Index

- Introduction

- Case Details and Coram

- Factual Background

- The Two Issues Before the Court

- Issue One: Causal Nexus Between the Accident and Death

- Issue Two: “Consumption” of Alcohol Is Not the Same as Being “Under the Influence”

- Strict Construction of Insurance Exclusion Clauses

- Precedents Relied Upon by the Court

- Ratio Decidendi and Its Limits

- The Court’s Final Order

- Key Takeaways

- Conclusion

- FAQs

1.Introduction

In a judgment dated 08.06.2026, the High Court of Kerala at Ernakulam, in a ruling delivered by Justice Harisankar V. Menon, dismissed a writ petition filed by United India Insurance Company challenging a Permanent Lok Adalat award of Rs. 15 lakhs in favour of the legal heirs of a deceased policyholder. The case, United India Insurance Company Co. Ltd. v. Salpriya and Others (WP(C) No. 16379 of 2023), turned on two recurring issues in motor accident insurance litigation: whether an injury sustained in an accident must be the sole cause of death for a claim to survive, and whether the mere presence of alcohol in a toxicology report is enough to invoke a policy’s intoxication exclusion clause.

The dispute illustrates the layered appellate architecture available to insurers dissatisfied with an award of the Permanent Lok Adalat: rather than an ordinary civil appeal, the insurer approached the High Court in its writ jurisdiction, and the Court’s scrutiny was accordingly confined to whether the Lok Adalat’s findings disclosed any legal infirmity, rather than a fresh reappraisal of the evidence on merits.

2.Case Details and Coram

- Case Title: United India Insurance Company Co. Ltd. v. Salpriya and Others

- Neutral Citation: 2026:KER:40266

- Case Number: WP(C) No. 16379 of 2023

- Court: High Court of Kerala at Ernakulam

- Coram: Hon’ble Mr. Justice Harisankar V. Menon

- Date of Judgment: 8 June 2026

- Counsel: Sri S. Arun Raj, Smt. C.T. Suja, and Sri Arjun S. Raj for the petitioner-insurer; Sri R.T. Pradeep and Sri Niranjan T. Pradeep for the respondents

- Forum Below: Permanent Lok Adalat, Thiruvananthapuram, O.P. No. 42 of 2021

3.Factual Background

The deceased, Babu, was found unconscious on the roadside on 30.11.2020 and was taken to hospital by ambulance. He succumbed to his injuries on 01.12.2020. The post-mortem certificate was dated 02.12.2020, and a toxicology report, based on a sample collected on 01.12.2020, recorded a positive result for alcohol. Babu held a motorcycle package insurance policy covering vehicle registration KL-20-D-5674. His legal heirs, his wife and two daughters, filed a claim with the insurer on the basis that he met with an accident while riding the insured motorcycle and later died.

The insurer contested the claim on three grounds: first, that the cause of death was occlusive coronary artery disease and not the accident; second, that the deceased was under the influence of alcohol at the time; and third, that the policy’s exclusion clauses accordingly barred the claim. The Permanent Lok Adalat rejected both contentions and awarded Rs. 15 lakhs to the legal heirs by an award dated 14.09.2022. The insurer challenged that award before the High Court under its writ jurisdiction.

4.The Two Issues Before the Court

The Court framed the dispute around two discrete questions: first, whether the post-mortem findings established a sufficient causal link between the accident and death, notwithstanding that the immediate medical cause of death was recorded as a coronary condition; and second, whether the toxicology report, standing alone, was sufficient to establish that the deceased was “under the influence of intoxicating liquor or drugs” within the meaning of the policy’s exclusion clause, as opposed to having merely consumed alcohol at some point before the accident.

