INTRODUCTION

Corporate governance is no longer viewed merely as a mechanism for ensuring regulatory compliance. In today's corporate environment, it represents the foundation upon which investor confidence, business sustainability, and long-term economic growth are built. A company may possess strong financial performance and an experienced management team, yet the absence of effective governance can expose it to fraud, mismanagement, regulatory scrutiny, and loss of public trust. Over the past two decades, several corporate failures across the world have demonstrated that governance lapses often originate not because laws are absent, but because those entrusted with oversight fail to exercise their responsibilities effectively.

The role of independent directors has therefore become central to modern corporate governance. They are expected to serve as impartial decision-makers who are capable of scrutinising management decisions without being influenced by promoters or executive directors. Their presence on the board is intended to create a system of checks and balances, ensuring that decisions are taken in the interests of the company as a whole rather than for the benefit of a select group of individuals.

India's corporate governance framework underwent a significant transformation after the exposure of the Satyam Computer Services scandal in 2009. The scandal revealed that despite the presence of reputed professionals on the board, governance mechanisms had failed to detect large-scale accounting fraud. This prompted lawmakers and regulators to revisit the existing framework governing board independence and corporate accountability. The enactment of the Companies Act, 2013, coupled with stricter disclosure requirements under the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, sought to redefine the responsibilities and accountability of independent directors.

However, an important question continues to remain unanswered. Has the legal framework succeeded in creating truly independent oversight, or has the position of independent director become a statutory requirement that often exists only on paper? While the law prescribes qualifications, duties, and codes of conduct, practical challenges such as promoter dominance, inadequate information, and fear of regulatory liability continue to affect the effectiveness of independent directors.

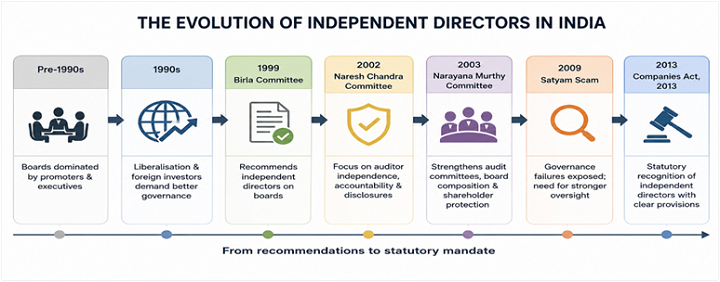

THE EVOLUTION OF INDEPENDENT DIRECTORS IN INDIA

The concept of independent directors is relatively new in Indian corporate law. Prior to the liberalisation of the Indian economy in the 1990s, corporate boards were largely dominated by promoters and executive management. Board meetings often functioned as formal approval mechanisms rather than forums for objective deliberation. Minority shareholders had limited representation, and there were few institutional safeguards to ensure transparency in corporate decision-making.

Economic liberalisation and the increasing participation of foreign institutional investors created pressure for stronger governance standards. Investors sought greater transparency, accountability, and protection against managerial abuse. This shift led to a series of committee reports that laid the foundation for the modern governance framework.

The Kumar Mangalam Birla Committee Report (1999) was the first comprehensive effort to introduce structured corporate governance norms in India. It recommended that listed companies should include independent directors on their boards to improve objectivity and reduce the concentration of power among promoters. The committee recognised that independent directors could bring specialised expertise while providing impartial oversight over executive management.

The recommendations of the Birla Committee were followed by the Naresh Chandra Committee (2002), which focused on strengthening auditor independence, board accountability, and financial disclosures. It emphasised that corporate governance should not be viewed merely as a compliance exercise but as an essential component of responsible corporate management.

Subsequently, the Narayana Murthy Committee (2003) proposed significant improvements relating to audit committees, disclosure obligations, board composition, and shareholder protection. Many of its recommendations were incorporated into Clause 49 of the Listing Agreement, which governed listed companies before the enactment of the Companies Act, 2013.

The exposure of accounting fraud in Satyam Computer Services in 2009 further accelerated governance reforms. The scandal demonstrated that merely appointing distinguished professionals as independent directors could not guarantee effective oversight if they failed to question management decisions or exercise due diligence.

These developments ultimately culminated in the enactment of the Companies Act, 2013, which for the first time gave statutory recognition to independent directors and prescribed detailed provisions governing their appointment, qualifications, tenure, duties, evaluation, and liability.

WHY INDEPENDENT DIRECTORS MATTER

A corporate board performs two distinct functions. First, it assists management in developing long-term business strategies. Second, it supervises management to ensure that corporate powers are exercised responsibly.

