The Karnataka High Court has as of late tended to a address that has taken on basic significance in India’s advancing charge requirement scene. The Court held that custodial cross examination is not an programmed prerequisite in cases including affirmed avoidance of Products and Administrations Assess where the statute endorses detainment of up to five a long time.

The choice, which emerges from a case including charged avoidance of roughly thirty one crore rupees, accentuates that statutory discipline must educate the legal work out of watchfulness in choosing whether custodial cross examination is essential. The High Court made clear that whereas financial offenses are genuine, individual freedom must stay secured unless there are compelling realities to legitimize custodial cross examination. This article investigates the lawful foundation, statutory system, protected standards, and procedural suggestions of this administering in detail.

The Statutory System for GST Offences

India’s GST system, set up by the Central Merchandise and Administrations Assess Act, mixes administrative assess collection with criminal requirement measures. The objective of the GST administration is to bind together circuitous assess structures into a single comprehensive assess, diminish compliance burdens, and anticipate cascading charge impacts.

Master Insolvency and Bankruptcy Code IBC Certificate Course by Adv. Amrita Kharkar. Enroll Now!

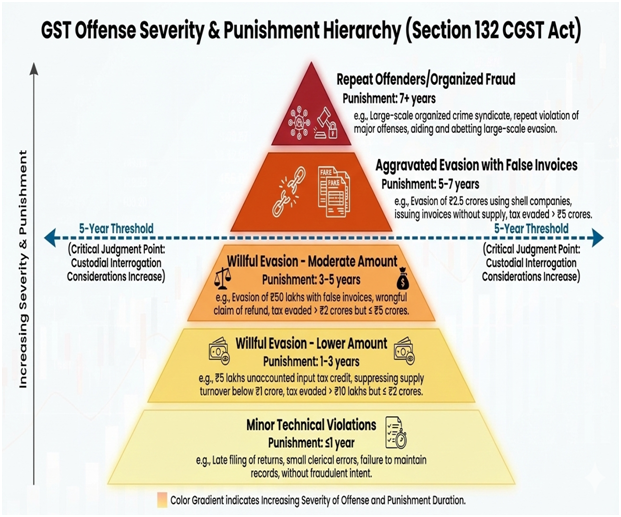

The Act moreover perceives that assess avoidance and false hones can have a destructive impact on income collection and financial decency. To address these concerns, Parliament included criminal sanctions in Section 132 of the CGST Act for certain categories of terrible conduct, such as wilful avoidance of assess, issuance of untrue solicitations, and false profiting of input assess credit.

Under Section 132, the assembly has made changing levels of discipline depending on the particular offense and the sum of charge charged to have been sidestepped. For a few offenses, the most extreme term of detainment is capped at five a long time. For other, more irritated circumstances including higher sums or more genuine conduct, discipline may surpass five a long time.

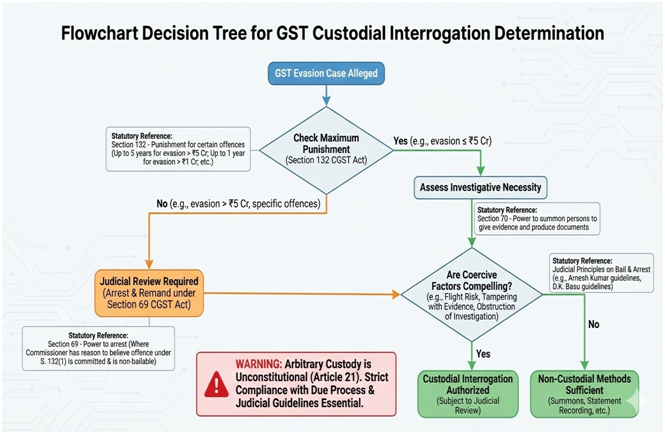

These qualifications are noteworthy since they reflect an inner authoritative judgment on the relative gravity of diverse sorts of assess wrongdoing. Sections 69 and 70 of the Act oversee capture and examination in connection to all offenses beneath this statute, counting the necessity that capturing specialists must have “reasons to believe” based on valid fabric some time recently continuing with capture.

