INTRODUCTION

The traditional paradigm of the business corporation, famously articulated by Milton Friedman, posited that the sole social responsibility of business is to increase its profits while operating within the rules of the game. For decades, this shareholder-centric model dominated corporate legal theory and practice, viewing expenditures on social welfare as an unauthorized tax on investor capital or a misallocation of corporate resources. However, the unchecked expansion of global commerce, coupled with escalating environmental degradation, resource scarcity, and systemic social inequities, exposed the limitations of this narrow economic view. The modern public corporation is no longer conceptualized merely as a private contract among shareholders, but as a powerful social institution with a massive footprint on the community and the planet. This realization fueled the rise of Corporate Social Responsibility (CSR) the principle that companies must be accountable to a broader spectrum of stakeholders, including employees, consumers, local communities, and the environment.

The structural nature of CSR has undergone a profound transformation over the past two decades. What began as a loose collection of voluntary ethics, corporate philanthropy, and public relations strategies has evolved into a highly codified regime of mandatory compliance. This shift reflects a growing legislative consensus that voluntary corporate altruism is insufficient to address pressing sustainable development challenges. Governments worldwide are increasingly leveraging corporate balance sheets to supplement state-driven social development programs. The transition from voluntary engagement to statutory mandate fundamentally redefines the relationship between capital accumulation and social equity. This research paper examines this regulatory metamorphosis, analyzing the statutory mechanisms, compliance challenges, and corporate governance shifts that occur when ethical obligations are translated into legally enforceable corporate mandates.

EVOLUTION OF CSR IN CORPORATE GOVERNANCE

The integration of CSR into the formal architecture of corporate governance has its roots in the evolving theories of the firm. Early iterations of CSR were deeply rooted in stewardship and paternalistic charity, where wealthy industrialists channeled personal or corporate surpluses into building schools, hospitals, and community infrastructure. These actions were distinct from the core operations of the company and were treated as discretionary expressions of civic virtue. As corporate structures grew more complex, academic scholarship began to challenge the shareholder-primacy model, introducing "Stakeholder Theory." This framework argues that a corporation’s long-term commercial survival depends on the support and goodwill of all entities affected by its operations. Consequently, managing stakeholder relationships ceased to be a peripheral moral concern and became a core strategic priority for the board of directors.

As stakeholder theory gained traction, international bodies began developing standardized frameworks to institutionalize corporate accountability. Initiatives such as the United Nations Global Compact, the Organization for Economic Co-operation and Development (OECD) Guidelines for Multinational Enterprises, and the Global Reporting Initiative (GRI) established voluntary benchmarks for human rights, labor standards, and environmental conservation. Despite their widespread adoption, these international frameworks lacked coercive enforcement mechanisms, allowing corporations to engage in "greenwashing" the practice of projecting an environmentally or socially responsible image while continuing unsustainable core operations. The manifest inadequacy of purely voluntary standards prompted a global regulatory pivot. Jurisdictions began moving toward a harder-edged regulatory approach, culminating in legislative interventions that directly embedded social and environmental obligations into corporate law statutes.

STATUTORY FRAMEWORK UNDER SECTION 135

The pioneering legislative experiment in mandatory corporate social responsibility occurred with the enactment of the Indian Companies Act, 2013, which introduced Section 135. This statutory provision converted CSR from an ethical choice into a rigid, arithmetic compliance obligation for companies operating within the jurisdiction. Section 135 applies a strict objective threshold based on the financial health of the enterprise, targeting any company that matches or exceeds specific fiscal benchmarks during any financial year:

- Net Worth: Five billion rupees or more

- Turnover: Ten billion rupees or more

- Net Profit: Fifty million rupees or more

Companies crossing any of these thresholds are legally mandated to spend at least two percent of their average net profits made during the three immediately preceding financial years on specified CSR activities.

The statutory framework does not grant corporations unfettered discretion regarding where they deploy these funds. The permissible areas of social expenditure are explicitly restricted to the items listed under Schedule VII of the Act, which covers broad national development goals such as eradicating hunger and poverty, promoting education, ensuring environmental sustainability, reducing gender inequality, and funding technology incubators. Crucially, the legislature deliberately designed the law to prevent corporations from using CSR as an internal employee benefit or a direct commercial marketing tool; expenditures that benefit only the company's employees or their families do not qualify as valid CSR spend. By creating a clear statutory line between ordinary business expenses and genuine social investments, the framework treats corporate profit as an asset that must partially clear its social debt before being distributed as pure residual wealth to equity investors.

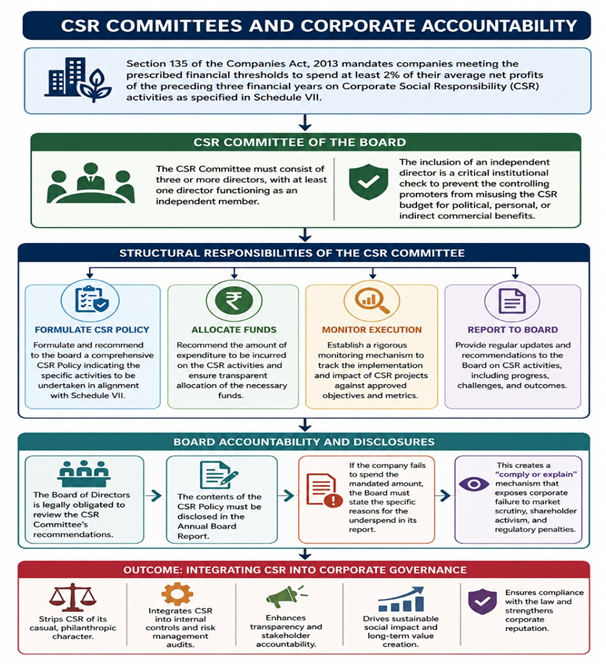

CSR COMMITTEES AND CORPORATE ACCOUNTABILITY

To ensure that the mandatory spending requirements are executed with high administrative precision, Section 135 establishes a distinct governance mechanism within the corporate hierarchy: the Corporate Social Responsibility Committee of the Board. The statute mandates that the CSR Committee must consist of three or more directors, with at least one director functioning as an independent member. The inclusion of an independent director is a critical institutional check, designed to prevent the controlling promoters from weaponizing the CSR budget to fund political pet projects, family-run trusts, or entities that provide indirect commercial or personal advantages to the insiders.

The CSR Committee holds sweeping structural responsibilities that directly affect corporate accountability:

The committee is legally tasked with formulating and recommending to the board a comprehensive CSR Policy that indicates the specific activities to be undertaken in alignment with Schedule VII. Furthermore, the committee is responsible for transparently allocating the necessary funds and establishing a rigorous monitoring mechanism to track the execution metrics of the approved projects.

By elevating CSR to a board-level committee responsibility, the law strips social spending of its casual, philanthropic character and integrates it directly into the company’s internal controls and risk management audits. The board of directors is legally obligated to review the committee's recommendations and disclose the contents of the CSR policy in the annual board report. If the company fails to spend the mandated amount, the board must state the specific reasons for the underspend in its report, anchoring a "comply or explain" mechanism that exposes corporate failure directly to market scrutiny, shareholder activism, and regulatory penalties.

ESG PRINCIPLES AND SUSTAINABLE DEVELOPMENT

The transition of CSR from voluntary ethics to mandatory compliance has occurred in tandem with the rise of Environmental, Social, and Governance (ESG) principles within international capital markets. While traditional CSR focuses primarily on corporate philanthropy and community engagement, ESG functions as an investment-driven risk assessment framework. Global institutional investors, sovereign wealth funds, and asset managers increasingly utilize ESG metrics to evaluate a corporation's long-term resilience and ethical footprint. They recognize that companies with poor environmental records, systemic labor disputes, or weak governance structures present severe financial risks, including sudden regulatory fines, litigation costs, and terminal reputational damage.

|

Dimension |

Core Operational Focus Areas |

|

Environmental (E) |

Carbon footprint reduction, waste management systems, and transition to renewable energy sources. |

|

Social (S) |

Human rights compliance, workplace safety standards, and equitable local community development. |

|

Governance (G) |

Executive compensation limits, board diversity metrics, and anti-corruption compliance frameworks. |

The statutory codification of CSR provides a concrete, data-driven foundation for the "Social" component of ESG reporting. By compelling companies to track, measure, and report their social interventions, mandatory CSR laws convert vague ethical assertions into verifiable compliance data. This integration is essential for advancing sustainable development goals, as it forces corporate capital to align with global environmental and social targets. Consequently, mandatory compliance ensures that the pursuit of commercial profit does not occur in isolation from the overarching societal imperative to preserve natural capital and foster inclusive economic growth.

REGULATORY COMPLIANCE AND REPORTING OBLIGATIONS

As jurisdictions hardened their stance on corporate accountability, the regulatory compliance and reporting obligations surrounding CSR grew increasingly stringent. Initial versions of mandatory CSR legislation operated on a flexible "comply or explain" model, where a failure to spend the allocated budget could be legally absolved by providing a plausible explanation in the annual board report. However, regulatory authorities observed that many corporations abused this flexibility, offering generic, repetitive administrative excuses to justify substantial underspending. To close these compliance loopholes, legislatures amended the statutory frameworks, transforming the regime from "comply or explain" to "comply or carry forward," backed by severe penal consequences.

Under current regulatory protocols, any unspent CSR funds allocated for an ongoing project must be transferred within thirty days of the end of the financial year to a specialized, ring-fenced bank account known as the "Unspent Corporate Social Responsibility Account." These funds must be fully deployed toward the designated project within a statutory window of three financial years. If a company fails to utilize the money within this period, or if the unspent funds are not tied to any ongoing project, the law mandates that the remaining balance be transferred directly to state-administered national development funds within six months of the financial year's close.

