I. Introduction: The Structural Paradox of Minority Protection

Back then, under old rules from England like Foss v. Harbottle (1843) 2 Hare 461, small investors could only watch while bigger players took control. When most owners agreed on something, the firm moved forward regardless of others' objections - those who disagreed had just one path: push for closure of the whole business. India's new Companies Act, 2013 aimed to shift this balance. Instead of forcing shutdowns, it built space for fairer fixes through sections 241 to 244. These parts connect with special courts - the NCLT and NCLAT - to give smaller stakeholders a working way out when decisions felt unfair or poorly handled.

Still, moving through 2025’s business world, people keep questioning whether these rules actually work. Though built on solid legal design, the system loses strength because of three deep flaws. One, it demands too much proof before calling something unfair. Two, small shareholders face tougher processes and higher burdens when bringing claims. Then there's precedent - specifically how the Supreme Court ruled in Tata Consultancy Services Ltd. v. Cyrus Investments Pvt. Ltd., (2021) 9 SCC 449 - which leans hard toward letting majority owners decide freely, even at the cost of fairness for others. Because of this mix, relief sits written into law yet slips away just when needed most.

II. The Statutory Architecture: Sections 241–244 and the Jurisdictional Terrain

One way to start things: under India’s Company law, regular shareholders can reach out to a special tribunal if business actions harm the public, damage corporate goals, or squeeze out individual owners. When matters go sideways, this court steps in - not just watching closely but acting directly. It might reshape how decisions get made inside the firm, place limits on moving ownership stakes around.

Agreements already signed? Those could be scrapped or changed. Legal moves using the company’s own name become possible through its approval. Most striking - it can force dominant investors to buy out others, sometimes even make smaller stakeholders absorb holdings, whichever fits fairness best.

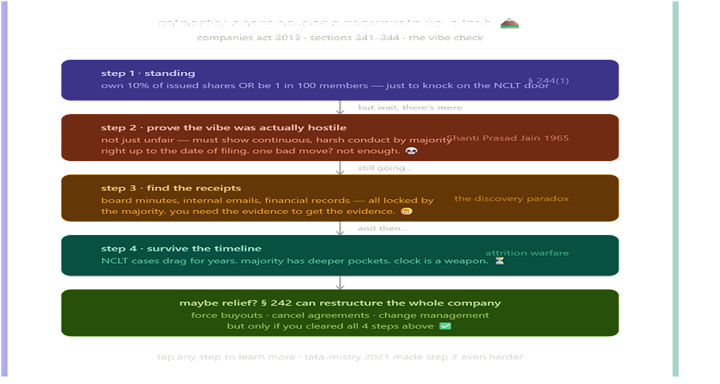

What counts as enough standing comes down to Section 244. When a company has shares, the request can come from either a hundred people on the list or one out of every ten members - whatever number turns up smaller. Another route opens for anyone who owns a tenth part of the shares already handed out.

Yet there's this: under Section 244(1)'s added note, the NCLT holds power to set those numbers aside when fairness demands it. That escape clause matters in real cases - even though courts reach for it carefully, never too quick.

One by one, these rules seem to form a wide net for protecting minority interests - at least on paper - in developing economies. What stands out is how far Section 242 reaches: it lets the NCLT reshape how a company runs, something unseen before 2013 in India’s laws. Still, the real issue isn’t just having such powers; it’s whether courts will apply them in ways that actually deliver fairness.

III. The Foundational Jurisprudence: Establishing the Threshold for Oppression

That idea of unfair treatment under India’s company rules traces back to a key court moment - Shanti Prasad Jain versus Kalinga Tubes Ltd., reported in AIR 1965 SC 1535, settled on 14 January 1965. A small shareholder claimed wrong when 39,000 fresh shares went to third parties seen as stand-ins for dominant insiders - clearly meant to weaken his stake and push out his team.

Justice Wanchoo spoke for the panel of three judges, setting a core standard at paragraph 16: needing only fair reasons to shut down the firm falls short; instead, proof must exist of ongoing harsh actions by those in power against fellow owners, stretching right up to filing day - clear evidence the business ran in ways that crushed certain shareholders’ position

Later cases kept quoting what the judges said about unfair treatment. At paragraph 19, they took wording used by Lord Cooper long ago in a Scottish ruling - Elder versus Elder and Watson from 1952. He wrote that complaints must show clear signs of dishonesty, something plainly outside normal fairness. Shareholders expect honest handling when placing trust in a firm; any breach strikes at that core idea. Since then, Indian courts have treated this as the base rule for deciding if actions are truly oppressive.

Wrongful behaviour needing proof of moral failure plus broken equity became key. In Shanti Prasad Jain, things moved further - at para 28, appeals got rejected. Fear alone by dominant owners, worried subordinates could grab power, wasn’t enough to prove harm. From there on, rulings demanded strong evidence rooted deeply in each situation’s details.

Big changes came through a court case called Needle Industries (India) Ltd. vs Needle Industries Newey. A clash arose when a foreign parent firm and local minority owners disagreed about new share issues in their shared company. Though the judges found no real unfairness - since Indian managers followed currency rules, not personal spite - they still claimed authority to fix deeper imbalances.

One key point emerged at paragraph 118: using power just to grab or keep control counts as misuse. Later, at paragraph 120, it became clear that issuing shares demands honest intent and bad motives spoil such choices. That thinking built a way to tell apart fair moves from sneaky ones - a line businesses need, yet courts often struggle to draw.

Out of sight, the managing director slipped extra shares into his own name. This happened inside a tightly bound firm, one that acted much like a shared venture between trusted parties. Back in September 2004, silence spoke louder than words when news never reached the main investor. By staying quiet, control quietly shifted hands - not by vote, but by hidden moves. A ruling came down which stated that if someone wears two hats, leader and insider, yet acts without clear reason or openness, trust cracks.

One judge put it plainly - doing so spoils fairness twice over, breaking loyalty while squeezing out others. That moment became law in 2005, printed within volume one of Supreme Court Cases at page 212. Nowhere is it fair, the judges made clear, for someone who caused harm to later purchase the victim’s stake.

That idea flipped the earlier ruling where the injured party was told to hand over their shares to the one who did wrong. Since then, courts have leaned on this stance when weighing justice under Section 242. Rarely does power tilt so sharply toward protection. The logic sticks - wrongdoing earns no ownership rights.

IV. The Tata-Mistry Moment: Corporate Autonomy vs. Substantive Minority Justice

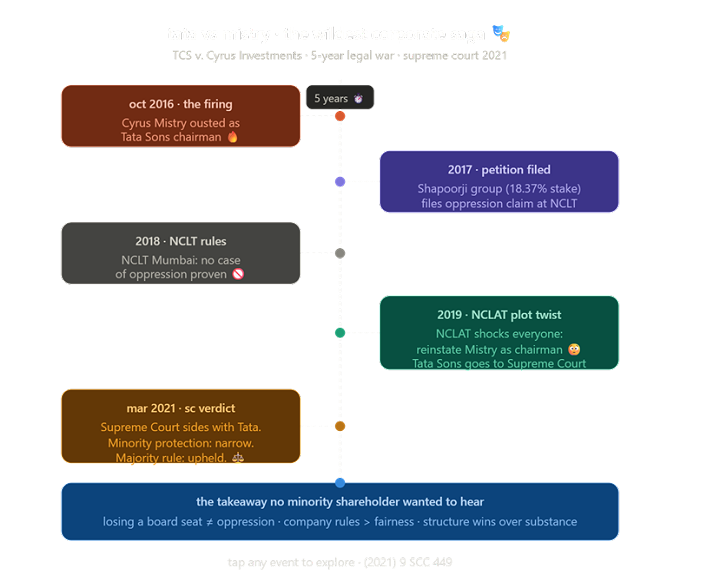

Midway through 2025, any fair look at how minorities are shielded legally must touch upon Tata Consultancy Services Ltd. v. Cyrus Investments Pvt. Ltd. That lengthy clash - sparked when Cyrus Mistry was removed as head of Tata Sons back in October 2016 - unraveled into the deepest court dive into Sections 241 and 242 since the new Company law began. Nearly five years passed between dispute start and verdict.

With roughly 18.37% ownership held by the Shapoorji faction inside Tata Sons, their complaint reached India’s corporate tribunal in Mumbai claiming unfair treatment. Suddenly judges faced thorny questions baked into company rules. What happens when a small but significant voice gets shut out quietly, not through rule breaking but silent sidelining? Does stripping influence bit by bit count as harm even if no clause is violated outright? Into that gray space stepped the judiciary.

Pages long, the Supreme Court said no to both issues, sharply limiting how Section 241 can be used. Not every time someone loses their role as chairperson or board member counts, the judges explained at paragraph 88 - only when it hurts the company, its people, or what matters to society.

Later, at paragraph 97, they added: restoring a removed chairman isn’t something Section 242 allows, wiping out a prior unusual call by NCLAT. About being treated unfairly, the court picked up where lower courts left off - losing trust in a minority nominee’s leadership skills alone?

That doesn’t equal mistreatment, per paragraph 134. Being on the board brings one set of powers; owning shares gives another, the bench noted plainly in paragraph 93 - ending that job does not mean your voice as an owner gets crushed

It stands firm on several legal points, yet the top court’s reversal of NCLAT’s odd decision to reinstate sparked valid concerns. What draws scrutiny is how tightly the ruling sticks to following the company’s rulebook, ignoring whether those rules themselves keep smaller shareholders at bay.

When power leans heavily on documents written by the dominant party, fairness risks vanishing behind legality. Protection for minority voices becomes limited strictly to what the founding papers spell out - nothing more. That tight interpretation of Section 241 may let hidden forms of dominance slip through unnoticed. Structure wins over substance when actions fit within self-made boundaries.

V. The Procedural Labyrinth: Structural Disadvantages of the Minority Petitioner

Just clearing the first legal hurdle barely scratches the surface. How these cases move through courts often tilts against smaller stakeholders. Three deep flaws show up every time. Starting with lopsided knowledge - those bringing claims rarely see company emails, meeting notes, or financial records vital to their argument.

Those documents stay locked down by dominant owners, leaving others to build early proof using whatever’s public. Which creates a twist: you need hidden facts to win, but can’t get them without already showing cause.

Later on, court cases under NCLT often drag on for many years - slowly wearing down those involved. Because of this, dominant owners with deeper pockets tend to come out ahead in fights over control. Then again, one bigger issue comes from the rule set by Shanti Prasad Jain: single acts of misuse, even if clearly unjust, rarely count without ongoing patterns.

To prove such a pattern exists and show bad intentions behind decisions, insiders need records from company boards. Yet these papers stay locked away before any investigation begins. So the proof needed sits just beyond reach, blocking the fix it would enable.

VI. New-Age Vulnerabilities: Start-Ups, Private Equity, and ESG Activism

Out in the open, those earlier flaws grow sharper when new kinds of businesses come into play. Not your usual firms - these are startups backed by venture money or shaped by private equity, built on dense shareholder deals few can untangle. Hidden inside? Drag-along clauses, payout priorities, shields against share loss, access to insider data - all stacking power so founders, especially small ones, get left behind.

Trouble shows up fast here, yet old legal tools like Sections 241 to 244 don’t quite reach it. Control isn’t always held by a dominant owner; sometimes it's an expert-level investor pulling strings. Their moves might feel aggressive, even one-sided, but rarely match the raw unfairness seen in past cases like Shanti Prasad Jain.

Looking at how things like climate, fairness, and leadership shape investing reveals fresh ways small owners push back. Pension providers, green-focused funds, plus advisory groups now question choices around environmental risks or deals between insiders.

Rules set by SEBI offer some safety for smaller players in public firms - big decisions need wide agreement - but those outside the stock markets face tougher odds. Information gaps hit harder there, leaving little room to walk away. Independent board members were meant to balance power under Section 149 and its guidelines, yet the clash between Tata and Mistry showed these roles often tilt toward whoever holds control. Even people picked to stay neutral may act loyal only to dominant figures if appointments come from them.

VII. Judicial Trends and the NCLT's Evolving Approach

Even though the case of Tata and Mistry set limits, the NCLT and NCLAT have shaped subtler legal views after 2021. By 2024 and 2025, in multiple rulings, these courts began looking past surface-level compliance to check if majority moves actually harm minorities when taken together.

Watchfulness grew especially sharp where: issuing rights shares in ratios meant to push small owners under Section 244’s limit - a move now often seen as serving outside goals per Needle Industries; approving deals with linked parties on unfair terms that shift worth from private firms to dominant groups; blocking minority holders repeatedly from accessing info they should get under company rules.

Now courts allow more leeway when skipping strict standing rules under Section 244(1)'s exception. Judges see clearly that rigid checks block valid cases without ever reviewing their core. Good thing too - lawmakers built in that escape hatch knowing fairness might demand it. Opening the door wider fits how Chapter XVI aims to fix wrongs, not pile on hurdles.

VIII. Reforming the Framework: What a Robust 2025 Regime Requires

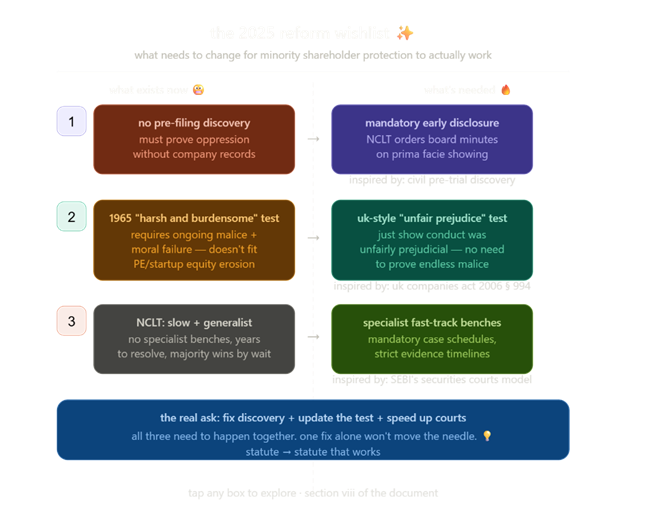

For the minority shareholder safeguards in the Companies Act, 2013 to actually work, changes need to happen in three areas at once. Instead of just sounding good on paper, the system has to shift how proof is gathered.

One way forward: let the NCLT require companies to release board records and internal messages early, if there’s even a hint of unfair treatment - much like what happens before a lawsuit formally begins. Right now, small shareholders have to piece together evidence without access, which makes fair outcomes nearly impossible. Because they’re locked out from the start, real justice can’t take root.

Nowadays, the legal test for oppression needs updating. Harsh, burdensome, wrong - that old description from Shanti Prasad Jain worked when ownership was simple. Yet it struggles with today’s stealthy equity erosion techniques. Private equity moves fast.

Shareholder deals now twist power quietly behind closed doors. A better fit might come from Britain’s approach under Section 994. Their rule asks only if company actions harm some shareholders unfairly. Proving endless malice isn’t needed. Not abandoning past wisdom here. Just honoring what the law meant to do all along.

Start by upgrading the NCLT’s core structure - specialized panels focused on company oversight could shift how cases unfold. Instead of long waits, faster schedules for handling unfair treatment claims might change outcomes entirely. Early meetings to outline each case step should happen without exception. Limiting how much time parties get before sharing evidence may stop delays from building up.

On another note, widen what SEBI demands companies disclose when deals occur off public markets. That extra transparency can shrink the knowledge gap dominant owners now hold in venture-backed and private investment spaces.

IX. Conclusion: The Distance Between Statute and Justice

Little has changed by 2025 for minority shareholders in India, despite strong laws on paper. Though the Companies Act, 2013 arms them with tools like Sections 241 to 244 - some of the widest safeguards anywhere - the courts rarely deliver. Past rulings shape what happens now: back in 1965, Shanti Prasad Jain demanded proof of ongoing unfair behavior; later, Needle Industries in 1981 insisted actions must serve proper aims only. Jump ahead to 2005, when Dale & Carrington said oppressed minorities can force buyouts.

Then came 2021’s Tata Consultancy Services case, favoring dominant owners once more. Each step forward seems met with resistance in practice. Proof needed is heavy, court waits stretch long, judges still hesitate to challenge majority control. So those very powers meant to shield small investors often sit unused. Reality bends away from promise.

Far from suggesting minority investors should dodge every tough outcome, the system still leans on majority votes as its backbone. Yet courts stepping into everyday company choices would wreck the speed businesses need to function well.

What matters now is whether current laws - how they’re read and applied today - actually keep dominant owners in check through real oversight. Truthfully, right now, that deterrent rarely works without high expense or uncertainty. Unless proof standards shift, unless fairness benchmarks are clarified, unless court systems gain strength, safeguards for smaller stakeholders may stay just out of reach - like so many times before, more illusion than reality.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others