INTRODUCTION

Corporate governance has become one of the defining aspects of modern corporate law, shaping how companies are managed, controlled, and held accountable. In today's interconnected global economy, investors and stakeholders no longer assess companies solely on the basis of profitability or market performance. Instead, they increasingly evaluate transparency, ethical decision-making, board independence, regulatory compliance, and long-term sustainability before investing or engaging with a corporation. Consequently, corporate governance has evolved from being a matter of internal management to a legal and strategic imperative.

India's corporate governance framework has undergone a remarkable transformation over the last three decades. Before the economic liberalisation of 1991, governance standards were relatively underdeveloped, largely because the economy was characterised by government control, limited competition, and concentrated promoter ownership. However, with the opening of the Indian economy, the influx of foreign investment, and the rapid expansion of capital markets, the need for internationally accepted governance standards became increasingly evident.

The evolution of corporate governance in India has been shaped by a combination of regulatory reforms, expert committee recommendations, corporate scandals, judicial interventions, and changing investor expectations. Voluntary governance principles gradually evolved into mandatory legal obligations through legislative measures such as the Companies Act, 2013 and the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015. Today, corporate governance extends beyond shareholder protection to include environmental responsibility, corporate social responsibility (CSR), stakeholder welfare, risk management, and sustainable business practices.

MEANING AND IMPORTANCE OF CORPORATE GOVERNANCE

Corporate governance refers to the system of rules, policies, processes, and institutional mechanisms through which companies are directed and controlled. It establishes the relationship between a company's board of directors, management, shareholders, creditors, employees, regulators, and other stakeholders while ensuring that corporate objectives are achieved in an accountable and transparent manner.

The Organisation for Economic Co-operation and Development (OECD) defines corporate governance as the framework through which corporate objectives are established, performance is monitored, and accountability is ensured.

Good corporate governance rests upon four universally accepted principles:

- Transparency in decision-making and financial reporting.

- Accountability of directors and senior management.

- Fairness towards all shareholders, particularly minority investors.

- Responsibility towards stakeholders and society.

Effective governance generates numerous benefits. It improves investor confidence, reduces financial fraud, facilitates access to domestic and international capital, enhances operational efficiency, strengthens corporate reputation, and promotes long-term sustainability. Conversely, weak governance often results in financial irregularities, managerial abuse, erosion of shareholder wealth, regulatory penalties, and loss of public trust.

HISTORICAL EVOLUTION

Before the economic reforms of 1991, corporate governance in India was relatively underdeveloped due to the Licence Raj, which subjected businesses to extensive government regulation and industrial licensing. Most companies were family-owned, with concentrated ownership and limited participation from institutional investors. As a result, issues such as board independence, minority shareholder protection, and corporate transparency received little attention.

The Companies Act, 1956 governed corporate functioning by prescribing provisions relating to directors, audits, and company management. However, its focus was primarily on statutory compliance rather than governance standards. Limited integration with global markets also meant that international governance practices had little influence on Indian companies. Nevertheless, this period laid the legal foundation for the governance reforms that followed.

Liberalisation and the Beginning of Modern Corporate Governance

The economic liberalisation of 1991 marked a turning point in the evolution of corporate governance in India. Opening the economy to foreign investment and global competition increased the need for transparency, accountability, and better corporate disclosures.

The establishment of SEBI as a statutory regulator under the SEBI Act, 1992 further strengthened investor protection and securities market regulation. As Indian companies began accessing global capital, corporate governance evolved from a compliance-based concept to an essential framework for enhancing investor confidence and ensuring responsible corporate management.

MAJOR COMMITTEES AND THEIR CONTRIBUTIONS

Recognising the need for stronger governance standards, industry bodies and regulators constituted several expert committees whose recommendations significantly shaped India's corporate governance framework.

CII Code (1998)

The Confederation of Indian Industry (CII) introduced India's first voluntary Desirable Corporate Governance Code in 1998. It recommended the appointment of independent directors, constitution of audit committees, improved financial disclosures, and greater board accountability. Though voluntary, it laid the foundation for future governance reforms.

Kumar Mangalam Birla Committee (1999)

Constituted by SEBI, this committee recommended mandatory governance standards for listed companies. Its key recommendations included independent directors, audit committees, enhanced financial disclosures, and improved shareholder protection. These recommendations formed the basis of Clause 49 of the Listing Agreement.

