1. INTRODUCTION AND RESEARCH FRAMEWORK

1.1 Background of the Study

Corporate governance constitutes the systematic framework of rules, relationships, systems, and processes by which corporations are directed and controlled. It balances the interests of a company's many stakeholders, including shareholders, senior management executives, customers, suppliers, financiers, the government, and the community. In India, the landscape of corporate administration underwent a paradigm shift with the enactment of the Companies Act, 2013, which replaced the archaic Companies Act, 1956. This legislative overhaul sought to modernize India’s corporate ecosystem, inject transparency, protect minority investors, and align domestic frameworks with global benchmarks.

1.2 Research Problem & Objectives

Despite over a decade of operational enforcement, supplemented by structural revisions up through the Corporate Laws (Amendment) Bill, 2026, systemic failures continue to challenge the regulatory apparatus. High-profile corporate scandals underscore a persistent divergence between statutory mandates (de jure compliance) and ethical operational realities (de facto execution).

This research paper critically evaluates the structural efficacy of the corporate governance framework engineered by the Companies Act, 2013. The primary objectives are:

- To trace the historical evolution and theoretical constructs underpinning Indian corporate governance.

- To evaluate the mechanics of board institutional accountability, with a specific focus on the operational independence of independent directors.

- To assess mechanisms protecting minority interest and facilitating stakeholder democracy.

- To diagnose systemic vulnerabilities exposed by regulatory failures and draw comparative insights from international legal frameworks to suggest policy adjustments.

2. EVOLUTION OF CORPORATE GOVERNANCE IN INDIA

The trajectory of corporate governance regulations in India reflects a transition from a closed, promoter-dominated economic system to an integrated, market-driven economy.

2.1 The Pre-Liberalization Era and the 1956 Framework

Prior to the 1991 economic reforms, Indian corporate structures were heavily defined by the "promoter-led" model and state-directed capitalism. The Companies Act, 1956, focused primarily on basic procedural compliance rather than robust internal accountability. This statutory environment led to a highly concentrated shareholding matrix, where public financial institutions and family-led promoter groups dominated management networks, often leaving minority retail shareholders marginalized.

2.2 Post-Liberalization Committees

The opening of Indian markets in 1991 necessitated capital market integrity to attract foreign institutional investors (FIIs). Consequently, a series of advisory committees shaped the evolving governance architecture:

- CII Code (1998): The Confederation of Indian Industry published India’s first voluntary code of corporate governance, emphasizing board professionalism.

- Kumar Mangalam Birla Committee (1999): Constituted by the Securities and Exchange Board of India (SEBI), this committee led to the introduction of Clause 49 of the Listing Agreement, establishing the initial framework for independent directors and audit committees in listed entities.

- Naresh Chandra Committee (2002): Addressed auditor-company relationships and corporate auditing practices following global failures like Enron.

- Narayana Murthy Committee (2003): Refined the definitions of independent directors, audited financial disclosures, and risk management evaluation parameters.

2.3 Synthesis into the Companies Act, 2013

The Satyam Computer Services scandal in 2009 exposed deep vulnerabilities in accounting controls and independent oversight, accelerating the legislative push for reform. The resulting Companies Act, 2013, systematically codified corporate governance principles, transforming voluntary guidelines into mandatory statutory obligations backed by strict civil and criminal liabilities.

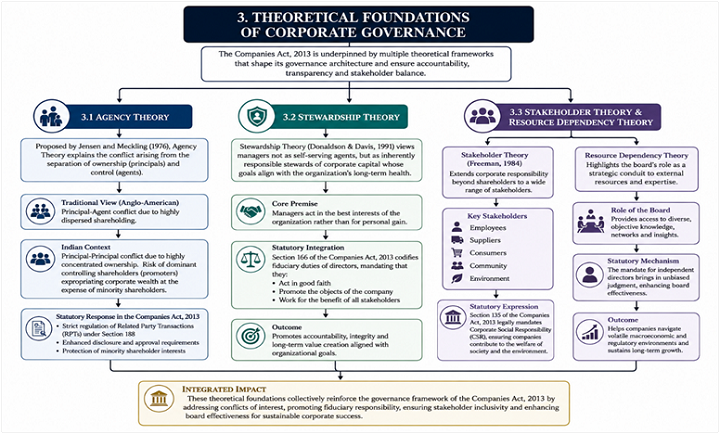

3. THEORETICAL FOUNDATIONS OF CORPORATE GOVERNANCE

To systematically assess the efficacy of the Companies Act, 2013, its provisions must be parsed through established theoretical corporate models.

3.1 Agency Theory

Pioneered by Jensen and Meckling (1976), Agency Theory posits a structural conflict of interest arising from the separation of ownership (principals) and control (agents). In Anglo-American jurisdictions, this dynamic typically manifests as a Principal-Agent conflict due to highly dispersed shareholding.

Conversely, the Indian corporate ecosystem is characterized by highly concentrated ownership. Consequently, the primary friction is the principal-Principal conflict: the risk of dominant controlling shareholders (promoters) expropriating corporate wealth at the expense of non-controlling minority shareholders. The 2013 Act addresses this through strict statutory oversight of Related Party Transactions (RPTs) and enhanced disclosure requirements under Section 188.

3.2 Stewardship Theory

Stewardship Theory (Donaldson & Davis, 1991) views managers not as self-serving agents, but as inherently responsible stewards of corporate capital whose goals align with the organization's long-term health. The 2013 Act integrates this by codifying fiduciary responsibilities under Section 166, which explicitly mandates that directors act in good faith to promote the objects of the company for the collective benefit of all stakeholders.

3.3 Stakeholder Theory & Resource Dependency Theory

Stakeholder Theory (Freeman, 1984) extends corporate responsibility beyond shareholders to encompass employees, suppliers, consumers, and the broader community. This finds clear expression in Section 135 of the Act, which legally mandates Corporate Social Responsibility (CSR).

Concurrently, Resource Dependency Theory highlights the board's role as a strategic conduit to external resources. The statutory mandate for independent directors provides companies with diverse, objective expertise, helping navigate volatile macroeconomic and regulatory environments.

4. BOARD STRUCTURE AND INSTITUTIONAL ACCOUNTABILITY

The Act reshaped board composition to establish internal checks and balances, focusing on structural independence and operational transparency.

4.1 Composition and Diversity Mandates

Under Section 149(1), every company must have a board of directors comprising individuals only, with a minimum of three directors for public companies and two for private companies.

To address historical imbalances and enhance board cognitive diversity, the Act introduced a mandatory requirement for at least one-Woman Director for all listed entities and public companies meeting specified paid-up capital or turnover thresholds. Empirical data indicates this provision has elevated gender representation across Indian boards, though some companies initially complied by appointing family members of promoters, illustrating the friction between formal compliance and true diversity of thought.

4.2 Board Committees

The regulatory architecture decentralizes board oversight into specialized committees to ensure objective, uncompromised evaluation:

|

Committee Type |

Statutory Provision |

Composition Mandate |

Primary Governance Function |

|

Audit Committee |

Section 177 |

Minimum 3 directors; Independent Directors must form a majority. |

Oversees financial reporting, controls, auditor independence, and reviews RPTs. |

|

Nomination & Remuneration Committee (NRC) |

Section 178 |

Minimum 3 non-executive directors; at least half must be Independent. |

Formulates criteria for qualifications, positive attributes, and determines executive pay. |

|

Stakeholders Relationship Committee (SRC) |

Section 178(5) |

Chaired by a non-executive director; other members decided by the Board. |

Resolves grievances of security holders, including dividend payments and share transfers. |

4.3 Evaluation Mechanisms and Internal Financial Controls

Section 134(3)(p) requires formal annual performance evaluations of the board, its committees, and individual directors. Furthermore, directors must explicitly state in their Directors’ Responsibility Statement that robust Internal Financial Controls (IFC) are in place and operating effectively. This operational requirement deters executive management from bypassing internal account controls.

5. INDEPENDENT DIRECTORS AND GOVERNANCE OVERSIGHT

Independent Directors (IDs) serve as a primary statutory check against promoter dominance and managerial overreach.

5.1 Criteria for Independence: Section 149(6)

The Act establishes a strict definition of independence designed to exclude any material pecuniary or familial relationship with promoters, holding companies, or subsidiaries.

This structural framework has been continuously tightened. For instance, the Corporate Laws (Amendment) Bill, 2026 expands the look-back period for disqualifying relationship tests to include the current financial year. It also empowers the Central Government to reduce the material transaction thresholds for legal and consulting firms, further preventing indirect financial influence.

5.2 Roles, Duties, and the Code for Independent Directors

Schedule IV of the Act delineates a comprehensive, mandatory "Code for Independent Directors." This code instructs IDs to bring independent judgment to bear on board deliberations, particularly regarding strategy, performance, risk management, and key appointments. They are also required to hold at least one exclusive annual meeting without the presence of non-independent directors or management, creating a private forum to evaluate the board’s performance and leadership.

5.3 The Conundrum of Independence: Realities vs. Statutory Intent

Despite these legal guardrails, the structural independence of IDs remains a key vulnerability in Indian corporate governance. Because promoters frequently hold controlling stakes, they retain significant influence over the appointment and reappointment processes in general shareholder meetings. This dynamic can create a subtle pressure to conform, where IDs may hesitate to voice dissent for fear of being voted out.

The Accountability Dilemma: While Section 149(12) protects IDs from liability except for acts of omission or commission occurring with their knowledge, consent, or lack of due diligence, regulatory bodies have increasingly penalized IDs for corporate malfeasance. This stricter approach has driven an increase in resignations among IDs, who face rising legal exposures without proportional operational control.

6. SHAREHOLDER DEMOCRACY AND STAKEHOLDER INTERESTS

The 2013 Act significantly advanced shareholder democracy by expanding the rights of minority investors and institutionalizing mechanisms for active engagement.

6.1 Protection of Minority Shareholders

The framework balances majority rule with the protection of minority interests through several key mechanisms:

- Class Action Suits (Section 245): Allows a specified number of depositors or shareholders to seek damages from the company, its directors, or auditors for fraudulent or ultra vires acts, bridging a significant gap in India's historical investor-protection regime.

- Oppression and Mismanagement (Sections 241-244): Empowers shareholders to petition the National Financial Reporting Authority or the National Company Law Tribunal (NCLT) if the company's affairs are conducted in a manner prejudicial to public interest or oppressive to any member.

6.2 Related Party Transactions (RPTs) and SEBI LODR Alignments

Control over Related Party Transactions is crucial for preventing controlling shareholders from siphoning off corporate assets. Section 188 mandates that RPTs outside the ordinary course of business or not at arm’s length require prior Audit Committee approval and, above specified financial thresholds, a ordinary resolution by non-interested shareholders.

To streamline compliance for larger enterprises, late 2025 amendments to the SEBI (Listing Obligations and Disclosure Requirements) Regulations transitioned RPT materiality limits from a flat INR 1,000 crore cap to a graded, scale-based framework. This change ensures that high-value transactions receive targeted scrutiny while reducing routine administrative friction.

[Prior SEBI LODR Framework] ──────> Materiality = Lower of 10% Consolidated Turnover OR Flat ₹1,000 Cr

[Modern Scale-Based Approach] ───> Scaled Slabs based on Turnover (Up to ₹5,000 Cr absolute ceiling)

6.3 Institutional Investors and Stewardship Codes

Institutional investors, such as mutual funds and insurance companies, have transitioned from passive observers into active participants in corporate governance. Guided by SEBI's Stewardship Code, institutional blocks regularly exercise their voting rights on crucial matters like executive remuneration, independent director appointments, and capital restructuring, acting as an effective market-driven check on management.

7. CORPORATE GOVERNANCE FAILURES AND REGULATORY RESPONSES

The practical efficacy of a regulatory framework is often revealed by how it responds to institutional failures.

7.1 Analysis of Systemic Scandals

- IL&FS (2018): Exposed severe deficiencies in risk assessment, complex unlisted holding-subsidiary structures, and a breakdown in credit rating mechanisms that masked a deep liquidity crisis.

- DHFL & Yes Bank (2020): Highlighted systemic weaknesses in internal financial controls, aggressive off-balance-sheet lending, and related-party diversion of funds that bypassed internal credit and audit committees.

7.2 The Role of NFRA and SFIO

In response to these failures, the government activated the National Financial Reporting Authority (NFRA) under Section 132 as an independent oversight body for the auditing profession, reducing reliance on self-regulatory models. Simultaneously, the Serious Fraud Investigation Office (SFIO) was granted enhanced statutory powers to investigate and prosecute complex corporate white-collar crimes.

To further strengthen this ecosystem, the Corporate Laws (Amendment) Bill, 2026 proposes adding Sections 132A through 132K. This expansion aims to grant NFRA independent regulation-making authority and a broader enforcement toolkit, reinforcing its capacity to maintain audit integrity.

8. COMPARATIVE JURISPRUDENCE AND INTERNATIONAL STANDARDS

Evaluating India’s regulatory framework against international benchmarks highlights both its strengths and areas for potential refinement.

8.1 Comparison with the US (Sarbanes-Oxley Act, 2002) and the UK Corporate Governance Code

The US approach, codified via the Sarbanes-Oxley Act (SOX), is highly prescriptive and rules-based, imposing strict criminal liability on CEOs and CFOs for financial misstatements. India's IFC requirements under Section 134 broadly mirror the internal control mandates of SOX Section 404.

Conversely, the UK operates under a principles-based, "comply or explain" Corporate Governance Code. This offers companies operational flexibility while relying on institutional market forces to penalize poor governance. India's framework under the 2013 Act is a hybrid model: it enforces a strict statutory baseline for all companies via the Companies Act, while applying dynamic, principles-based disclosure layers through SEBI's LODR regulations for listed entities.

8.2 OECD Principles of Corporate Governance

The G20/OECD Principles focus on ensuring a transparent and efficient market, protecting shareholder rights, and facilitating equitable treatment of all investors. India aligns well with these principles regarding disclosure transparency and minority shareholder rights. However, it continues to face practical enforcement challenges due to judicial backlogs, particularly at the NCLT level. Recent initiatives, such as the introduction of the Companies (Adjudication of Penalties) Rules, seek to address this by moving minor compliance infractions to electronic administrative adjudication, helping preserve tribunal capacity for complex corporate disputes.

9. CONCLUSION AND POLICY RECOMMENDATIONS

9.1 Synthesis of Findings

The Companies Act, 2013, succeeded in shifting the Indian corporate environment from formalistic compliance to a more robust, accountability-driven framework. The codification of directors' duties, strict regulation of related party transactions, and the introduction of independent oversight bodies like NFRA have enhanced institutional transparency and minority investor protection.

However, structural vulnerabilities persist. The primary challenge remains the structural dependence of independent directors within promoter-dominated companies, alongside the operational complexities of managing multi-tiered subsidiary structures. While ongoing updates through 2025 and 2026 have improved digital compliance and rationalized operational thresholds, addressing the underlying concentration of ownership control remains an ongoing regulatory task.

9.2 Forward-Looking Policy Recommendations

To further strengthen the efficacy of India's corporate governance framework, the following strategic interventions are proposed:

- Reforming Independent Director Selection: To insulate IDs from promoter influence, a dual-voting mechanism should be considered for listed companies. Under this model, the appointment of an ID would require approval from both the overall shareholder body and a majority of the minority retail/institutional shareholders voting independently.

- Enhancing Whistleblower Protection: While Section 177 mandates a vigil mechanism, its internal operation often fails to protect informants from professional retaliation. Implementing an independent external reporting channel managed directly by SEBI or NFRA, combined with clear financial incentives for uncovering material fraud, would improve early detection.

- Strengthening Judicial Infrastructure: The NCLT's capacity must expand to handle complex governance disputes effectively. Specializing corporate law tribunals and establishing strict timelines for corporate fraud cases would reduce delays, making provisions like Class Action suits a more reliable deterrent against corporate misconduct.

10.REFERENCES

- Government of India. The Companies Act, 2013. Ministry of Corporate Affairs.

- Securities and Exchange Board of India. SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (as amended up to 2026).

- Ministry of Corporate Affairs. The Corporate Laws (Amendment) Bill, 2026.

- Jensen, M. C., & Meckling, W. H. (1976). "Theory of the firm: Managerial behavior, agency costs and ownership structure." Journal of Financial Economics, 3(4), 305-360.

- Donaldson, L., & Davis, J. H. (1991). "Stewardship theory or agency theory: CEO governance and shareholder returns." Australian Journal of Management, 16(1), 49-64.

- G20/OECD. Principles of Corporate Governance. OECD Publishing.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others