Constitutional Shields and Individual Liberty

The Structure of India cherishes individual freedom as a essential right beneath Article 21. This right incorporates security against subjective or unjustified detainment. Over decades of law, the Preeminent Court has fortified the recommendation that capture and custodial cross examination are not inescapable results of each offense only since the law permits them.

A custodial environment fundamenHighy chills individual freedom and dangers the work out of coercive powers by the state unless rigid shields are watched. Capture, whereas legal in cognizable non-bailable offenses, must be went with by a appropriate appreciation of protected securities counting the right to be educated of the grounds of capture, get to to direct, and legal audit where fitting. These shields are not scholarly formalisms but viable securities planning to anticipate mishandle of state control and wrongful hardship of freedom.

Economic offenses, counting charge avoidance, involve a nuanced space in this scene. On one hand, the social and financial costs of large-scale avoidance require strong requirement. On the other hand, the prove in most charge avoidance cases is narrative or electronic, including solicitations, returns, bank records, and advanced filings.

Not at all like rough violations where prompt cross examination may be advocated on security grounds, financial offenses frequently do not include unmistakable, perishable prove that can as it were be secured through custodial cross examination. This refinement advises the legal approach to safeguard and care in charge matters.

Facts and Procedural Pose in the Karnataka High Court Case

In the case of Sri Akram Pasha v. Senior Intelligence Officer some time recently the Karnataka High Court, the Directorate of Central GST had started procedures against the solicitor for affirmed avoidance of GST producing to over thirty one crore rupees. The charge sheet charged offenses beneath Section 132 of the CGST Act, particularly offenses where the most extreme endorsed discipline did not surpass five a long time. Taking after capture, the solicitor looked for safeguard from the High Court, contending that custodial cross examination was not obligatory for such offenses.

The petitioner’s advise fought that since the statutory discipline was restricted, custodial cross examination might not be treated as a essential investigative step in each case. The High Court concurred with this position, giving safeguard and accentuating that custodial cross examination must be defended by particular realities on the ground, not assumed on account of the financial nature of the offense.

The Court’s Thinking on Safeguard and Custody

The Karnataka High Court stated that the statutory run of discipline is a key figure in deciding both the gravity of an offense and the require for custodial cross examination. In offenses where Parliament has capped discipline at detainment up to five a long time, the Court contemplated that custodial cross examination cannot be treated as an suggested need.

The administrative system itself demonstrates degrees of earnestness, and courts must regard that calibration when considering hardship of freedom. The High Court’s thinking places a premium on statutory elucidation nearby sacred assurances.

In giving safeguard, the High Court moreover watched that custodial cross examination is not a statutory right in cases beneath the CGST Act. Examining specialists may select to issue summons or look for intentional participation, but detainment cannot be programmed indeed in genuine financial offense examinations unless particular reasons legitimize it.

The nonattendance of substantial hazard components, such as risk of prove altering, flight hazard, or obstacle of examination, weighed in support of the accused’s freedom. The Court clarified that financial offenses are not resistant from freedom assurances basically since they affect open funds.

Comparative Statute on Care in Financial Offense Cases

The Karnataka High Court’s administering fits inside a broader legal slant that accentuates cautious utilize of care in financial offense indictments. Other High Courts have hooked with comparable issues in GST and related charge things. In a GST input assess credit extortion case in the Calcutta High Court, the Court held that capture and custodial cross examination were unbalanced where the applicant had participated completely with the examination, postured no flight hazard, and where essential prove was narrative in nature.

In that case, the Court watched that the exploring organization fizzled to follow to statutory rules and needed new implicating fabric some time recently making an capture. The Calcutta High Court allowed safeguard and remanded the denounced to coordinate with examination exterior of guardianship.

Similarly, in other purviews courts have perceived that custodial cross examination is not an inalienable component of GST examinations. In a Karnataka High Court case including false availment of input assess credit where the statutory discipline was up to five a long time, the Court permitted expectant safeguard on grounds that custodial cross examination was not one or the other justified by the statute nor essential for compelling examination.