Naresh Chandra Committee (2002)

Formed in the aftermath of global corporate scandals, the Committee focused on strengthening auditor independence and improving financial reporting. It recommended restrictions on non-audit services, greater accountability of auditors, and stronger disclosure norms.

Narayana Murthy Committee (2003)

The Narayana Murthy Committee further strengthened governance by recommending better disclosure standards, whistleblower mechanisms, enhanced audit committee responsibilities, risk management reporting, and greater transparency. Many of its recommendations were later incorporated into Clause 49.

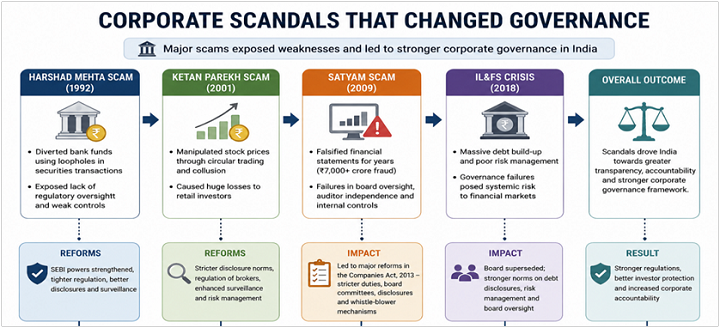

CORPORATE SCANDALS THAT CHANGED GOVERNANCE

While expert committees and regulatory initiatives laid the foundation for corporate governance reforms, some of the most significant changes were prompted by major corporate scandals.

Harshad Mehta Scam (1992)

The Harshad Mehta securities scam was one of the earliest financial scandals to expose serious deficiencies in India's banking and capital market systems. By exploiting loopholes in the issuance of Bank Receipts (BRs) and government securities transactions, Harshad Mehta diverted thousands of crores of rupees from the banking system into the stock market, artificially inflating share prices.

The scam highlighted the absence of effective regulatory oversight, weak internal controls within banks, inadequate disclosure mechanisms, and poor coordination among financial regulators. Although the fraud was primarily a securities market scam rather than a traditional corporate governance failure, it underscored the importance of transparency and accountability in financial markets.

In response, the powers of the Securities and Exchange Board of India (SEBI) were significantly strengthened. Reforms included tighter regulation of stock exchanges, improved settlement systems, enhanced disclosure requirements, and stricter surveillance of securities transactions. The scam also accelerated the modernisation of India's financial infrastructure and reinforced the need for robust governance mechanisms within listed companies.

Ketan Parekh Scam (2001)

Nearly a decade later, the Ketan Parekh scam once again exposed vulnerabilities in India's capital markets. Parekh manipulated the prices of select technology and media stocks through circular trading, financing arrangements, and collusion with certain financial institutions and brokers.

The collapse of these artificially inflated stocks caused substantial losses to retail investors and raised concerns regarding market manipulation, insider dealings, and regulatory enforcement.

Following the scam, SEBI introduced several reforms aimed at improving market integrity. These included stricter disclosure norms, tighter regulation of brokers and intermediaries, enhanced surveillance systems, shorter settlement cycles, and stronger risk management mechanisms within stock exchanges.

The episode reaffirmed that effective corporate governance extends beyond companies themselves and requires well-regulated financial markets capable of detecting and preventing manipulation.

Satyam Scam (2009)

The Satyam Computer Services scandal is widely regarded as India's "Enron moment" and remains the country's most significant corporate governance failure.

In January 2009, the company's founder and Chairman, B. Ramalinga Raju, admitted to falsifying the company's financial statements for several years by inflating revenues, profits, cash balances, and assets. The fraud, amounting to over ₹7,000 crore, revealed serious failures in corporate governance despite the existence of statutory audits, independent directors, and regulatory oversight.

The scandal exposed multiple governance deficiencies, including ineffective board supervision, compromised auditor independence, weak internal controls, and inadequate scrutiny by audit committees. It also demonstrated that formal compliance with governance norms is insufficient if ethical leadership and institutional accountability are absent.

The Satyam scandal fundamentally reshaped India's corporate governance framework. It directly influenced several provisions incorporated into the Companies Act, 2013, including stricter duties for directors, enhanced auditor accountability, mandatory board committees, improved disclosure obligations, and stronger whistle-blower mechanisms. It also led to greater emphasis on independent directors and board evaluation processes.

IL&FS Crisis (2018)

The collapse of Infrastructure Leasing & Financial Services (IL&FS) in 2018 represented one of India's largest corporate governance failures in the financial sector. Despite being regarded as a systemically important financial institution, IL&FS accumulated massive debt while its governance framework failed to identify and manage the associated risks.

Investigations revealed deficiencies in board oversight, risk management, financial disclosures, and internal controls. The crisis affected banks, mutual funds, infrastructure projects, and financial markets, demonstrating how governance failures within a single institution could pose systemic economic risks.

The Government of India superseded the existing board under the Companies Act, 2013 and appointed a new board to stabilise the institution. Subsequently, regulators strengthened governance norms relating to debt disclosures, risk management, board oversight, and financial reporting for large financial entities. The IL&FS crisis highlighted the necessity of integrating effective risk management into corporate governance rather than treating it as a separate compliance function.

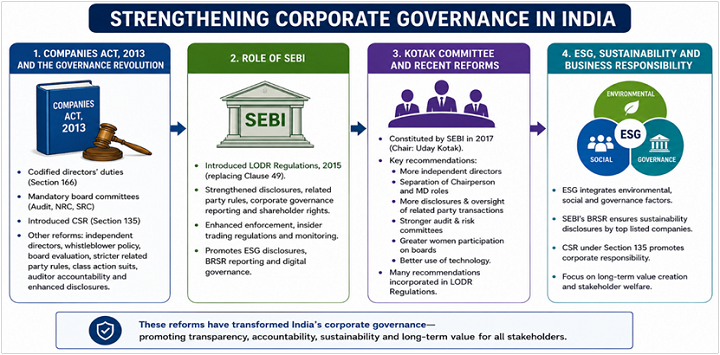

COMPANIES ACT, 2013 AND THE GOVERNANCE REVOLUTION

The Companies Act, 2013 represents the most significant milestone in the evolution of corporate governance in India. Replacing the Companies Act, 1956, the legislation introduced an entirely new governance architecture based on transparency, accountability, stakeholder protection, and ethical corporate conduct.

One of its most important contributions was the codification of directors' duties under Section 166, which requires directors to act in good faith, exercise due care and diligence, avoid conflicts of interest, and act in the best interests of the company, its employees, shareholders, the community, and the environment.

The Act also institutionalised board committees by mandating the constitution of Audit Committees, Nomination and Remuneration Committees, and Stakeholders Relationship Committees for specified classes of companies. These committees strengthened board oversight and improved decision-making processes.

Another landmark reform was the introduction of mandatory Corporate Social Responsibility (CSR) under Section 135, making India one of the first countries to impose statutory CSR obligations on qualifying companies. This reflected a broader understanding that corporations owe responsibilities not only to shareholders but also to society.

Additional governance reforms included:

- Mandatory appointment of independent directors.

- Vigil mechanism and whistleblower policy.

- Performance evaluation of the board and independent directors.

- Class action suits under Section 245.

- Stricter regulation of related-party transactions.

- Increased accountability of auditors.

- Enhanced financial disclosures.

The Companies Act, 2013 therefore shifted Indian corporate governance from a compliance-oriented framework to one based on ethical responsibility and stakeholder accountability.

ROLE OF SEBI

The Securities and Exchange Board of India (SEBI) has played a central role in shaping and continuously strengthening corporate governance standards for listed entities.

Beyond its regulatory functions under the SEBI Act, 1992, SEBI has consistently updated governance requirements in response to market developments and international best practices.

Its most significant contribution came through the introduction of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (LODR Regulations), which replaced the earlier Listing Agreement, including Clause 49. The LODR Regulations consolidated governance requirements relating to board composition, disclosure obligations, related-party transactions, shareholder rights, corporate governance reporting, and timely dissemination of material information.

SEBI has also strengthened governance through stricter disclosure norms, insider trading regulations, continuous monitoring of listed companies, enhanced enforcement powers, and penalties for non-compliance. More recently, it has introduced measures relating to ESG disclosures, business responsibility reporting, and digital governance.

Kotak Committee and Recent Reforms

Recognising the need to further modernise governance standards, SEBI constituted the Committee on Corporate Governance under the chairmanship of Uday Kotak in 2017.

The Committee examined global governance practices and recommended reforms aimed at improving board effectiveness, transparency, and investor protection.

Its major recommendations included:

- Increasing the number of independent directors.

- Separation of the roles of Chairperson and Managing Director in specified listed entities.

- Enhanced disclosure requirements.

- Greater oversight of related-party transactions.

- Strengthening the role of audit and risk management committees.

- Improved participation of women on corporate boards.

- Better utilisation of technology in governance processes.

Many of these recommendations have been incorporated into the LODR Regulations through subsequent amendments. The Kotak Committee marked another important step in India's transition from rule-based compliance towards principles-based governance and board accountability.

ESG, SUSTAINABILITY AND BUSINESS RESPONSIBILITY

Corporate governance in India has undergone a significant transformation in recent years, moving beyond traditional concerns of shareholder protection and financial accountability to embrace broader issues of sustainability and stakeholder welfare. This shift reflects the growing recognition that long-term corporate success depends not only on profitability but also on responsible environmental, social, and governance (ESG) practices.

Environmental, Social, and Governance (ESG) has emerged as a key framework for evaluating corporate performance. The environmental component focuses on issues such as climate change, resource conservation, pollution control, renewable energy adoption, and carbon emissions. The social dimension assesses a company's relationship with its employees, customers, suppliers, and local communities, including labour rights, workplace diversity, human rights, and community development. Governance, the third pillar, examines board independence, executive accountability, ethical conduct, shareholder rights, and regulatory compliance.

Recognising the increasing importance of ESG, SEBI introduced the Business Responsibility and Sustainability Report (BRSR), replacing the earlier Business Responsibility Report (BRR). The BRSR requires the top listed companies in India to make comprehensive disclosures regarding their environmental impact, social initiatives, governance structures, risk management practices, and sustainability policies. This has enhanced transparency by enabling investors to assess companies not only on financial metrics but also on their commitment to sustainable development.

The Companies Act, 2013 also contributed to this broader governance framework by introducing mandatory Corporate Social Responsibility (CSR) under Section 135. Companies meeting prescribed financial thresholds are required to spend at least two per cent of their average net profits on CSR activities. Although CSR and ESG are distinct concepts, both reinforce the principle that corporations have responsibilities extending beyond wealth maximisation.

Today, institutional investors, sovereign wealth funds, and global asset managers increasingly incorporate ESG considerations into their investment decisions. Consequently, Indian companies have begun integrating sustainability into corporate strategy, risk management, and board-level decision-making. Corporate governance has therefore evolved from ensuring legal compliance to promoting responsible, ethical, and sustainable business practices.

CURRENT CHALLENGES

Despite significant reforms, corporate governance in India continues to face several challenges. Promoter dominance remains a major concern, as concentrated ownership can limit board independence and affect minority shareholder interests. The effectiveness of independent directors is also questioned, with many facing practical constraints in exercising objective oversight.

Weak board evaluation processes and delays in regulatory enforcement further reduce governance effectiveness. Additionally, technological developments such as cybersecurity, data privacy, and artificial intelligence have introduced new governance responsibilities for corporate boards.

Ultimately, while India has a strong legal framework, effective corporate governance depends not only on regulatory compliance but also on ethical leadership, robust enforcement, and a culture of transparency and accountability.

GLOBAL COMPARISON (INDIA, UK AND USA)

India's corporate governance framework has increasingly aligned itself with international standards while retaining features suited to its unique corporate environment. A comparison with the governance regimes of the United Kingdom and the United States highlights both similarities and distinctive characteristics.

The United Kingdom primarily follows a principles-based approach through the UK Corporate Governance Code. Rather than imposing rigid statutory requirements, listed companies are expected to comply with governance principles or explain the reasons for any deviation under the well-established "comply or explain" model. This approach provides companies with greater flexibility while encouraging transparency and market discipline.

In contrast, the United States adopts a more rules-based framework, particularly following the enactment of the Sarbanes-Oxley Act, 2002 in response to the Enron and WorldCom scandals. The American model imposes detailed statutory obligations concerning financial reporting, auditor independence, internal controls, executive certification, and criminal liability for corporate fraud.

India occupies a middle ground between these two approaches. While several governance requirements are mandatory under the Companies Act, 2013 and SEBI (LODR) Regulations, Indian regulators have also incorporated principles-based governance by encouraging board independence, ethical leadership, stakeholder engagement, and sustainability reporting.

A unique feature of India's governance framework is its statutory Corporate Social Responsibility (CSR) regime under Section 135 of the Companies Act, 2013. Unlike most jurisdictions, India legally requires qualifying companies to undertake specified CSR expenditure, reflecting the country's emphasis on inclusive and socially responsible economic development.

Similarly, India's adoption of Business Responsibility and Sustainability Reporting (BRSR) demonstrates its growing commitment to global ESG standards while tailoring disclosure requirements to domestic regulatory priorities.

FUTURE OF CORPORATE GOVERNANCE IN INDIA

Corporate governance in India is expected to evolve further in response to technological innovation, changing investor expectations, and increasing global integration.

One of the most significant future developments will be the deeper integration of ESG principles into corporate strategy. Investors are increasingly evaluating companies based on sustainability performance, climate-related disclosures, diversity, responsible supply chains, and ethical governance. Boards will therefore be expected to incorporate ESG considerations into long-term decision-making rather than treating them as separate compliance obligations.

Technology will also reshape governance practices. Artificial intelligence, blockchain technology, big data analytics, and digital compliance tools have the potential to improve transparency, strengthen internal controls, enhance audit quality, and facilitate real-time regulatory reporting. At the same time, boards must develop expertise in managing cyber risks, data privacy obligations, and digital ethics.

The role of independent directors is also likely to expand. Future reforms may place greater emphasis on board diversity, specialised expertise, periodic training, and objective performance evaluation to ensure that independent directors effectively discharge their oversight responsibilities.

Institutional investors, proxy advisory firms, and shareholder activism are expected to exert increasing influence on corporate governance. As ownership patterns evolve, companies will face greater scrutiny regarding executive remuneration, board appointments, related-party transactions, and sustainability commitments.

Regulators are also expected to strengthen enforcement through greater use of technology-driven supervision, forensic investigations, and coordinated regulatory action. Stronger enforcement, combined with improved governance culture, will remain essential for maintaining investor confidence.

Ultimately, the future of corporate governance in India lies in striking an appropriate balance between regulatory compliance, ethical leadership, business innovation, and sustainable value creation. Governance will increasingly be viewed not as a cost of compliance but as a strategic advantage that enhances corporate resilience and long-term competitiveness.

CONCLUSION

The evolution of corporate governance in India reflects the country's broader economic transformation from a highly regulated domestic economy to one of the world's fastest-growing market economies. What began as a system focused primarily on statutory compliance has gradually developed into a sophisticated governance framework built upon transparency, accountability, ethical leadership, and stakeholder protection.

The journey has been shaped by multiple factors, including economic liberalisation, expert committee recommendations, major corporate scandals, legislative reforms, and proactive regulatory intervention by SEBI. Milestones such as the CII Code, Clause 49 of the Listing Agreement, the Companies Act, 2013, the SEBI (Listing Obligations and Disclosure Requirements) Regulations, and the recommendations of the Kotak Committee have collectively strengthened India's corporate governance architecture.

Looking ahead, the future of corporate governance in India will be shaped by sustainability, technological innovation, ESG integration, shareholder activism, and global investment expectations. As businesses become increasingly interconnected and accountable to a wider range of stakeholders, governance will continue to expand beyond financial reporting to encompass environmental stewardship, social responsibility, digital resilience, and long-term value creation.

India today possesses one of the most comprehensive corporate governance frameworks among emerging economies. The challenge is no longer the absence of law but ensuring effective implementation, strong institutional enforcement, and a corporate culture that genuinely embraces the principles of transparency, accountability, fairness, and integrity. Only through this combination can corporate governance fulfil its ultimate objective of fostering sustainable businesses, protecting stakeholder interests, and strengthening confidence in India's corporate sector.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others