Furthermore, the reporting requirements have been heavily expanded to include mandatory impact assessments. Companies with large annual CSR budgets are legally required to hire independent external agencies to conduct rigorous impact evaluations of their social projects. The resulting comprehensive reports, detailed with project milestones and third-party verifications, must be annexed to the annual financial disclosures and published prominently on the company's public interface, ensuring total transparency for regulators and market stakeholders alike.

JUDICIAL AND ADMINISTRATIVE DEVELOPMENTS

The operational boundaries of mandatory CSR are continuously defined, clarified, and reinforced by the judiciary and state administrative agencies. As corporations devised complex accounting maneuvers to circumvent their spending obligations, regulatory departments responded by issuing detailed, binding clarifications and guidance circulars. These administrative decrees explicitly established that any expenditure undertaken by a corporation during the ordinary course of its business cannot be repackaged as a CSR contribution. For instance, an automobile manufacturer cannot claim the internal development of an eco-friendly engine prototype as a CSR activity, as that investment directly enhances its core commercial product line.

Simultaneously, the judiciary has taken a firm, non-interventionist stance regarding the enforcement of the statutory thresholds, while strictly penalizing procedural non-compliance and financial misrepresentation. Tribunals handling corporate disputes have consistently ruled that the statutory definitions of "Net Profit" must be calculated in strict compliance with prescribed accounting standards, invalidating corporate attempts to artificially deflate profit metrics through arbitrary asset depreciations or inter-corporate accounting maneuvers.

Furthermore, courts have actively intervened to prevent the misappropriation of CSR funds by corporate insiders. In landmark corporate governance cases, where promoters routed CSR allocations into private family trusts or shell companies under the guise of rural development, the judiciary has pierced the corporate veil. Judges have imposed heavy financial penalties and ordered criminal prosecutions for criminal breach of trust and corporate fraud, signaling to the commercial market that mandatory social spending is a serious statutory obligation that cannot be subverted for personal or administrative enrichment.

CHALLENGES IN IMPLEMENTATION

Despite the robust statutory framework and expanding regulatory enforcement, the implementation of mandatory CSR faces severe systemic challenges that hinder its overall efficacy. A primary operational hurdle is the highly unequal geographic distribution of CSR expenditures. The statutory text frequently includes provisions directing companies to give preference to the "local areas" around which they operate. Because the vast majority of industrial manufacturing plants, technology hubs, and corporate headquarters are concentrated in heavily developed, urbanized states, these regions receive an overwhelming share of corporate social investments. Conversely, impoverished, rural, and economically marginalized provinces that lack a significant corporate presence find themselves structurally starved of CSR funding, exacerbating existing regional economic imbalances rather than mitigating them.

Another significant challenge is the acute deficit of institutional capacity and professional expertise within corporate structures to manage complex social development projects. Designing, executing, and monitoring long-term social interventions such as reviving depleted water tables, combatting chronic malnutrition, or restructuring rural educational systems requires deep sociological insight and specialized field experience. Most corporate managers, trained exclusively in commercial operations and financial efficiency, lack these competencies.

This capacity gap has led to a widespread reliance on intermediary Non-Governmental Organizations (NGOs) and civil society trusts to implement projects. However, the social sector is highly fragmented, and many small-scale implementation agencies lack transparent financial controls, leading to administrative inefficiencies, leakage of funds, and a proliferation of superficial, short-term projects that deliver high public relations visibility but negligible long-term societal impact.

CONCLUSION

The evolution of Corporate Social Responsibility from a domain of voluntary business ethics to an era of mandatory legal compliance represents a fundamental shift in contemporary corporate jurisprudence. The law has dismantled the archaic view that corporations operate in an isolated economic vacuum with obligations limited strictly to equity investors. By codifying social spend and anchoring it within board-level committee structures, the legal framework positions the modern public corporation as an active partner in national sustainable development. The statutory model demonstrates that corporate capital can be systematically redirected toward public welfare without compromising the core entrepreneurial incentives that drive market economies.

However, the long-term success of the mandatory CSR experiment depends on the continuous refinement of its regulatory and operational architecture. Policymakers must actively address the structural defects in the system, particularly the geographic concentration of funds, by developing mechanisms that incentivize investments in remote and historically marginalized regions. Furthermore, building institutional collaboration between corporate bodies, specialized academic institutions, and verified civil society organizations is essential to bridge the current implementation capacity gap. By ensuring absolute transparency, enforcing strict impact assessments, and aligning corporate mandates with broader ESG principles, the legal system can guarantee that mandatory corporate social responsibility ceases to be a bureaucratic box-checking exercise and becomes a transformative instrument of equitable economic growth.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others