Index of Headings

- Introduction

- Background: A Three Percent Gap and a Constitutional Question

- Arguments on Both Sides

- The Constitutional Framework: Twin Tests and Their Application

- The Financial Crunch Argument: How Far Does It Go?

- Precedents Distinguished: Entitlement vs. Quantum

- Significance of the Ruling

- What the Judgment Gets Right, and What It Leaves Open

- Conclusion

- FAQs

Introduction

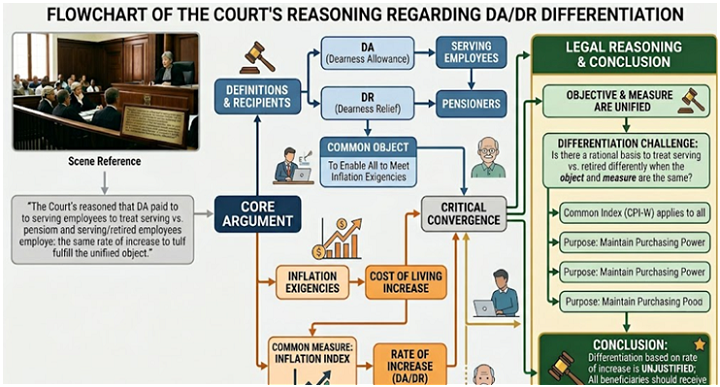

On April 10, 2026, the Supreme Court of India settled a question that sits at the crossroads of service law, constitutional equality, and fiscal governance: can the State provide dearness allowance to serving employees and dearness relief to pensioners at different rates, when both are linked to the same inflation index and serve the same object? The Court's answer was an unambiguous no.

A bench of Justices Manoj Misra and Prasanna B. Varale dismissed the appeals filed by the State of Kerala and the Kerala State Road Transport Corporation (KSRTC), holding that fixing a higher rate of enhancement of dearness allowance (DA) for serving employees than dearness relief (DR) for pensioners violates Article 14 of the Constitution. The judgment draws a firm line: financial constraints may justify deferring a benefit or choosing a cut-off date, but once a benefit is granted, it cannot be granted unequally when the underlying rationale is identical for both groups.

Background: A Three Percent Gap and a Constitutional Question

In February 2021, the Government of Kerala issued an order to meet inflationary pressures. Under that order, serving employees of Karnataka State Road Transport Corporation (KSRTC) were granted an enhancement in DA from 98% to 112%, an increase of 14 percentage points. Pensioners of KSRTC, by contrast, received an enhancement in DR from 98% to 109%, an increase of only 11 percentage points. Both enhancements were effective from March 2021.

Retired employees of KSRTC challenged this differentiation before the Kerala High Court, arguing that there was no rational basis for treating pensioners less favourably than serving employees when both categories were subject to the same inflationary pressures. A Single Judge dismissed the petitions, accepting the argument that serving employees and pensioners constitute two distinct classes and that different treatment of distinct classes is permissible under Article 14.

A Division Bench of the High Court reversed that finding. It held that once the State decided to extend the benefit of enhanced DA/DR to both employees and pensioners, it could not discriminate between them in the course of implementation. The object of the benefit, neutralising inflation, was common to both. The State and KSRTC then appealed to the Supreme Court.

Arguments on Both Sides

The State and KSRTC advanced two principal arguments.

First, they submitted that retired employees and serving employees constitute different classes, and differentiation between distinct classes does not violate the right to equality. Second, they invoked the financial condition of KSRTC as a justification for granting a lower rate of DR to pensioners.

In support of these positions, the appellants relied on a line of decisions in which the Supreme Court had upheld employer decisions to limit the scope of pension schemes, fix prospective cut-off dates for new benefits, and defer implementation of pay commission recommendations on grounds of financial constraints. The common thread in those decisions was judicial deference to executive action in matters of economic policy, particularly where the question was one of eligibility or entitlement to a benefit rather than the quantum at which an admitted benefit was to be paid.

The retired employees, represented by Senior Advocate V. Chitambaresh, pressed a narrower argument. They did not dispute that serving and retired employees are distinct categories, but rather contended that once the entitlement to both DA and DR were admitted, and once the rate of enhancement was accepted to be linked to a common inflation index, there was no justification for a differential rate. All in all, according to them - Inflation operates without regard to employment status. A pensioner faces the same rise in the price of goods as a serving employee and to remedy the harm differently when the harm is identical is arbitrary.

The Constitutional Framework: Twin Tests and Their Application

The Court's analysis began with the settled framework for testing classification under Article 14. Any classification by the State must satisfy two conditions: it must be founded on an intelligible differentia that distinguishes the grouped persons from others, and that differentia must have a rational nexus to the object sought to be achieved by the measure in question.

Justice Misra, writing for the bench, quoted Dr. D.Y. Chandrachud C.J. (as he then was) in State of Punjab v. Davinder Singh to reinforce the point that the basis of classification must have a nexus with the object of the classification, and that where there is little or no difference between the grouped and excluded persons relative to the object sought to be achieved, the classification is unreasonable.

Applying these tests to the facts, the Court identified the relevant object as the mitigation of hardship caused by inflation. Both DA and DR serve this object. The inflation index is common to serving and retired employees alike. Given that the object is identical and the measure of harm is the same, differentiating the rate of enhancement by reference to whether the recipient is in service or in retirement has no rational nexus to the object.

The Court's reasoned that DA is paid to serving employees and DR is paid to pensioners. The object of both DA and DR is common, which is to enable the serving employees and pensioners to meet the exigencies of inflation. As the object of both DR/DA is common, which is to meet inflationary pressures, and the inflation index is common to both the serving and the non-serving/retired employees, qua the measure, that is the rate of increase of DA/DR, could serving and retired employees be differentiated?

The answer, the Court held, was no. Differentiating the rate of increase has no rational nexus to the object. It is, therefore, discriminatory and arbitrary in violation of Article 14.

The answer, the Court held, was no. Differentiating the rate of increase has no rational nexus to the object. It is, therefore, discriminatory and arbitrary in violation of Article 14.

The Financial Crunch Argument: How Far Does It Go?

The most practically significant aspect of this judgment is its treatment of the financial crunch argument. Courts have long recognised that the fiscal health of a government or public sector employer is a legitimate consideration in making decisions about service benefits; an argument that was heavily favoured by the appellants.

The Supreme Court did not reject that principle. It accepted that financial constraints are a valid reason to defer disbursement of benefits or to fix separate implementation dates. But it drew a clear line at differential rates once a decision to grant the benefit has already been made. Once a decision is taken to provide certain allowances and also to increase them based on inflation, fixing a higher rate of increase for those who are serving than for those who have retired is arbitrary and violative of Article 14.

This distinction matters. The Court is not saying that KSRTC cannot defer an enhancement, pay it in phases, or consider its budget before making a decision. What it cannot do is announce an enhancement and then apply it unequally to two groups whose underlying need for the benefit is the same. The financial justification, if it had any force at all, would have justified not granting the enhancement to pensioners at all, or granting it at a later stage. It cannot justify granting it at a lower rate than that given to employees when the index driving both enhancements is shared.

Precedents Distinguished: Entitlement vs. Quantum

The Court dealt carefully with the body of precedent cited by the State. Each of the decisions relied upon by the appellants involved questions of eligibility or entitlement: whether a new pension scheme could be made applicable retrospectively, whether benefits could be confined to those retiring after a particular cut-off date, whether pay commission recommendations could be deferred for financial reasons. In all those cases, the dispute was about whether a benefit was owed at all, not about the rate at which an admitted benefit was to be paid.

The present case was different in a fundamental respect. There was no dispute that KSRTC pensioners were entitled to DR. There was no dispute that the DR was to be enhanced. The only question was whether the rate of enhancement could be lower for pensioners than for serving employees. On that question, the earlier decisions offered no support to the appellants because they all concerned access to a benefit rather than the terms of a benefit already granted.

This analytical distinction between entitlement and quantum is one of the more useful contributions of this judgment to service law jurisprudence. It clarifies the scope within which fiscal justifications operate: they can define the threshold of who receives a benefit and when, but once that threshold is crossed and a benefit is operative, the principle of equal treatment reasserts itself where the purpose is the same for all recipients.

Significance of the Ruling

The ruling carries implications beyond the KSRTC context. Public sector employers across India periodically revise DA and DR at rates that diverge from each other. In most cases, this is done through administrative orders that do not receive judicial scrutiny. The Supreme Court's ruling now provides a clear constitutional standard against which such orders can be measured.

The core proposition is narrow but important: where DA and DR are both admitted benefits, both linked to a common inflation index, and both designed to serve the same compensatory purpose, a differential rate of enhancement lacks rational nexus to the object and is unconstitutional. The State retains significant latitude in deciding whether to enhance, when to enhance, and how to phase the financial burden. What it cannot do is use fiscal arguments to provide a lower rate of relief to one group when the basis of entitlement is the same.

For retired public sector employees more broadly, this judgment is a reaffirmation that pensionary benefits are not merely ex gratia payments subject to the full discretion of the employer. Once a pension and its linked components are in place, they carry constitutional protection. The employer may manage the finances, but not by discriminating within a class of beneficiaries whose need for a particular benefit is legally and factually identical.

What the Judgment Gets Right, and What It Leaves Open

The most persuasive part of the Court's reasoning is its refusal to let the financial crunch argument do work it was never designed to do. Fiscal justifications in service law are legitimate as gatekeeping tools: they explain why a benefit was not introduced earlier, why it was limited to future retirees, or why implementation was deferred. But they cannot logically justify treating two groups differently once both are inside the gate. The moment KSRTC decided to enhance DR for pensioners at all, it conceded that it had the financial capacity to do so. The argument that it lacked the capacity to do so at the same rate as DA, without any supporting data or analysis placed before the Court, was exactly the kind of bare fiscal plea that Article 14 scrutiny is designed to test. The Court was right to find it inadequate.

There is also something constitutionally important in the Court's implicit treatment of pension as a vested right rather than a discretionary benefit. The line of cases relied upon by the State all arose in a context where the employer was making a prospective decision about a new scheme or an extended benefit. In those cases, the employer was genuinely exercising policy discretion at the threshold. In the present case, the employer was already inside a live obligation. Pension was being paid. DR was being paid. The enhancement was a revision of a subsisting entitlement. Applying financial constraint arguments to revisions of subsisting entitlements, as though they were fresh policy choices, conflates two very different kinds of decisions. The Court's instinct to separate them is right, even if the judgment does not spell out this distinction as sharply as it might have.

That said, the judgment leaves open some questions that practitioners and administrators will need to work through. The Court's holding is premised on the fact that both DA and DR are linked to a common inflation index and serve a common object. What happens when the inflation index used to calculate DA for serving employees differs structurally from the one used for pensioners? What if the employer argues, with actuarial support, that the cost-of-living adjustments relevant to a retired population are genuinely different from those relevant to an active workforce? The judgment, in its present form, does not address these possibilities. Its force is strongest where the link to a single common index is undisputed, as it was here.

A related gap is the Court's treatment of the quantum question in isolation from broader pension parity debates. In several states and central public sector undertakings, the problem is not merely a differential enhancement rate in one year, but a systematic pattern over many years where DR has consistently lagged behind DA, compounding the real-terms income gap between retirees and serving employees. The present judgment addresses the constitutional impermissibility of a single differential enhancement. It does not say anything about what remedy is available where the differential has been applied repeatedly over time, or whether past differentials, not challenged in time, can be revisited. These are open questions.

There is also a structural concern worth flagging. The judgment's logic, applied broadly, would seem to require that whenever an employer links both DA and DR to the same inflation index, parity of enhancement rate is a constitutional requirement. If that is correct, employers who wish to retain flexibility in their treatment of pensioners would need either to link DA and DR to different indices or to formally decouple the basis of enhancement. Neither is a legally objectionable course. But if the result of this judgment is to push employers toward formal decoupling rather than genuine parity, it will have achieved less than it appears. Courts cannot substitute for legislative or executive structures that actually protect pensioners.

Finally, there is the question of enforcement. The retired employees of KSRTC litigated this question from the High Court through the Supreme Court over the better part of five years. Most pensioners in similar positions, across smaller corporations, state undertakings, and semi-government bodies, do not have the resources or organisational capacity to sustain litigation of that kind. The judgment sets the rule. The harder problem, which no court can solve by itself, is building the institutional conditions under which the rule is applied without litigation having to be the vehicle.

Conclusion

This judgment does not disturb the well-established deference courts extend to fiscal policy decisions. It does not say that serving employees and pensioners are interchangeable in all respects. What it says is that where the State chooses to address a common problem, inflation, through a common mechanism, an inflation-linked allowance, it cannot then apply that mechanism at different rates to the two groups it has chosen to include, without any justification other than a financial constraint that would, at most, justify not making the decision at all.

Equality, as the Court reminded us, is antithetical to arbitrariness. A three-percentage point gap in an inflation-linked benefit, unsupported by any rationale tied to the object of that benefit, is precisely the kind of arbitrariness that Article 14 exists to prevent.

FAQs

1. Can the government give different DA and DR rates after this judgment?

No, not when both are linked to the same inflation index and serve the same purpose. The Court held that unequal rates in such a situation violate Article 14.

2. Does this mean financial constraints are irrelevant?

No. The government can still delay or phase benefits due to financial constraints, but it cannot use that reason to justify unequal rates once the benefit is granted.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others