INTRODUCTION

The corporate architecture of a developing market economy depends heavily on its capacity to efficiently mobilize, allocate, and regulate capital. Under Indian corporate jurisprudence, a company’s share capital serves as its financial lifeblood, providing the essential resources required to fuel industrial expansion, technological innovation, and commercial scale. However, the accumulation of capital from public and private streams creates an inherent asymmetry of power within the corporate ecosystem. While corporate promoters and managers possess direct control over the deployment of pooled funds and access to real-time operational data, individual investors particularly retail minority shareholders occupy a vulnerable position, separated from daily administration and exposed to the risks of managerial misconduct, asset diversion, and market manipulation.

Consequently, the evolution of Indian company law has been fundamentally driven by the dual objective of facilitating seamless capital formation while erecting unyielding legal barriers to protect investor interests. The historical landscape of the Indian capital market is dotted with structural transformations, moving from the restrictive, pre-liberalization era of the Controller of Capital Issues (CCI) to the modern, market-driven regime established under the Companies Act, 2013. Share capital regulation is no longer viewed merely as an internal administrative matter of a company; it is recognized as a vital pillar of macroeconomic stability and market integrity. This research paper provides a comprehensive legal and economic analysis of share capital regulation under Indian company law, examining how statutory provisions, institutional checks, and regulatory oversight interlock to maintain investor confidence and ensure a fair, transparent capital market.

CONCEPTUAL FRAMEWORK OF SHARE CAPITAL

In corporate jurisprudence, share capital represents the total amount of capital that a company is contractually and legally authorized to raise from investors through the issuance of shares. A share itself is not a physical piece of property, but a bundle of abstract legal rights and obligations; as classically defined in Indian judicial precedent, it represents an undivided monetary interest in the company’s enterprise, measured by a sum of money for the purpose of liability and dividend, and accompanied by a series of statutory covenants. The Companies Act, 2013 establishes a strict taxonomy of share capital to ensure total transparency for creditors, investors, and the state, dividing it into distinct legal categories:

- Authorized or Nominal Capital: The maximum amount of share capital that a company is legally permitted to raise, as explicitly registered in its Memorandum of Association (MoA).

•Issued Capital: The fractional component of the authorized capital that the company offers to the public or private subscribers for subscription over time. - Subscribed Capital: The portion of the issued capital that has been completely taken up and accepted by investors.

- Paid-Up Capital: The actual total amount of money received by the company from its shareholders against the issued shares, representing the true equity buffer available to absorb business losses and protect corporate creditors.

The regulation of this structural framework is governed by the foundational principle of "capital maintenance," a doctrine designed to preserve the integrity of the company’s fund pool. Because limited liability shields shareholders from personal exposure beyond their unpaid share value, creditors lend capital based on the assurance that the company's paid-up capital will not be improperly returned to investors or artificially eroded through fraudulent accounting maneuvers. Indian company law strictly enforces this doctrine by mandating that any alteration, reduction, or restructuring of a company’s share capital must navigate rigorous statutory procedures, including mandatory approvals from the National Company Law Tribunal (NCLT) and comprehensive clearances from creditors. This legal discipline ensures that the corporate capital structure remains a reliable, transparent indicator of the firm’s financial solvency.

EQUITY AND PREFERENCE SHARES

Section 43 of the Companies Act, 2013 restricts the share capital of a company limited by shares into two primary structural categories: equity share capital and preference share capital. This statutory division creates two distinct classes of investors with entirely different risk-reward profiles, voting privileges, and liquidation priorities. Preference share capital enjoys an explicitly elevated contractual status within the corporate cash flow matrix. Holders of preference shares possess a preferential right to receive a fixed rate of dividend before any dividend is allocated to ordinary equity shareholders. Furthermore, in a liquidation or winding-up scenario, preference shareholders retain a prior claim to the repayment of their capital, standing ahead of the residual equity pool but remaining subordinate to external secured and unsecured creditors.

In sharp contrast, equity share capital represents the true risk-bearing core of the enterprise. Equity shareholders are the ultimate residual claimants of the corporate vehicle; they profit substantially when the company achieves commercial success, but they bear the immediate burden of financial loss if the venture collapses. To balance this high-risk exposure, the law vests equity shareholders with the primary control rights of the corporation. Section 47 of the Act mandates that every member holding equity share capital possesses a statutory right to vote on every resolution placed before the company, with their voting power directly proportional to their share in the paid-up equity capital. Preference shareholders, conversely, are stripped of general voting rights, except on resolutions that directly affect their class rights, such as proposals to wind up the company or reduce its capital, or when their fixed dividends have remained entirely unpaid for a consecutive period of two years or more.

The Indian corporate landscape also permits the issuance of Equity Shares with Differential Rights (DVRs) as to dividend, voting, or otherwise. DVRs allow founders and tech-entrepreneurs to raise vast amounts of external equity capital from the public markets without diluting their operational control over the enterprise, typically by retaining high-voting-power shares while issuing low-voting, high-dividend shares to passive financial investors. To prevent promoters from abusing this mechanism to entrench inefficient management or marginalize minority investors, the Companies (Share Capital and Debentures) Rules impose strict regulatory ceilings, capping the total voting power exerted through differential shares at seventy-four percent of the total voting power, and requiring a spotless compliance record regarding financial reporting and debt servicing.

PUBLIC OFFERINGS AND PRIVATE PLACEMENTS

When a corporation seeks to mobilize capital from external markets, it must navigate two entirely distinct statutory tracks depending on the scale, nature, and target audience of the fund-raising exercise: Public Offerings or Private Placements. A public offering implemented either as an Initial Public Offering (IPO) by an unlisted company or a Further Public Offering (FPO) by an already listed entity represents an open invitation to the public at large to subscribe to the company’s securities. Because public offerings target vulnerable retail investors who lack access to internal corporate data, the Companies Act, under Chapter III, demands total financial disclosure. The company must draft and register a comprehensive "Prospectus" containing an exhaustive account of its financial health, promoter track records, ongoing material litigations, and the precise object for which the raised capital will be deployed. Any material misstatement, omission, or fraudulent claim within the prospectus triggers immediate, severe civil and criminal liabilities for the directors, promoters, and experts involved.

Conversely, when a company prefers a faster, more targeted capital-raising mechanism without incurring the heavy compliance costs of a public offering, it utilizes the "Private Placement" route under Section 42 of the Act. A private placement is a highly restricted offer of securities made selectively to a pre-identified group of sophisticated investors, such as institutional funds, venture capitalists, or high-net-worth individuals, who possess the financial expertise to independently evaluate corporate risk. To prevent companies from exploiting private placements as unregulated, backdoor public offerings a systemic loophole that resulted in major corporate scams in the past the legislature erected strict statutory boundaries around the process:

|

Regulatory Parameter |

Statutory Private Placement Obligation (Section 42) |

|

Numerical Cap |

Strictly limited to a maximum of 200 select persons in a single financial year, excluding Qualified Institutional Buyers (QIBs) and employees under ESOPs. |

|

Marketing Restrictions |

Complete ban on public advertisements, media releases, or utilization of external marketing channels to solicit subscriptions. |

|

Banking Discipline |

All subscription monies must be routed through separate, dedicated bank accounts; funds cannot be utilized until formal allotment shares are completed. |

|

Allotment Deadline |

Shares must be formally allotted within 60 days of fund receipt; failure triggers mandatory repayment at a penal 12% interest rate. |

RIGHTS ISSUES, BONUS ISSUES AND BUY-BACKS

Once a company is operational, it frequently alters its capital structure to accommodate subsequent financing needs or reward existing investors through Rights Issues, Bonus Issues, or Share Buy-Backs. A "Rights Issue," governed by Section 62 of the Companies Act, 2013, is rooted in the equitable doctrine of "pre-emption rights." This doctrine dictates that whenever a company decides to increase its subscribed capital by issuing fresh shares, it must first offer those shares to its existing equity shareholders in proportion to their existing paid-up capital. The pre-emption rule acts as a critical institutional shield protecting minority investors; it prevents corporate promoters from surreptitiously issuing cheap shares to external allies, an unfair practice that would instantly dilute both the economic value and the proportional voting power held by the minority block.

A "Bonus Issue," regulated under Section 63, represents a non-cash capitalization of a company’s accumulated financial reserves. When a company possesses vast undistributed profits within its Free Reserves, Securities Premium Account, or Capital Redemption Reserve, it can convert these accounting balances into paid-up share capital by issuing fully paid-up bonus shares to its existing members for free, in proportion to their holding. While a bonus issue increases the total number of shares outstanding, it does not alter the underlying net worth of the company or inject fresh cash into its operations; it merely reconfigures the internal equity ledger, lowering the market price per share to make the stock more liquid and accessible to retail day-traders.

Conversely, a share "Buy-Back," governed by Sections 68, 69, and 70, is the exact reverse of capital generation, representing a mechanism where a company purchases its own shares back from the market, effectively reducing its total paid-up share capital. Companies deploy buy-backs to return surplus, unutilised cash to shareholders, optimize their debt-to-equity ratios, or signal to the wider market that management believes the company's shares are significantly undervalued. However, because buy-backs result in a direct outflow of cash from the corporate vehicle, they carry the risk of asset-stripping and creditor prejudice. To counter this, the law prohibits companies from financing a buy-back through borrowed funds, mandates a post-buy-back debt-to-equity ratio ceiling of, and requires the creation of a specialized Capital Redemption Reserve to maintain capital stability and protect external lenders.

INVESTOR PROTECTION MECHANISMS

The regulatory core of Indian company law is deeply anchored in a multi-layered matrix of investor protection mechanisms designed to curb managerial overreach and ensure corporate democracy. A primary statutory instrument is the prevention of "Oppression and Mismanagement" under Sections 241 to 244 of the Act. This framework empowers minority shareholders holding at least ten percent of the issued share capital, or one-tenth of the total number of members, to directly approach the NCLT if they believe the affairs of the company are being conducted in a manner prejudicial to public interest, oppressive to any member, or destructive to the corporate estate. The NCLT possesses sweeping equitable powers to intervene, including the authority to terminate unfair contracts, regulate the future conduct of the business, remove fraudulent directors, and alter the share capital structure to restore balance.

Furthermore, the Companies Act, 2013 introduced the revolutionary mechanism of "Class Action Suits" under Section 245, providing a powerful collective-redress platform for scattered, retail investors who previously lacked the financial resources to contest large corporate conglomerates individually. Under this framework, a defined group of depositors or shareholders can file a unified lawsuit against the company, its directors, statutory auditors, or external consultants for any fraudulent, misleading, or ultra vires action. This collective mechanism ensures that if an auditing firm colludes with management to falsify accounts and artificially inflate share values, the investors can seek collective financial damages through a single, high-leverage legal proceeding. Complementing these judicial recourses is the administrative operation of the Investor Education and Protection Fund (IEPF) Authority. Under Section 125, any dividend, matured deposit, or share value that remains unclaimed or unpaid by investors for a consecutive period of seven years must be mandatorily transferred by the corporation to the government-administered IEPF. The IEPF Authority functions as a protective custodian, preventing companies from quietly absorbing forgotten investor money back into their corporate reserves, while running educational campaigns to increase financial literacy and providing a centralized, transparent digital pathway for retail investors or their legal heirs to reclaim their rightful financial assets.

REGULATORY ROLE OF SEBI

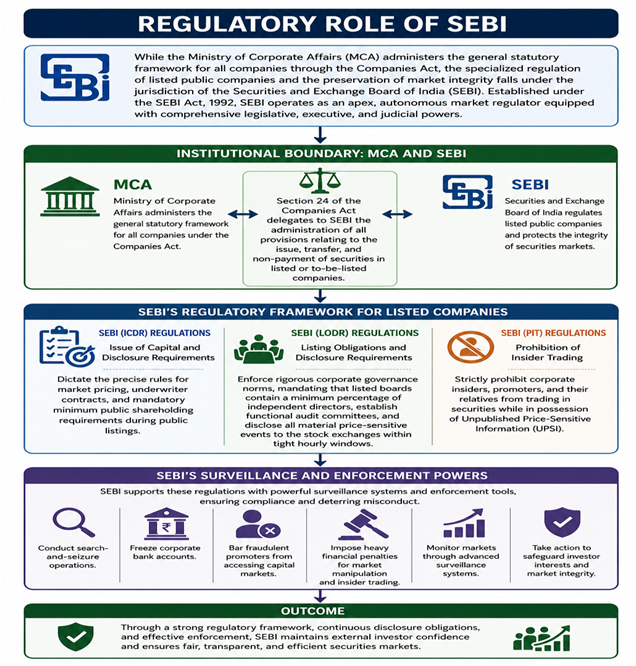

While the Ministry of Corporate Affairs (MCA) administers the general statutory framework for all companies through the Companies Act, the specialized regulation of listed public companies and the preservation of market integrity falls under the jurisdiction of the Securities and Exchange Board of India (SEBI). Established under the SEBI Act, 1992, SEBI operates as an apex, autonomous market regulator equipped with comprehensive legislative, executive, and judicial powers. The institutional boundary between the MCA and SEBI is explicitly recognized under Section 24 of the Companies Act, which delegates the administration of all provisions relating to the issue, transfer, and non-payment of securities in listed or to-be-listed companies directly to SEBI.

SEBI executes its protective mandate through an array of regulations that impose continuous disclosure obligations on corporate entities:

- SEBI (ICDR) Regulations: The Issue of Capital and Disclosure Requirements dictate the precise rules for market pricing, underwriter contracts, and mandatory minimum public shareholding requirements during public listings.

- SEBI (LODR) Regulations: The Listing Obligations and Disclosure Requirements enforce rigorous corporate governance norms, mandating that listed boards contain a minimum percentage of independent directors, establish functional audit committees, and disclose all material price-sensitive events to the stock exchanges within tight hourly windows.

- SEBI (PIT) Regulations: The Prohibition of Insider Trading regulations strictly prohibit corporate insiders, promoters, and their relatives from trading in securities while in possession of Unpublished Price-Sensitive Information (UPSI).

SEBI supports these regulations with powerful surveillance systems and enforcement tools, including the authority to conduct search-and-seizure operations, freeze corporate bank accounts, bar fraudulent promoters from accessing capital markets, and impose heavy financial penalties for market manipulation and insider trading, thereby maintaining external investor confidence.

CONTEMPORARY CHALLENGES IN CAPITAL MARKETS

Despite a sophisticated regulatory framework, the Indian capital market faces persistent challenges driven by technological evolution and complex financial engineering. A major regulatory challenge is the rise of retail trading algorithmic platforms and decentralized finance, which operate with unprecedented speed and create a massive digital information gap for ordinary retail investors. Furthermore, the modern corporate ecosystem is increasingly grappling with "greenwashing" in the capital markets, where companies issue specialized green bonds or sustainable equity instruments by presenting exaggerated or completely falsified environmental metrics to capture premium institutional capital, testing the enforcement capabilities of market regulators.

Another structural challenge centers on the regulation of Related Party Transactions (RPTs) within complex, multi-layered Indian business conglomerates. Promoters frequently utilize corporate restructuring, inter-corporate loans, and complex supply contracts with shell companies or private promoter-owned entities to subtly siphon off capital from listed subsidiaries where the public holds a significant stake. While SEBI and the Companies Act have tightened RPT disclosure rules and mandated that material RPTs require the approval of independent audit committees and unconflicted minority shareholders, tracking these hidden value-conspiracies remains highly challenging. Additionally, the rapid emergence of high-valuation tech startups backed by complex venture capital instruments such as convertible preference shares with complex liquidation preferences and anti-dilution ratchets introduces instability when these firms transition into the public markets, highlighting the need for continuous legal reform.

CONCLUSION

The legal architecture governing share capital regulation and investor protection under Indian company law represents a sophisticated, continuously evolving balance between capital mobilization and financial integrity. The transition from the old corporate regimes to the comprehensive framework of the Companies Act, 2013, supported by the targeted regulatory enforcement of SEBI, has successfully established a predictable, rule-based ecosystem for investors. By clearly delineating capital structures, enforcing strict statutory boundaries around public offers and private placements, and embedding pre-emption protections into corporate law, the Indian legal system has shifted the capital market away from an environment prone to systemic scams and toward a transparent, institutionalized framework that commands global investor confidence.

However, the long-term resilience of the Indian capital market depends on its ability to rapidly adapt to structural changes. As corporate conglomerates grow more sophisticated and digital finance platforms accelerate trading speeds, the boundaries of statutory oversight must expand accordingly. Protecting retail investors from complex related-party transactions, enforcing strict transparency around ESG and green capital instruments, and ensuring fast collective redress through class-action mechanisms remain critical legislative and regulatory priorities. By continuously anchoring share capital rules in the core principles of capital maintenance, corporate democracy, and absolute disclosure, the legal framework guarantees that corporate capital generation does not operate at the expense of investor safety, but remains a vital engine for sustainable, equitable economic growth.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others