The Court in that matter underscored that the reason of GST authorization is assess collection and compliance or maybe than correctional care, and that coercive detainment might unfavorably affect commerce interface without progressing the investigatory handle.

In differentiate, a few High Courts have communicated caution in other sorts of financial or specialized offenses, noticing that custodial cross examination may be vital in particular settings, such as cyber financial wrongdoing, where the advanced measurable component is complex and where suspects may conceal key data exterior of care.

The Karnataka High Court itself has watched in an irrelevant cyber wrongdoing setting that custodial cross examination may be required to reveal the full degree of information robbery when suspects deny to participate. These qualifications highlight that the need of guardianship depends on realities, not on categorical presumptions based on offense sort.

A choice from the Punjab and Haryana High Court in another GST matter emphasized that safeguard is not consequently denied fair since an allegation includes grave financial offenses. In that case, the High Court watched that where prove is narrative or electronic and the accused’s conduct does not show chance of altering, safeguard may be suitable. This approach adjusts with the Karnataka High Court’s thinking in treating freedom as the run the show and care as an exemption.

Constitutional and Procedural Implications

The Karnataka High Court’s choice is noteworthy for its reaffirmation that custodial cross examination must be advocated by need and educated by statutory discipline edges. This rule regards the protected security of individual freedom beneath Article 21 and the procedural shields implanted in the Code of Criminal Strategy and in extraordinary statutes such as the CGST Act. Examiners must fastidiously archive reasons for capture and care, and courts must examine these reasons or maybe than acknowledge custodial cross examination as a default investigative technique.

The judgment moreover has down to earth suggestions for how GST examinations are conducted. Examining offices are reminded that deliberate participation, statutory summons, and non-custodial addressing can frequently suffice to secure prove, especially where the assess obligation and evidentiary materials are essentially narrative. A nuanced approach to care energizes adjust between requirement viability and regard for individual liberty.

This administering ought to too impact prosecutorial technique. Charge requirement specialists must hone the truthful premise for looking for custodial cross examination. Cover attestations around reality or potential avoidance size will no longer legitimize programmed guardianship where the statutory discipline does not surpass indicated limits. The Court’s accentuation on statutory calibration welcomes a more taught and prove tied down approach to conjuring coercive powers.

Broader Legal Patterns and Future Litigation

The Karnataka High Court’s administering joins a line of legal considering over High Courts that underscores freedom where statutory discipline and investigatory realities do not legitimize custodial cross examination. These legal patterns reflect a developing understanding that financial offense indictment must be compelling and reasonable at the same time. Whereas assess avoidance and false hones harm open funds, they do not intrinsically require custodial detainment unless there is particular prove that care will substantially progress examination or anticipate injustice.

Future case concerning GST offenses and custodial cross examination will likely lock in more profound examinations of investigative records, narrative prove, flight hazard, hazard of altering, and other concrete variables or maybe than wide presumptions approximately offense gravity. Requests in such things may turn on nuanced evaluations of investigatory fabric, statutory elucidation of Sections 69, 70, and 132 of the CGST Act, and protected safeguards.

This advancing statute reflects broader sacred values. Care and detainment are coercive rebellious. Their work out must be corresponding, advocated, and firmly bound to evident need. Judiciary’s part in administering custodial choices in financial offenses strengthens the division of powers and reaffirms the run the show of law in the confront of effective authorization offices.

Conclusion

The Karnataka High Court’s decision that custodial interrogation is not mandatory in GST evasion cases punishable with imprisonment up to five years provides essential guidance for Indian criminal procedure. By grounding its reasoning in statutory punishment thresholds, constitutional protections under Article 21, and the factual matrix of economic offence investigations, the Court has reaffirmed the primacy of personal liberty in criminal justice.

The ruling aligns with judicial trends across jurisdictions that emphasise careful assessment of custody rather than presumption of detention. Investigating agencies and courts are now directed to rely on documented necessity rather than categorical assumptions. This development marks a critical point in the jurisprudence of economic offences and procedural fairness in India.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :others