are broadly constructive. Global venture capital and private equity funds that had minor, passive LBC-linked limited partners were frequently unable to invest in Indian start-ups under PN3, even where those LPs exercised no operational role whatsoever. Under the framework as indicated by PN2/2026, if the aggregate LBC beneficial ownership in such funds does not exceed the prescribed PMLA threshold and does not involve control, the funds may invest under the automatic route. This is expected to unlock a meaningful pipeline of investment for Indian start-ups and deep-tech ventures that were previously inaccessible to such funds a direct benefit to India's innovation ecosystem.

For large M&A transactions and manufacturing joint ventures, the assessment is more nuanced. The three-tiered test particularly the qualitative control and ultimate effective control limbs requires parties to conduct granular legal analysis of their investment structures before committing to transactions. Governance rights that may appear routine in other cross-border contexts such as veto rights over significant capital expenditure, or the right to appoint a minority director to the board could trigger the government approval requirement under the PN2/2026 framework.

For Chinese investors and companies directly seeking to enter India, PN2/2026 signals a measured and calibrated opening. The government has indicated its willingness to consider LBC investments in priority manufacturing sectors, particularly where such investments support the objectives of Atmanirbhar Bharat and global supply chain integration. The approval route, however, remains the default for any LBC entity investing directly in India, and the substantive screening mechanisms embedded in the three-tiered test ensure that meaningful regulatory oversight is preserved.

10.The Law Commission of India's Perspective on FDI Screening

The Law Commission of India has, across successive reports addressing foreign investment, commercial law reform, and regulatory governance, consistently articulated a clear position: India's investment screening framework must achieve a workable equilibrium between encouraging foreign capital inflows and protecting the nation's economic sovereignty and strategic interests. The Commission has repeatedly identified regulatory ambiguity as a structural impediment to investment not merely an inconvenience, but a substantive non-tariff barrier that undermines India's positioning as a predictable destination for long-term capital.

In the specific context of PN3 and frameworks of its kind, the Law Commission's jurisprudential approach supports the view that any restriction on FDI must satisfy three conditions: it must be grounded in a clear and publicly accessible legal standard; it must be proportionate to the identified national security or economic risk; and it must be administered through a transparent process with defined and enforceable timelines. The absence of a beneficial ownership definition in PN3 was precisely the kind of drafting gap that the Commission has historically flagged not because restrictions on LBC investment are per se unjustified, but because restrictions without definitional clarity breed legal uncertainty, invite inconsistent implementation, and penalize legitimate investment that was never meant to be caught.

The alignment of the beneficial ownership definition with the PMLA framework, as indicated by PN2/2026, is consistent with the Law Commission's longstanding recommendation that definitional concepts should be harmonized across statutory regimes wherever feasible. Employing a common definition of "beneficial owner" for both FDI screening and anti-money laundering purposes reduces compliance complexity, promotes regulatory coherence across government departments, and strengthens the framework's resilience to legal challenge.

The Law Commission has also, in its broader work on commercial law reform, flagged the desirability of India developing a more sophisticated and sector-differentiated investment screening architecture one potentially drawing on comparative models such as the Committee on Foreign Investment in the United States (CFIUS), which evaluates inbound FDI specifically on national security grounds with defined statutory criteria. PN2/2026, with its threshold-based approach and qualitative control analysis, moves meaningfully in that direction. Substantial institutional and legislative work, however, remains before India can be said to possess a CFIUS-equivalent framework with equivalent legal authority, enforcement teeth, and procedural certainty.

11.Key Snippets

The following are the five most important takeaways from this article for quick reference:

a.PN2/2026 appears to formally define "beneficial ownership" under India's FDI framework for the first time, aligning it with Section 2(1)(fa) of the PMLA and Rule 9(3) of the PML Rules a development that, once backed by the pending FEMA amendment, would bring regulatory clarity after five years of definitional gaps under PN3.

b.The notified framework introduces a three-tiered test for beneficial ownership a quantitative threshold limb (10%), a control-over-investor limb, and an ultimate effective control over investee limb making the analysis more rigorous and more substantive than a simple ownership percentage.

c.Investments with non-controlling LBC beneficial ownership not exceeding the applicable PMLA thresholds may now proceed through the automatic route, subject to new reporting obligations to DPIIT a significant development for global PE and VC funds carrying passive LBC limited partner exposure.

d.The aggregation rule requires the cumulative clubbing of all LBC citizens' and entities' shareholding when assessing the beneficial ownership threshold irrespective of whether those LBC persons are related or acting in concert a provision that prevents fragmentation-based circumvention of the ownership rules.

e.The 60-day expedited approval timeline indicated in the Cabinet's press release has not been incorporated into the formal text of PN2/2026 and currently remains a policy direction without binding legal force, pending formal amendment to the FEMA NDI Rules.

12.Conclusion

India's FDI regulatory framework for land border countries has undergone a meaningful policy reset through PN2/2026. For the better part of six years, the absence of a defined "beneficial ownership" standard under PN3 created a compliance environment in which even benign, minority, and entirely passive investments were subjected to procedural delays and regulatory uncertainty. PN2/2026 addresses this by anchoring the beneficial ownership concept to the PMLA framework, introducing a threshold-based three-tiered analytical test, and creating a conditional pathway for non-controlling LBC investments to proceed through the automatic route.

At the same time, the framework as notified does not constitute a wholesale liberalization of India's FDI policy toward LBCs. The qualitative control limbs of the beneficial ownership test, the aggregation rule, and the look-through approach collectively ensure that the government retains substantive oversight over investments carrying material LBC influence. The new reporting requirements for automatic route transactions add a post-transaction monitoring dimension that preserves regulatory visibility across the full spectrum of LBC-linked FDI.

The two most significant pending gaps the absence of the 60-day timeline in the formal policy text, and the outstanding FEMA NDI Rules amendment require urgent legislative attention. Investor confidence is not built on policy announcements alone; it is built on the alignment between announced intent and enforceable law. The government's credibility on regulatory reform will be measured by how swiftly these gaps are closed.

For the Indian legal and business community, PN2/2026 when read alongside the pending FEMA amendment indicates an important step toward a more calibrated and analytically grounded FDI screening regime: one that draws meaningful distinctions between controlling and non-controlling investments, between direct and indirect exposure, and between the need for prior regulatory approval and post-transaction visibility. As the Law Commission and leading practitioners have long emphasized, the objective must be a framework that is simultaneously predictable, proportionate, and resistant to misuse. PN2/2026 advances that objective in a meaningful direction. India stands at a regulatory inflection point one where the quality of implementation and legislative follow-through will determine whether this policy reset translates into lasting investor confidence or remains a work in progress.

Frequently Asked Questions (FAQs)

1.What is Press Note 3 of 2020, and why was it introduced?

Press Note 3 of 2020 was issued by the DPIIT on April 17, 2020, as an amendment to India's Consolidated FDI Policy. It made prior government approval mandatory for all FDI from countries sharing a land border with India including China, Pakistan, Bangladesh, Nepal, Myanmar, Bhutan, and Afghanistan. It was introduced to prevent opportunistic takeovers of Indian companies during the economic vulnerability caused by the COVID-19 pandemic, with a particular focus on concerns about the acquisition of distressed Indian assets by investors from neighbouring countries.

2.What is Press Note 2 of 2026, and how does it seek to change PN3?

Press Note 2 of 2026 (PN2/2026), notified by the DPIIT on March 15, 2026, amends Paragraph 3.1.1 of the Consolidated FDI Policy, 2020. As per recent policy developments, it introduces a formal definition of "beneficial ownership" aligned with the PMLA, creates a three-tiered test for determining LBC beneficial ownership, indicates that non-controlling LBC investments below the 10% threshold may proceed under the automatic route, introduces aggregation and look-through obligations, and establishes reporting requirements for automatic route investments with LBC exposure. It is important to note that full statutory effect will follow only upon the pending amendment to the FEMA (Non-Debt Instruments) Rules, 2019.

3.What is the significance of aligning beneficial ownership with the PMLA framework?

The PMLA framework particularly Section 2(1)(fa) and Rule 9(3) of the PML Rules provides a well-established and judicially interpreted legal standard for determining who ultimately owns or controls an entity. Anchoring PN3's beneficial ownership concept to this framework eliminates the definitional vacuum that had existed since 2020, ensures consistency between India's FDI screening and anti-money laundering architecture, and provides a clear quantitative threshold 10% for companies that market participants can practically apply in structuring and compliance analysis.

4.Can a global private equity fund with some Chinese limited partners now invest in India under the automatic route?

Potentially, yes subject to careful analysis. If the combined shareholding of all LBC citizens and entities in the fund does not exceed the applicable PMLA threshold, and if such LBC investors do not hold governance rights amounting to control over the fund or the Indian investee entity, the investment may proceed under the automatic route as per the notified framework. However, the aggregation rule requires that all LBC-linked holdings be clubbed together regardless of any relationship between those investors. The qualitative control limbs of the three-tiered test must also be satisfied. Specific legal advice on the fund's structure is strongly recommended before relying on the automatic route.

5.What is the 60-day approval timeline, and why does it matter?

The Cabinet's press release of March 10, 2026, indicated that investment proposals from LBCs in specified priority manufacturing sectors including capital goods, electronic capital goods, electronic components, and polysilicon and ingot-wafer manufacturing would be processed within 60 days. This was intended to signal regulatory intent to facilitate LBC investment in strategic manufacturing. However, this timeline has not been incorporated into the formal text of PN2/2026 and does not presently carry binding legal force. It remains a policy direction, and investors should not rely on it as a guaranteed procedural entitlement until it is formally adopted through FEMA NDI Rules or an updated SOP.

6.Are Pakistani investors treated differently under the new framework?

Yes. Pakistan and Afghanistan are subject to heightened and distinct restrictions. Pakistani investors remain confined to investments in non-sensitive sectors and must in all cases proceed through the government approval route. The conditional liberalization introduced through PN2/2026 particularly the indicated automatic route for non-controlling sub-threshold investments operates in the general LBC context and does not reduce the specific and more stringent restrictions applicable to Pakistani and Afghan investors.

7.What are the new reporting obligations introduced by PN2/2026?

PN2/2026 introduces a requirement that investee Indian entities report to DPIIT all investments involving any direct or indirect ownership by a citizen or entity of an LBC even where such investments qualify for the automatic route and do not require prior government approval. This creates a post-transaction monitoring regime ensuring that all LBC-linked FDI remains within the government's regulatory visibility. The specific format, timelines, and operational process for such reporting are yet to be prescribed by the DPIIT, and revisions to the existing SOP dated August 17, 2023, are anticipated.

Click here to download the original copy of the Files

Click here to download the original copy of the Files

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others