These two roles may sometimes conflict. Executive directors are directly involved in the company's operations and may naturally support management decisions. Promoter directors may also have personal or financial interests that influence their judgment. In such circumstances, independent directors act as neutral participants whose responsibility is not to represent management but to protect the interests of the company and all its stakeholders.

The need for independent directors becomes particularly evident during situations involving related party transactions, mergers and acquisitions, executive remuneration, financial reporting, internal investigations, and allegations of corporate misconduct. Since independent directors do not participate in day-to-day management, they are expected to assess these matters objectively and question decisions that may adversely affect shareholders or creditors.

Their importance extends beyond shareholder protection. Independent directors contribute to better risk management, stronger compliance systems, improved financial oversight, and enhanced corporate reputation. Companies with effective independent boards are generally viewed more favourably by investors because robust governance reduces business uncertainty and enhances confidence in management.

Corporate governance is therefore not merely about complying with statutory provisions; it is about ensuring that power within the company is exercised responsibly. Independent directors serve as one of the principal mechanisms through which this objective is achieved.

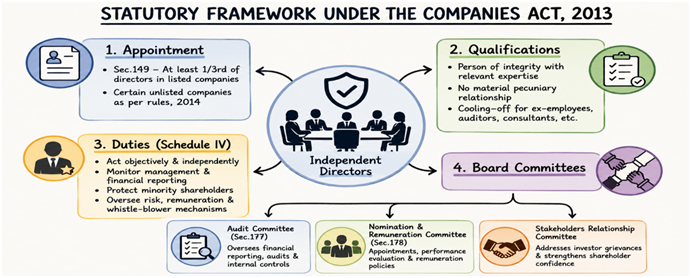

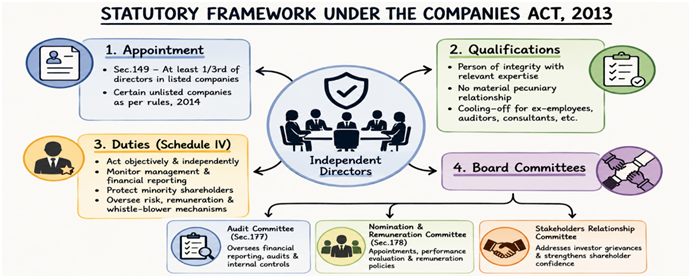

STATUTORY FRAMEWORK UNDER THE COMPANIES ACT, 2013

The Companies Act, 2013 introduced an extensive legal framework governing independent directors. Unlike the earlier regime, where governance standards were primarily contained in listing requirements, the Act gave statutory recognition to board independence.

Appointment of Independent Directors

Section 149 of the Companies Act mandates that every listed public company shall appoint at least one-third of its total number of directors as independent directors. Certain classes of unlisted public companies meeting prescribed financial thresholds are also required to appoint independent directors under the Companies (Appointment and Qualification of Directors) Rules, 2014.

The objective behind prescribing mandatory board independence is to ensure that strategic decisions are not taken exclusively by promoters or executive management.

Unlike nominee directors who may represent financial institutions or investors, independent directors are expected to remain free from external influence and exercise independent judgment throughout their tenure.

Qualifications for Independent Directors

Section 149(6) prescribes detailed eligibility conditions.

An independent director must be a person of integrity possessing relevant expertise and experience. More importantly, the individual should have no material pecuniary relationship with the company, its promoters, holding company, subsidiary, or associate company that could compromise objective decision-making.

The Act also excludes persons who have recently served as employees, auditors, consultants, legal advisers, or key managerial personnel of the company from being appointed as independent directors within the prescribed cooling-off period. These restrictions seek to eliminate situations where previous professional relationships might influence board decisions.

The emphasis on independence reflects the legislative intention that board oversight should remain free from conflicts of interest rather than merely satisfying procedural requirements.

Duties and Responsibilities of Independent Directors

The significance of independent directors lies not in their designation but in the responsibilities they are expected to discharge. Recognising this, the Companies Act, 2013 devotes an entire Schedule IV to prescribing a Code for Independent Directors. Unlike general directors, independent directors are expected to maintain a higher degree of objectivity and professional scepticism while participating in board affairs.

Schedule IV requires them to uphold ethical standards, act objectively, exercise independent judgment, and devote sufficient time to understanding the company's business. They are expected to scrutinise the performance of management, monitor financial reporting, satisfy themselves regarding the integrity of internal financial controls, and ensure that robust risk management systems are in place.

One of their most important responsibilities is safeguarding the interests of minority shareholders. In promoter-driven companies, board decisions may occasionally favour controlling shareholders at the expense of minority investors. Independent directors are expected to ensure that such decisions are fair, transparent, and taken in accordance with law.

Their duties also extend to reviewing executive remuneration, evaluating the performance of non-independent directors, participating in succession planning, and overseeing whistle-blower mechanisms. These responsibilities illustrate that an independent director is not expected to remain a passive participant in board meetings but to actively contribute towards improving corporate governance.

However, the law also recognises that independent directors cannot supervise every operational aspect of a company. Their responsibility is to ensure that governance systems function effectively and that management remains accountable.

INDEPENDENT DIRECTORS AND BOARD COMMITTEES

The effectiveness of independent directors becomes particularly evident through the specialised committees of the board. Modern corporate governance relies extensively on these committees because they enable detailed examination of complex issues that cannot be adequately addressed during general board meetings.

Audit Committee

Section 177 of the Companies Act, 2013 requires specified companies to constitute an Audit Committee, with independent directors forming a majority of its members. The committee acts as the primary oversight body for financial reporting and corporate accountability.

Its functions include reviewing financial statements before they are approved by the board, supervising statutory and internal audits, examining related party transactions, monitoring internal financial controls, and evaluating the effectiveness of risk management mechanisms.

Following corporate scandals such as Satyam, the role of audit committees has become increasingly significant. Investors often regard an active audit committee as one of the strongest indicators of good corporate governance.

Nomination and Remuneration Committee

Executive compensation has frequently attracted criticism where remuneration appears disconnected from corporate performance. To address this concern, Section 178 provides for the Nomination and Remuneration Committee, which consists largely of independent directors.

The committee recommends appointments to the board, evaluates directors' performance, formulates remuneration policies, and ensures that executive compensation remains transparent and linked to long-term corporate objectives.

Stakeholders Relationship Committee

Independent directors also participate in the Stakeholders Relationship Committee, which addresses investor grievances relating to transfer of securities, dividends, and shareholder communications. Although this committee often receives less attention than the Audit Committee, it plays an important role in strengthening investor confidence and protecting shareholder rights.

GOVERNANCE OVERSIGHT UNDER THE SEBI (LODR) REGULATIONS, 2015

While the Companies Act provides the statutory framework governing independent directors, listed companies are additionally regulated by the Securities and Exchange Board of India through the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

The SEBI Regulations adopt a stricter approach towards board independence, reflecting the regulator's objective of strengthening investor protection in listed entities.

The regulations prescribe detailed requirements regarding board composition, approval of related party transactions, disclosure obligations, evaluation of independent directors, familiarisation programmes, and committee composition.

One of the notable features of the SEBI framework is its emphasis on continuous disclosure. Investors are entitled to receive timely and accurate information regarding material events affecting the company. Independent directors therefore play a crucial role in ensuring that disclosures made by listed companies are complete, truthful, and not misleading.

SEBI has also sought to reduce promoter influence over board appointments by introducing stricter eligibility norms and requiring greater shareholder participation in the appointment and reappointment of independent directors.

The Kotak Committee and Strengthening Board Independence

Recognising that governance standards required further improvement, SEBI constituted the Committee on Corporate Governance under the chairmanship of Uday Kotak in 2017.

The Kotak Committee observed that while Indian corporate law contained detailed governance provisions, practical implementation remained inconsistent. It therefore recommended several reforms aimed at improving board effectiveness.

Among its significant recommendations were:

- strengthening the independence criteria for directors;

- increasing the number of independent directors on certain boards;

- improving disclosure standards;

- separating the offices of Chairperson and Managing Director in specified companies;

- enhancing the role of board committees;

- improving evaluation mechanisms for independent directors.

Many of these recommendations were subsequently incorporated into the SEBI (LODR) Regulations through amendments issued in 2018 and later years.

The Kotak Committee's work reflects an important shift in regulatory thinking. Rather than focusing solely on statutory compliance, it emphasised the quality of governance and the effectiveness of board oversight.

JUDICIAL APPROACH TOWARDS INDEPENDENT DIRECTORS

Courts have repeatedly recognised that imposing automatic liability upon independent directors would discourage competent professionals from serving on corporate boards. Consequently, judicial decisions have sought to balance accountability with fairness.

Section 149(12) of the Companies Act limits the liability of independent directors. They are liable only for acts of omission or commission that occurred with their knowledge, attributable through board processes, and where they failed to act diligently.

This provision acknowledges the practical reality that independent directors are not involved in day-to-day management.

The Supreme Court, in Sunil Bharti Mittal v. CBI (2015), observed that criminal liability cannot be imposed merely because an individual occupies the position of director. There must be specific material demonstrating his or her involvement in the alleged offence.

Similarly, courts have consistently held that directors cannot be prosecuted solely on the basis of their designation. Liability must arise from specific allegations establishing participation, consent, connivance, or negligence.

This judicial approach is significant because independent directors often rely upon information provided by management. Holding them automatically liable for every corporate irregularity would defeat the very purpose of attracting experienced professionals to corporate boards.

Nevertheless, judicial protection does not absolve independent directors from exercising reasonable care. Where they knowingly approve illegal transactions or deliberately ignore obvious warning signs, they may still incur civil or criminal liability.

LESSONS FROM MAJOR CORPORATE GOVERNANCE FAILURES

Perhaps the strongest argument in favour of independent directors emerges from corporate failures where governance mechanisms proved ineffective despite elaborate legal frameworks.

Satyam Computer Services

The Satyam scandal remains India's most significant corporate governance failure. In January 2009, Chairman B. Ramalinga Raju admitted to manipulating the company's financial statements for several years, resulting in one of the largest accounting frauds in Indian corporate history.

The scandal exposed serious weaknesses in board oversight. Despite the presence of eminent professionals on the board, financial irregularities continued undetected for years. Independent directors were criticised for relying excessively upon information supplied by management instead of questioning suspicious financial trends.

The scandal directly influenced the enactment of stronger governance provisions under the Companies Act, 2013.

IL&FS

Nearly a decade later, the collapse of Infrastructure Leasing & Financial Services (IL&FS) once again raised concerns regarding the effectiveness of board oversight.

The company accumulated enormous debt while governance failures remained largely unnoticed. Questions were raised regarding whether independent directors exercised adequate diligence in reviewing financial disclosures, debt exposure, and risk management practices.

The IL&FS crisis demonstrated that governance failures often develop gradually rather than suddenly, making active board supervision essential.

CHALLENGES FACED BY INDEPENDENT DIRECTORS

Despite the comprehensive legal framework under the Companies Act, 2013 and the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, independent directors continue to face several practical challenges. A major concern is the dominance of promoters in Indian companies, where appointments and reappointments often depend upon the support of controlling shareholders. This may affect the ability of independent directors to express dissent or challenge management decisions freely. Another challenge is information asymmetry. Since independent directors are not involved in the day-to-day operations of the company, they rely heavily on information provided by management. If such information is incomplete or delayed, effective oversight becomes difficult. Further, increasing regulatory expectations, evolving business risks, and concerns regarding personal liability often discourage experienced professionals from accepting board positions.

CONCLUSION

Independent directors have become a cornerstone of corporate governance in India. Their role extends beyond fulfilling statutory requirements to ensuring transparency, accountability, ethical decision-making, and the protection of stakeholder interests. The Companies Act, 2013 and the SEBI (LODR) Regulations have considerably strengthened the legal framework governing their appointment, duties, and responsibilities. However, effective corporate governance ultimately depends on the willingness of independent directors to exercise independent judgment and actively participate in board deliberations.

Corporate governance failures such as Satyam, IL&FS, and Yes Bank demonstrate that legal provisions alone cannot prevent corporate misconduct. Independent directors must remain vigilant, seek adequate information, and question management decisions whenever necessary. As India's corporate sector continues to expand and integrate with global markets, truly independent and competent boards will play a crucial role in promoting sustainable business practices, protecting investor confidence, and ensuring long-term corporate accountability.

GOVERNANCE OVERSIGHT UNDER THE SEBI (LODR) REGULATIONS, 2015

While the Companies Act provides the statutory framework governing independent directors, listed companies are additionally regulated by the Securities and Exchange Board of India through the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

The SEBI Regulations adopt a stricter approach towards board independence, reflecting the regulator's objective of strengthening investor protection in listed entities.

The regulations prescribe detailed requirements regarding board composition, approval of related party transactions, disclosure obligations, evaluation of independent directors, familiarisation programmes, and committee composition.

One of the notable features of the SEBI framework is its emphasis on continuous disclosure. Investors are entitled to receive timely and accurate information regarding material events affecting the company. Independent directors therefore play a crucial role in ensuring that disclosures made by listed companies are complete, truthful, and not misleading.

SEBI has also sought to reduce promoter influence over board appointments by introducing stricter eligibility norms and requiring greater shareholder participation in the appointment and reappointment of independent directors.

The Kotak Committee and Strengthening Board Independence

Recognising that governance standards required further improvement, SEBI constituted the Committee on Corporate Governance under the chairmanship of Uday Kotak in 2017.

The Kotak Committee observed that while Indian corporate law contained detailed governance provisions, practical implementation remained inconsistent. It therefore recommended several reforms aimed at improving board effectiveness.

Among its significant recommendations were:

- strengthening the independence criteria for directors;

- increasing the number of independent directors on certain boards;

- improving disclosure standards;

- separating the offices of Chairperson and Managing Director in specified companies;

- enhancing the role of board committees;

- improving evaluation mechanisms for independent directors.

Many of these recommendations were subsequently incorporated into the SEBI (LODR) Regulations through amendments issued in 2018 and later years.

The Kotak Committee's work reflects an important shift in regulatory thinking. Rather than focusing solely on statutory compliance, it emphasised the quality of governance and the effectiveness of board oversight.

JUDICIAL APPROACH TOWARDS INDEPENDENT DIRECTORS

Courts have repeatedly recognised that imposing automatic liability upon independent directors would discourage competent professionals from serving on corporate boards. Consequently, judicial decisions have sought to balance accountability with fairness.

Section 149(12) of the Companies Act limits the liability of independent directors. They are liable only for acts of omission or commission that occurred with their knowledge, attributable through board processes, and where they failed to act diligently.

This provision acknowledges the practical reality that independent directors are not involved in day-to-day management.

The Supreme Court, in Sunil Bharti Mittal v. CBI (2015), observed that criminal liability cannot be imposed merely because an individual occupies the position of director. There must be specific material demonstrating his or her involvement in the alleged offence.

Similarly, courts have consistently held that directors cannot be prosecuted solely on the basis of their designation. Liability must arise from specific allegations establishing participation, consent, connivance, or negligence.

This judicial approach is significant because independent directors often rely upon information provided by management. Holding them automatically liable for every corporate irregularity would defeat the very purpose of attracting experienced professionals to corporate boards.

Nevertheless, judicial protection does not absolve independent directors from exercising reasonable care. Where they knowingly approve illegal transactions or deliberately ignore obvious warning signs, they may still incur civil or criminal liability.

LESSONS FROM MAJOR CORPORATE GOVERNANCE FAILURES

Perhaps the strongest argument in favour of independent directors emerges from corporate failures where governance mechanisms proved ineffective despite elaborate legal frameworks.

Satyam Computer Services

The Satyam scandal remains India's most significant corporate governance failure. In January 2009, Chairman B. Ramalinga Raju admitted to manipulating the company's financial statements for several years, resulting in one of the largest accounting frauds in Indian corporate history.

The scandal exposed serious weaknesses in board oversight. Despite the presence of eminent professionals on the board, financial irregularities continued undetected for years. Independent directors were criticised for relying excessively upon information supplied by management instead of questioning suspicious financial trends.

The scandal directly influenced the enactment of stronger governance provisions under the Companies Act, 2013.

IL&FS

Nearly a decade later, the collapse of Infrastructure Leasing & Financial Services (IL&FS) once again raised concerns regarding the effectiveness of board oversight.

The company accumulated enormous debt while governance failures remained largely unnoticed. Questions were raised regarding whether independent directors exercised adequate diligence in reviewing financial disclosures, debt exposure, and risk management practices.

The IL&FS crisis demonstrated that governance failures often develop gradually rather than suddenly, making active board supervision essential.

CHALLENGES FACED BY INDEPENDENT DIRECTORS

Despite the comprehensive legal framework under the Companies Act, 2013 and the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, independent directors continue to face several practical challenges. A major concern is the dominance of promoters in Indian companies, where appointments and reappointments often depend upon the support of controlling shareholders. This may affect the ability of independent directors to express dissent or challenge management decisions freely. Another challenge is information asymmetry. Since independent directors are not involved in the day-to-day operations of the company, they rely heavily on information provided by management. If such information is incomplete or delayed, effective oversight becomes difficult. Further, increasing regulatory expectations, evolving business risks, and concerns regarding personal liability often discourage experienced professionals from accepting board positions.

CONCLUSION

Independent directors have become a cornerstone of corporate governance in India. Their role extends beyond fulfilling statutory requirements to ensuring transparency, accountability, ethical decision-making, and the protection of stakeholder interests. The Companies Act, 2013 and the SEBI (LODR) Regulations have considerably strengthened the legal framework governing their appointment, duties, and responsibilities. However, effective corporate governance ultimately depends on the willingness of independent directors to exercise independent judgment and actively participate in board deliberations.

Corporate governance failures such as Satyam, IL&FS, and Yes Bank demonstrate that legal provisions alone cannot prevent corporate misconduct. Independent directors must remain vigilant, seek adequate information, and question management decisions whenever necessary. As India's corporate sector continues to expand and integrate with global markets, truly independent and competent boards will play a crucial role in promoting sustainable business practices, protecting investor confidence, and ensuring long-term corporate accountability.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others