Bench:

Justice Sanjay Karol and Justice Manoj Misra

Date of Judgment:

10 November 2025

Parties:

Appellant: Akula Narayana

Respondents: Oriental Insurance Company Limited and Vehicle Owner

Subject Matter

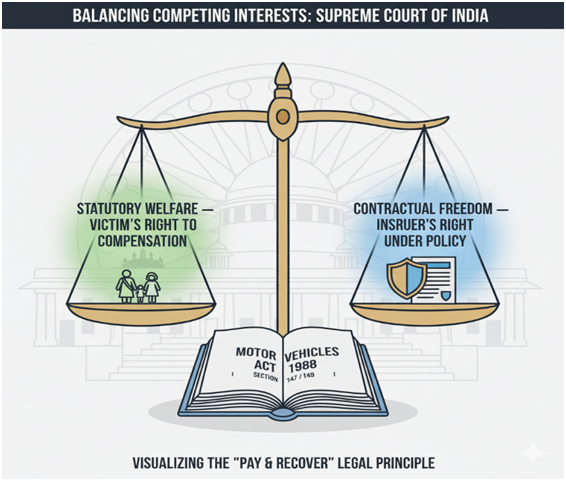

The dispute concerns the liability of an insurance company when the insured vehicle violates policy conditions by carrying passengers in excess of its permitted capacity. The central legal question concerns whether the insurer should be fully exonerated from liability due to such breach or whether the insurer must still satisfy the award in favour of the claimant and subsequently recover the amount from the vehicle owner.

The case also touches upon the role of additional premium collected for specific categories of persons, and whether such premium affects the determination of liability. The judgment reexamines the pay and recover doctrine in the broader context of motor accident compensation where competing interests of contractual freedom and statutory welfare intersect.

Provisions Involved

Section 147, Motor Vehicles Act 1988

Requirements of Policies and Limits of Liability

Requirements of policies and limits of liability.

(1) In order to comply with the requirements of this Chapter, a policy of insurance must be a policy which

(a) is issued by a person who is an authorised insurer, and

(b) insures the person or classes of persons specified in the policy to the extent specified in sub section (2)

(i) against any liability which may be incurred by him in respect of the death of or bodily injury to any person, including owner of the goods or his authorised representative carried in the vehicle, or damage to any property of a third party caused by or arising out of the use of the vehicle in a public place

(ii) against the death of or bodily injury to any passenger of a public service vehicle caused by or arising out of the use of the vehicle in a public place.

Proviso: A policy shall not be required to cover liability in respect of the death of or bodily injury to the employee of the insured arising out of and in the course of employment except for the driver or a conductor.

(2) A policy covered by this section shall cover the amount of liability incurred.

(3) The policy must be in the prescribed form and be issued by an authorised insurer.

Section 149, Motor Vehicles Act 1988

Duty of Insurers to Satisfy Awards

Duty of insurers to satisfy judgments and awards against persons insured in respect of third party risks.

(1) If, after a certificate of insurance has been issued, a judgment or award in respect of any liability covered by the policy is obtained against any person insured by the policy, then notwithstanding that the insurer may be entitled to avoid or cancel the policy, the insurer shall pay to the person entitled to the benefit of the decree the sum payable under the judgment or award.

(2) No sum shall be payable by an insurer under sub section (1) if, before the commencement of the proceedings in which the judgment or award is given, the insurer had obtained a declaration that the policy is void or has been cancelled or that the insurer is entitled to avoid it.

(3) Where the insurer has obtained such a declaration, the insurer shall not be liable to make any payment in respect of any judgment or award.

(4) Certain defences are available to the insurer, including breach of a specified condition of the policy, but the insurer must still satisfy the award where applicable.

Section 173, Motor Vehicles Act 1988

(1) Subject to the provisions of sub section (2), any person aggrieved by an award of a Claims Tribunal may, within ninety days from the date of the award, prefer an appeal to the High Court.

(2) No appeal shall lie against an award if the amount in dispute is less than ten thousand rupees.

(3) The High Court may entertain the appeal after the expiry of the said period of ninety days if it is satisfied that the appellant was prevented by sufficient cause from preferring the appeal in time.

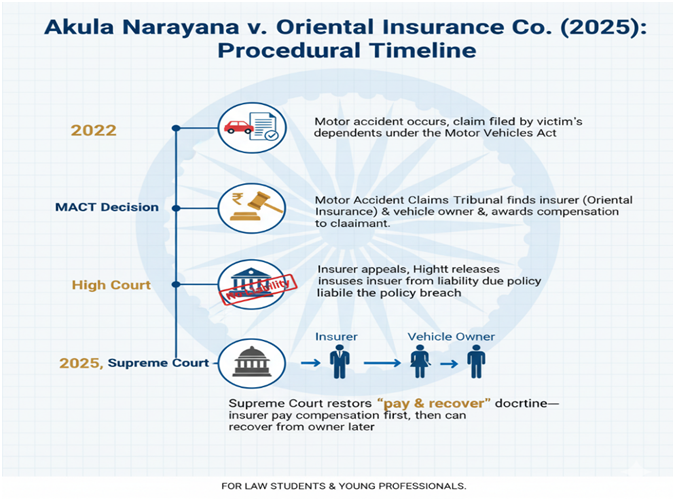

Factual Background

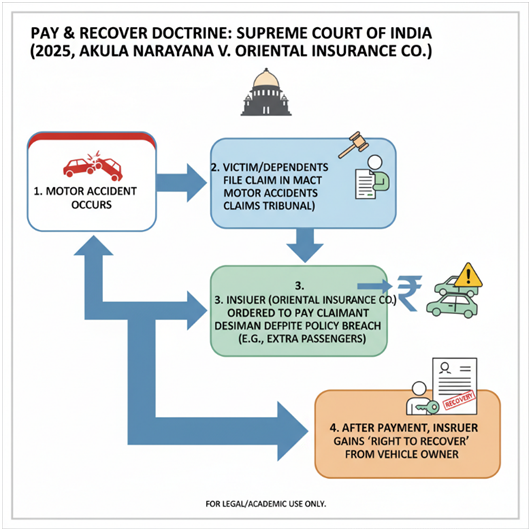

The case involves a motor accident involving a light motor vehicle insured with the Oriental Insurance Company Limited. The vehicle had the seating capacity for five persons including the driver. On the date of the accident, however, nine persons were travelling in it. One among them was the deceased in the case. The legal representatives of the deceased filed a claim petition before the Motor Accidents Claims Tribunal claiming compensation.

In the course of the proceedings, a very important piece of evidence unfolded when the administrative manager of the insurance company admitted during cross examination that the insurer had collected additional premium from the owner for covering three named persons described as the driver, conductor and cleaner.

The Tribunal construed the additional premium collected by the insurer to imply that the insurer had issued an enlarged policy beyond a strict statutory policy, at least as far as three unnamed persons occupying roles in the running of the vehicle were concerned.

The Tribunal held that while the deceased was not a driver, conductor or cleaner, the admission of having taken extra premium showed that the insurer intended to cover risks involving more than one person beyond the bare statutory minimum. The Tribunal considered the additional premium relevant and indicative of the insurer accepting broader responsibility. The Tribunal thus directed both the insurer and the vehicle owner to pay compensation to the claimant jointly and severally.

Procedural History

The insurance company challenged this decision of the Tribunal before the High Court of Telangana. The latter reversed the finding on joint liability and completely absolved the insurer of its liability. The High Court took a view that the extra premium paid for the driver, conductor and cleaner did not extend the policy to cover other passengers travelling in the vehicle, particularly when such persons are travelling in clear breach of seating capacity conditions.

The High Court further commented that overloading with nine persons in a vehicle meant for five is a fundamental breach of the insurance contract. Based on this, the High Court concluded that the insurer was required to pay nothing even temporarily.

The claimant, unable to recover compensation from the vehicle owner who had limited financial capacity, approached the Supreme Court. The appeal before the Supreme Court was thus limited to whether the High Court was justified in completely absolving the insurer from liability or whether the insurer should instead be compelled to pay the compensation and thereafter recover the amount from the owner.

Issues Before the Supreme Court

The question before the Supreme Court was whether the insurer should be completely exonerated from liability in circumstances featuring breach of seating capacity conditions and carriage of gratuitous passengers.

The Court was required to decide whether the High Court had erred in not applying the pay and recover doctrine. The other question was whether the additional premium collected by the insurer was relevant to liability, even though the deceased was not one of those categories of persons for whom premium had been collected.

Contentions of the Appellant

The appellant thus contended that though there was a breach of policy conditions, such breach would not absolve the insurer completely of the liability. Counsel appearing for the appellant relied considerably on the judgment of the Supreme Court in Mata Ram v. National Insurance Company Ltd., where the Supreme Court interpreted that payment of additional premium must be construed in favour of the insured and the third parties.

The appellant highlighted the discussion in paragraphs 11 to 14 in Mata Ram, wherein the Supreme Court explained that once the insurer accepts additional premium to cover three persons, the coverage should be interpreted liberally, unless it is excluded by express language used in the policy conditions.

The appellant also placed strong reliance on National Insurance Company Ltd. v. Swaran Singh, which is one of the foundational judgments in motor accident liability jurisprudence. The appellant stressed paragraph 110 of Swaran Singh, where the Supreme Court held that even when the insurer proves breach of policy conditions, the insurer must still satisfy the award and then recover the amount from the insured.

The appellant pointed out that the doctrine was developed specifically to protect innocent victims from being denied compensation due to the contractual dispute between insurer and insured. The appellant also referred to Shamanna v. Divisional Manager, Oriental Insurance Co. Ltd., where in paragraphs 15 to 20 the Supreme Court reaffirmed that once an insurance contract exists, technical breaches cannot prevent relief from reaching victims, and therefore the pay and recover doctrine is the appropriate tool to balance the interests of the parties.

The appellant also referred to the recent judgment in Rama Bai v. Amit Minerals, where the Supreme Court once again applied the pay and recover doctrine in situations arising from violation of policy conditions. The appellant urged that the present case was factually similar to Rama Bai and that the High Court had departed from established precedent by completely exonerating the insurer.

Respondent's Arguments

The insurer contended that the policy issued was a statutory policy and not a comprehensive policy and, therefore, only risks covered under section 147 of the Motor Vehicles Act were covered. The insurer thus contended that a gratuitous passenger, even while traveling in a private vehicle, is not a third party as such for the purpose of compulsory insurance.

The insurer emphasized that the deceased was not a driver, conductor or cleaner and, therefore, the additional premium had no relevance to the determination of liability. The insurer also placed strong reliance upon the serious breach of carrying nine persons in a vehicle meant for five and contended that such a breach was fundamental and went to the root of the contract. Thus, the insurer contended that it was entitled to be completely absolved from liability.

The insurer also argued that the Supreme Court’s precedents on pay and recover should not be applied mechanically because in carriage of excess passengers cases, courts have sometimes held that such breach completely absolves the insurer. The respondent argued that compelling the insurer to pay first and recover later would amount to rewriting the contract.

Court's Analysis

The Supreme Court began its analysis by observing that the insured vehicle owner had not challenged the conclusion reached by the High Court that he was not entitled to indemnification. Therefore, the Supreme Court confined itself to the legal question of whether the insurer should nonetheless be made to satisfy the award and recover the same from the owner.

The Court did not dispute the factual observation that the deceased did not belong to one of the three categories for whom additional premium was collected. However, the Court noted that this factual distinction did not decide the outcome since the essential legal issue was not whether the deceased was covered specifically, but whether the insurer should be directed to pay first and recover later.

The Supreme Court then turned to its long line of precedents. In Swaran Singh, the Court held in paragraph 110 that even when the insurer is successful in establishing breach, relief cannot be denied to the victim and that the policy of the law must ensure compensation is provided promptly. The Court recalled that Swaran Singh recognised that the insurer retains its contractual right to recover the amount from the owner and therefore no prejudice is caused to the insurer when asked to pay first. The Court found that the High Court had failed to meaningfully consider this principle.

The Court then went on to refer to the decision in Shamanna, wherein, the Supreme Court, at paragraph 15 to 20, held that the pay and recover doctrine would also apply in cases of invalid licences and other serious breaches. According to the Supreme Court, the rationale underlying pay and recover is the beneficial purpose of the Motor Vehicles Act, a social welfare legislation, for ensuring that victims receive compensation rather than encourage technical contractual disputes.

The Court also noticed that in Rama Bai, decided only the other day, it had reaffirmed this principle. In that case, despite breach on account of overloading, the Court insisted that the insurer first satisfy the award. The Court observed that the observations in Rama Bai are a clear pointer that Indian motor accident jurisprudence has moved along to ensure that victims do not suffer by reason of breaches committed by owners.

The Court was aware that the deceased might not have belonged to categories for whom an additional premium was paid, yet it still believed that the additional premium was relevant because it established that the insurer had accepted responsibility, over and above the statutory minimum, for risks arising from more than one person traveling in the vehicle. It concluded that this tended to support the view that total exoneration was not justified.

In the final analysis, the Court held that while the High Court was correct in identifying the breach, it erred in concluding that the insurer should be exonerated entirely. The Court concluded that fairness and justice require that the pay and recover doctrine be applied.

Holding

While giving the final directions, the Supreme Court cautioned that the central purpose of the Motor Vehicles Act is to secure just, fair and timely compensation for victims of road accidents, and this statutory purpose cannot be defeated by rigid reliance on contractual clauses between insurer and insured. It was held that even the presence of breach- much less a serious breach such as overloading or carrying gratuitous passengers-provides no automatic right of the insurer to absolute exoneration.

The Court emphasized that the jurisprudence on motor accident liability has evolved through a long line of authoritative decisions that have all consistently recognized that the insurer's contractual rights must operate in a manner not to undermine the claimant's right to compensation. Whereas the insurer has a contractual right to refuse indemnity to the insured in the presence of breach, the insurer does not acquire the right to shift the consequences of that breach onto the innocent victim.

The Court therefore held that the High Court committed a substantial error in treating the breach as a basis for complete immunity. The Supreme Court reasoned that such an approach runs counter to the pronouncements in Swaran Singh, which in paragraph 110 held that breaches of this nature do not enable the insurer to escape the statutory obligation to satisfy an award.

The Court noted that this principle was later reinforced in Shamanna, where, after reviewing earlier precedent, the Supreme Court held that the social welfare character of the Motor Vehicles Act dictates that the insurer must pay first and recover later. By reemphasising these foundational principles, the Court clarified that the High Court was not correct in suggesting that carrying excess passengers was a breach so fundamental as to justify full exoneration.

The Supreme Court then turned to the fact that the insurer had accepted additional premium for the driver, conductor and cleaner. While this did not directly translate into coverage for the deceased, the Court observed that this undisputed fact showed that the insurer had consciously extended the scope of its financial risk in the present policy. The Court considered this a relevant circumstance for determining whether the insurer was entitled to claim complete immunity.

The Court found that the collection of an additional premium showed that the insurer had already contemplated risks due to more than one person being associated with the operation of the vehicle. Even though the deceased did not fall into those categories, the fact of the insurer's admission weakened any argument that the policy should be construed strictly and in the narrowest possible sense.

In the light of these combined considerations, the Supreme Court held that the appropriate course was to direct the insurance company to satisfy the award and thereafter exercise its right of recovery against the owner of the vehicle. The balancing mechanism, as explained by the Court, protects the three interests involved: the claimant obtains compensation without being put to protracted enforcement proceedings, while in the case of the insurer, the amount is paid only temporarily, and finally, the insured bears the ultimate financial responsibility for the breach he committed.

The Court also emphasized that the insurer, being a corporate body with greater financial resources and a structured mechanism for recovery, was far better positioned to initiate recovery proceedings than a bereaved claimant who may lack the means to pursue litigation against a defaulting owner.

The Supreme Court also emphasized that allowing the insurer to escape liability altogether would lead to inequitable results, as most of the vehicle owners in such cases are usually impecunious or evasive. In such a scenario, the claimant would, for all purposes and intents, be deprived of compensation. The Court held that this would not be consonant with the very basic structure of the Act insofar as it being remedial legislation aimed at mitigating the hardship rather than increasing the frustration.

By ordering the insurer to pay the award and recover the same separately, the Court ensured that procedural fairness accorded with substantive justice. The Court thus concluded that the principle of pay and recover was not merely a matter of judicial discretion but a doctrinal necessity created to reconcile the tension between the contractual rights of insurers and the statutory rights of claimants.

The Court accordingly held that the High Court erred in failing to apply this well-established principle and restored the Tribunal’s direction, modifying it only to the extent of clarifying that the insurer is entitled to recover the amount from the owner after complying with the award.

MACT And Its Current Application

Speaking to LaWyersClub India’s Content Head, Advocate Yuvraj Singh said that “As far as I am concerned, the MACT process is one of the most workable remedies our system gives to road accident victims, but it still has its rough edges, and that is precisely where lawyers need to show up. My first advice to anyone who has been in an accident is simple.

Advising the victims under MACT or individual wanting to file a claim under the Act, Mr Singh said that “Keep your head straight, collect whatever evidence you can, and speak to a lawyer at the earliest. Never let the threats of insurance companies about the breach of policy scare you. The Supreme Court has made it clear that even if there is a technical issue, like carrying a few extra passengers, the insurer cannot back out totally. The idea of pay and recover ensures that the victim gets the compensation first and later on, the insurer and the vehicle owner can sort out their dispute. Your rights should not take a back seat.”

For individuals wanting to file a claim and go through the process the advocate said that

“People often agree on low settlements because someone pressures them or convinces them that the Tribunal process is too slow. That is almost always a mistake. What each individual should understand that there is no need to get nervous about the whole process, one should just go to the Tribunal, file your claim, and let the system do its work.

The paperwork might look heavy, but with a decent lawyer guiding you, the process is far more manageable than it appears. I have seen too many people lose out because they tried private negotiations or got overwhelmed by legal terms.”

Finishing off, advising the advocates, Mr Singh said that “To an advocate, none of these cases should feel mechanical. Each one is a real family that has suffered a loss. Our job is not just citing sections but rather ensuring that relief actually goes to the person entitled to it. Preparation matters. Study the policy. Determine whether any extra premiums have been paid. And most importantly, do not hesitate to challenge an insurer's denial when precedence has settled the law in your favor. Take the claimant seriously. Their struggle deserves more than routine representation.”