Introduction

One of the most misunderstood aspects of writ jurisdiction under Article 226 is not its scope, but its timing. The power of judicial review is undeniably wide, yet courts have consistently emphasised that the exercise of this power must be disciplined. The question is not simply whether a grievance exists, but whether the stage at which the court is approached is appropriate.

The Supreme Court’s order in M/s Trillion Lead Factory Pvt Ltd v Superintendent of Central Tax is a direct reaffirmation of this principle. The Court refused to entertain a challenge to a show cause notice proposing cancellation of GST registration. It held, without ambiguity, that such challenges are premature and not maintainable in the ordinary course.

At first glance, the order appears brief. However, its brevity is precisely what makes it important. The Court did not feel the need to elaborate because the principle involved is already settled. That in itself sends a strong message. Courts are not inclined to reopen foundational doctrines every time they are tested. Instead, they are reinforcing them through consistent application.

In the GST context, where regulatory actions often have immediate commercial implications, assessees frequently attempt to invoke writ jurisdiction at the earliest stage to prevent potential adverse outcomes. This ruling indicates that unless the case fits within specific exceptions, such tactics will not be successful. It emphasises procedural discipline once more and demands adherence to legal procedures.

Factual Background

The facts of the case follow a pattern that is increasingly common in GST litigation. The petitioner, a private company, came under scrutiny for what the tax authorities described as excessive or “huge” availment of input tax credit. This is one of the most litigated areas under GST, given its direct impact on tax liability and revenue.

The jurisdictional proper officer initiated a series of communications with the petitioner. What appeared here wasn’t just a onetime notice and the same formed part of a continuing review process. Instead of a single request, multiple queries reached the petitioner about how they justified their claim for input tax credit. Clearly, proceedings had not yet moved into formal judgment and rather, officials were collecting details to decide if deeper steps made sense.

Last year, the petitioner submitted its reply. The core of its defence was that the issue had already been examined by the Directorate General of GST Intelligence. It argued that initiating proceedings again on the same issue amounted to duplication and harassment. This is a strategic defence often raised in tax matters, especially where multiple wings of the department are involved.

Despite this reply, the petitioner anticipated coercive action. It approached the High Court under Article 226, seeking protection against possible adverse measures. Last year in october, the High Court granted interim relief, directing that no coercive action be taken.

However, the administrative process did not stop. On 17 December 2025, the proper officer issued a formal show cause notice proposing cancellation of the petitioner’s GST registration. This was a significant development. The matter moved from inquiry to adjudication. The petitioner was now formally required to show cause why its registration should not be cancelled.

The petitioner responded with a detailed reply to the notice. At this stage, the statutory process was fully engaged. The authority was expected to consider the reply and pass a reasoned order.

Instead of allowing this process to conclude, the petitioner continued with the writ proceedings. The High Court eventually dismissed the petition, holding that it was not maintainable at the show cause stage. The petitioner then approached the Supreme Court.

Can Courts Intervene Before a Decision is Made?