5.Issue One: Causal Nexus Between the Accident and Death

The insurer argued that the post-mortem certificate attributed death to occlusive coronary artery disease, that the FIR made no reference to any accident, and that the accident register-cum-wound certificate similarly omitted any mention of an accident. The Court, however, found that the post-mortem report did not stop at recording the coronary condition; it went on to note that the injuries sustained in the accident could have accelerated or precipitated death, a finding that had to be read alongside the seven distinct injuries recorded on the first page of the report and the observation that the brain was congested. On this basis, the Court held that the death was substantially attributable to the accident, and that the FIR’s silence on the point could not, by itself, defeat a claim otherwise supported by a detailed post-mortem report.

In reaching this conclusion, the Court relied on the Supreme Court’s ruling in Alka Shukla v. Life Insurance Corporation of India, 2019 (2) KLT 3098, where, on a materially similar exclusion clause, the Apex Court had held that a claim under an accident benefit cover requires the bodily injury to be the direct result of the accident, with a proximate causal relationship between the injury and the accident. Applying this test, the Court found that the requisite proximate causal link stood established on the facts before it.

6.Issue Two: “Consumption” of Alcohol Is Not the Same as Being “Under the Influence”

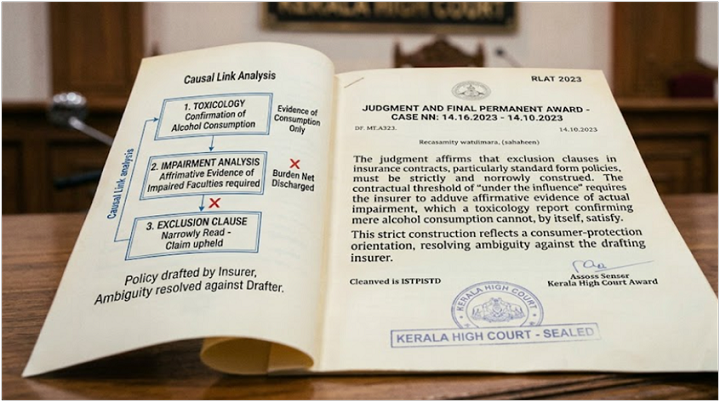

The insurance policy excluded liability only where the person riding the vehicle was “under the influence of intoxicating liquor or drugs”, not merely where alcohol had been consumed. The insurer’s case rested entirely on the toxicology report, which recorded a positive result for alcohol in the sample collected after death. The Court held that this was insufficient by itself: a positive toxicology finding establishes consumption, but consumption is not synonymous with impairment, and the exclusion clause is worded to require the latter.

The Court found no material on record, beyond the toxicology report itself, to establish that the deceased’s faculties were actually impaired at the relevant time, and held that the insurer had accordingly failed to discharge the burden of proof that rests on a party seeking to invoke a policy exclusion.

7.Strict Construction of Insurance Exclusion Clauses

The judgment proceeds on the settled contractual principle that exclusion clauses in a contract of insurance must be strictly and narrowly construed against the insurer seeking to rely on them. Where a policy conditions an exclusion on a specific state, here, being “under the influence” of alcohol, rather than mere consumption, the insurer must adduce affirmative evidence establishing that specific state. A toxicology report confirming the presence of alcohol addresses only the fact of consumption; it says nothing, without more, about the degree of impairment or its causal connection to the accident, and cannot, by itself, satisfy a contractual threshold pitched at impairment rather than consumption.

This principle of strict construction is not a mere technicality; it reflects the broader consumer-protection orientation of Indian insurance jurisprudence, under which ambiguity in a standard-form policy drafted by the insurer is resolved against the drafter, and exceptions carving out the insurer’s liability are read narrowly rather than expansively. An insurer that wishes to rely on a specific factual threshold, such as impairment rather than mere consumption, bears the evidentiary consequences of having chosen that threshold at the drafting stage.

8.Precedents Relied Upon by the Court

On the causation issue, the Court applied Alka Shukla v. Life Insurance Corporation of India, 2019 (2) KLT 3098 (Supreme Court), which requires a direct, proximate causal relationship between the bodily injury and the accident for a claim to survive under an accident benefit cover.