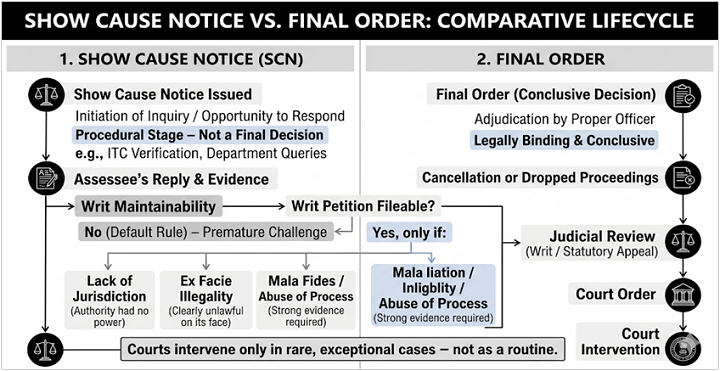

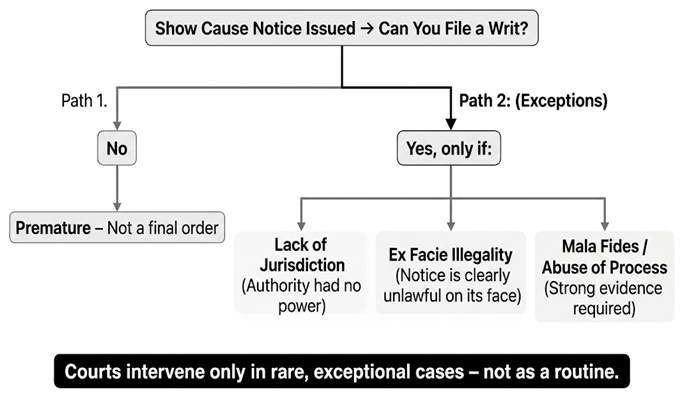

The legal issue before the Supreme Court was not complex in formulation, but it had significant implications. The question was whether a writ petition can be entertained against a show cause notice in GST proceedings, particularly where the notice proposes cancellation of registration.

This issue goes beyond tax law. It is rooted in administrative law and concerns the nature of judicial review itself. A show cause notice is not a final determination. It is a procedural step that precedes adjudication. It does not impose liability or alter rights. It merely calls upon the noticee to explain.

The petitioner’s approach was essentially anticipatory. It sought to prevent the possibility of an adverse order by challenging the notice itself. This raises a fundamental concern. If courts were to entertain such challenges routinely, administrative authorities would be unable to complete their functions. Every notice could become a potential subject of litigation, leading to paralysis of the system.

The law, therefore, requires a balance. While individuals must be protected from arbitrary action, administrative processes must also be allowed to function. The doctrine of non-interference at the show cause stage is an attempt to maintain this balance.

Supreme Court’s Reasoning

The Supreme Court dealt with the matter in a concise manner. It observed that it is “trite law” that no writ lies against the issuance of a show cause notice. The Court relied on two established precedents: Secretary, Ministry of Defence v Prabhash Chandra Mirdha and Commissioner of Central Excise v Krishna Wax (P) Ltd.

In Prabhash Chandra Mirdha, the Court had held that interference at the stage of show cause notice is not justified unless the notice is issued without jurisdiction or is otherwise wholly illegal.

The Court emphasised that the noticee must respond to the notice and that courts should not pre-empt the adjudicatory process. Similarly, in Krishna Wax, the Court reiterated that writ jurisdiction should not be invoked to challenge notices that merely initiate proceedings.

By relying on these decisions, the Supreme Court in the present case reaffirmed that the principle is settled. The Court did not find any exceptional circumstance that would justify deviation. The notice was issued by a competent authority. It was preceded by communications. The petitioner had been given an opportunity to respond and had in fact submitted a reply.

In these circumstances, the Court held that the High Court was correct in dismissing the writ petition. It concluded that the Special Leave Petition was liable to be rejected in limine.

Why Courts Avoid Interference at This Stage

The refusal to interfere at the show cause stage is not based on technicality. It is grounded in a clear understanding of how administrative decision-making works. A show cause notice serves two purposes. First, it informs the affected party of the allegations against it. Second, it provides an opportunity to respond. It is a safeguard built into the system. Treating it as a final action would defeat its purpose.

If courts were to intervene at this stage, they would effectively replace the authority’s role. They would be required to examine facts, assess evidence and decide issues that are meant to be considered by the authority in the first instance. This would blur the distinction between adjudication and judicial review.

There is also a practical concern. Administrative authorities deal with large volumes of cases. Allowing writ petitions at the notice stage would flood courts with premature challenges. It would delay proceedings and increase the burden on the judicial system.

The doctrine therefore ensures that the process is respected. The noticee must first participate in the proceedings. If the final order is adverse, it can then be challenged. This sequence preserves both fairness and efficiency.

Heightened Importance of Procedural Discipline

The GST framework makes the doctrine of non-interference at the show cause stage even more critical than in ordinary administrative law contexts. This is because GST is not merely a tax statute, but a compliance-heavy, transaction-driven regulatory system where liability is determined through layered verification.

Unlike traditional tax regimes where assessments were periodic and often retrospective, GST operates in near real-time, relying on returns, matching mechanisms, and digital records. This structural shift means that disputes, especially those relating to input tax credit, are deeply fact-intensive and cannot be meaningfully resolved without detailed examination at the administrative level.

In the present case, the allegation concerned “huge availment” of input tax credit. This is not a legal conclusion that can be tested in abstraction. It requires scrutiny of invoices, supplier compliance, transaction trails, and statutory eligibility conditions under the CGST Act. The adjudicating authority is expected to undertake this exercise, not the writ court. If the court were to intervene at the notice stage, it would either have to assume facts or engage in a fact-finding exercise, both of which fall outside the traditional boundaries of writ jurisdiction.

Further, cancellation of GST registration is not an automatic or mechanical consequence. It follows a defined statutory pathway. The issuance of a show cause notice is itself a procedural safeguard. It ensures that the assessee is not taken by surprise and is given an opportunity to respond before any adverse action is taken. Treating such a notice as an actionable wrong undermines its very purpose.

There is also a systemic dimension to this issue. GST administration involves a large number of taxpayers and continuous monitoring of compliance. If writ courts begin entertaining challenges at the notice stage as a matter of routine, the entire enforcement mechanism would be slowed down. Authorities would be unable to complete proceedings, and disputes would shift prematurely to constitutional courts. This would not only burden the judiciary but also create uncertainty in tax administration.

The Supreme Court’s approach in this case preserves the internal logic of the GST system. It ensures that disputes are first tested within the statutory framework, where facts can be properly evaluated. Only after a final order is passed does the question of judicial review arise in a meaningful way. This sequencing is not merely procedural; it is essential to the functioning of the regime itself.

The Parallel Proceedings Argument

A common problem in tax disputes is the possibility of multiple probes when someone brings up an earlier inquiry conducted by the Directorate General of GST Intelligence. Indeed, when you consider the concept, it makes logic. One matter caught between two probes might mean repeated actions, clashing results, awkward pressure. Still, courts won’t shut down a case just because another look is happening elsewhere. The fact alone isn’t enough to stop things before they start.

Timing trips up the petitioner’s case. Since someone says the matter was looked into before, that needs checking. Was it the exact same deals under review last time? Did the first probe actually reach firm conclusions? Is what is happening now a repeat - or just adding detail? Answers cannot come from guesses. They rely on documents, evidence, real boundaries drawn by different agencies’ power to act.

Right now, nothing has been settled when it comes to the show cause notice. Examination of the petitioner's response hasn’t happened yet by the officer in charge. With that chance on hand, the person can submit every piece of needed information, even facts about earlier checks said to exist. Only after all this does the deciding body need to think carefully and write down their conclusions.

A sudden move by the court now would skip ahead, jumping past established steps. Without a clear set of facts or any explanation from the agency, judgment on copying becomes guesswork. That kind of leap is exactly why courts stay out until later.

One thing to keep in mind - separate parts of the tax office often work in their own areas, doing distinct jobs. Just because DGGI is looking into something doesn’t stop a local officer from acting too. What matters is if both actions cover the same ground. Only once the details are reviewed will that become clear.

Skipping straight to the top court won’t help if earlier chances were missed. Help still exists down the line. Should the deciding body brush off key points too quickly, that ruling can later face review. Only then does deeper scrutiny become possible. Jumping ahead was what got turned away here.

Implications for Litigation Strategy

This judgment forces a reconsideration of how GST disputes are approached, particularly from the perspective of litigation strategy. Over time, there has been a growing tendency among assessees to invoke writ jurisdiction at an early stage, often immediately after receiving a show cause notice.

The underlying logic is to avoid the risk of an adverse order and the consequences that may follow, such as cancellation of registration or recovery proceedings. However, this approach is increasingly being discouraged by courts.

The present decision reinforces that writ jurisdiction is not an alternative to the statutory process. It is a supervisory mechanism that comes into play after the process has been completed or where it is fundamentally flawed. This has practical consequences. Assessees can no longer treat the reply to a show cause notice as a preliminary step before approaching the High Court. Instead, that reply becomes the central stage of the dispute.

A well-prepared reply must address both facts and law. It must provide supporting documentation, address the accusations in depth, and present all relevant defences. At this point, arguments including lack of jurisdiction, duplication of processes, or lack of factual basis must be explicitly stated. If these points are not raised before the authority, it becomes difficult to introduce them later.

From a practitioner’s perspective, the judgement also calls for greater discipline in assessing the maintainability of writ petitions. Filing a writ petition against a show cause notice should not be the default response. It should be reserved for cases where there is a clear jurisdictional error or a patent illegality. Otherwise, such petitions are likely to be dismissed at the threshold, as seen in the present case.

Tax officials are similarly affected by the judgement. Tax officials are similarly affected by the judgement. Since courts are reluctant to step in too soon, authorities are under more pressure to undertake just and lawful actions. Furthermore, notifications must be precise and understandable.

In addition to that they must also comply with the law in place. Commands must be well-founded, and responses must be properly evaluated. The absence of early judicial scrutiny does not indicate a lack of accountability rather, it merely modifies the point at which such inspection occurs.

The ruling essentially forces all parties involved to return to the legal framework. It reinstates the adjudicatory process's precedence and restricts the writ courts' authority to circumstances in which intervention is truly necessary.

When Courts Get Involved During the Show Cause Phase

Even if the Supreme Court upheld the general prohibition against interference in this case, it is as critical to comprehend the specific but significant exceptions to this rule. Refusing to consider writ petitions during the show cause phase is not a strict prohibition. Courts have, in carefully defined circumstances, stepped in even before an adjudication is completed. What this judgment makes clear is that those circumstances must be real, demonstrable, and not merely asserted.

The most well-recognised exception is where the notice is issued without jurisdiction. This goes to the root of the matter. If the authority issuing the notice lacks the legal power to do so, the entire proceeding becomes void. In such cases, requiring the noticee to participate in the process would serve no purpose. Judicial intervention is justified because the process itself is fundamentally flawed from inception.

A second category involves cases where the notice is ex facie illegal or based on allegations that are patently absurd. This is a higher threshold than mere disagreement with the contents of the notice. The illegality must be apparent on the face of the record. Courts are cautious in applying this exception because it requires them to form a prima facie view without a full factual record. As a result, this ground is invoked successfully only in rare situations.

There is also a third, less frequently applied exception, where the proceedings are demonstrably abusive or initiated in bad faith. This requires strong evidence of mala fides or misuse of power. Mere allegations of harassment or duplication, without substantiation, are not sufficient. Courts insist on clear material before invoking this ground.

The petitioner in this instance tried to rely on the claim of duplication resulting from earlier DGGI investigations. However, the Court's unwillingness to step in suggests that such a claim does not satisfy the criteria necessary to initiate an exception in the absence of thorough factual support at the threshold stage. The Court determined that the adjudicating body was the proper forum for preliminary investigation after the petitioner had the chance to present this material to them.

This aspect of the judgment is particularly instructive. It makes it clear that using exceptions to the non-interference rule as a tactic to get around the legal procedure is not acceptable. They are not early adjudication processes, but rather protections against blatant illegality. The Court has preserved the doctrine's purity while maintaining its flexibility for truly rare circumstances by refusing to expand these exclusions.

Practically speaking, this implies that when claiming writ jurisdiction at the notice stage, petitioners need to be much more specific. It is not enough to allege inconvenience or potential prejudice. There must be a clear legal defect that strikes at the root of the proceedings. Absent that, the expectation remains that the party will participate in the process and raise all available defences before the authority itself.

Conclusion

The decision in M/s Trillion Lead Factory Pvt Ltd v Superintendent of Central Tax ultimately turns on a simple but important idea: courts must intervene at the right time, not at the earliest possible time. Judicial review is not designed to anticipate every potential illegality. It is meant to address concrete grievances that arise from completed or substantially progressed processes.

By dismissing the Special Leave Petition, the Supreme Court has reaffirmed that a show cause notice does not give rise to such a grievance. It is an invitation to respond, not a determination of liability. Treating it as a final action would distort the structure of administrative law and undermine the role of statutory authorities.

The judgment also reflects a broader judicial philosophy. Courts are increasingly conscious of the need to maintain institutional boundaries. Administrative authorities are expected to perform their functions, and courts are expected to review their decisions, not replace them. This division of roles is essential for the efficient functioning of the legal system.

In the GST context, where disputes are frequent and often complex, this approach provides much-needed clarity. It discourages premature litigation and encourages engagement with the statutory process. It also ensures that courts are approached with fully developed disputes, supported by factual findings and reasoned orders.

What emerges from this decision is not a new principle, but a reaffirmation of an old one. Yet, in the current landscape of aggressive litigation strategies, that reaffirmation carries weight. It reminds litigants that not every administrative action is immediately justiciable. It reminds courts to exercise restraint. And it reinforces the idea that the law must be allowed to take its course before it is challenged.

That, in essence, is the discipline that this judgment restores.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others