On the alcohol-exclusion issue, the Court relied on the Division Bench ruling in Oriental Insurance Company Ltd., Mattancherry v. Vineetha Nair and Others, 2016 (4) KHC 392, which had categorically held that mere consumption of alcohol is not sufficient to deny a claim, and that the insurer must place material on record showing the person was actually under the influence of alcohol. The Court also drew on the Supreme Court’s ruling in IFFCO Tokio General Insurance Company Ltd. v. Pearl Beverages Ltd., 2021 KHC OnLine 6232, which held that such claims must be assessed with reference to the circumstances of the accident, the evidence of alcohol consumption before or during travel, the actual impact of that consumption on the driver, and the case set up by the parties, rather than being resolved on the strength of a toxicology finding in isolation.

9.Ratio Decidendi and Its Limits

The binding ratio of the judgment is narrow and fact-sensitive: an insurer relying on an intoxication exclusion clause must adduce evidence of actual impairment linked to the accident, and cannot rest its case on a toxicology report alone. The Court’s finding on causation, that injuries recorded in a post-mortem report can establish a sufficient causal link to death even where a separate medical condition is also recorded as a contributing cause, is similarly confined to cases where the post-mortem report itself supports an accelerative or precipitating role for the accident-related injuries. The judgment does not hold that toxicology evidence is irrelevant altogether; it holds only that such evidence, without corroboration on impairment, is insufficient to meet the insurer’s burden.

10.The Court’s Final Order

Having found no infirmity in the Permanent Lok Adalat’s reasoning on either issue, the Court held that the writ petition was without merit and dismissed it, thereby affirming the award of Rs. 15 lakh in favour of the deceased’s legal heirs.

11.Key Takeaways

- A toxicology report showing the presence of alcohol establishes consumption, not impairment; insurers must independently prove the latter to invoke an “under the influence” exclusion clause.

- Insurance exclusion clauses are strictly construed against the insurer, which bears the burden of proving that the conditions for exclusion are clearly satisfied.

- A claim under an accident benefit cover requires a direct, proximate causal relationship between the bodily injury and the accident, per Alka Shukla v. LIC of India, 2019 (2) KLT 3098.

- Silence in an FIR about the cause of death does not defeat a claim otherwise supported by a detailed post-mortem report recording accident-related injuries.

- Toxicology findings must be read alongside evidence of the circumstances of the accident and the actual impact of consumption on the driver, per IFFCO Tokio General Insurance Company Ltd. v. Pearl Beverages Ltd., 2021 KHC OnLine 6232.

12.Conclusion

The ruling draws a workable distinction that recurs across Indian motor accident insurance litigation, between consumption and impairment, and insists that only the latter, supported by evidence connecting it to the accident, can justify denial of a claim.

For claimants’ counsel, the judgment provides a template for resisting exclusion-clause defences founded solely on post-mortem toxicology: emphasise the strict construction rule, insist on evidence of actual impairment, and rely on the accelerative-cause reasoning to meet any argument that a separate medical condition breaks the causal chain. For insurers, the case is a reminder that successfully invoking an intoxication exclusion requires more than a positive toxicology result; it requires proof, tied to the specific circumstances of the accident, that the insured’s faculties were in fact impaired.

13.FAQs

Q1. Can an insurance company deny an accident claim just because alcohol was found in the deceased’s toxicology report?

No. The Kerala High Court held that a toxicology report showing the presence of alcohol establishes consumption but not impairment. To invoke an exclusion clause worded around being ‘under the influence’ of alcohol, the insurer must produce additional evidence showing the person’s faculties were actually impaired at the relevant time.

Q2. If a post-mortem report lists a medical condition as the cause of death, can an accident insurance claim still succeed?

Yes, provided the post-mortem report also indicates that injuries from the accident could have accelerated or precipitated the death. Applying Alka Shukla v. Life Insurance Corporation of India, 2019 (2) KLT 3098, the Kerala High Court held that a proximate causal relationship between the accident-related injury and death is sufficient, even where a separate medical condition is also recorded.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :others