Index of Headings

- Background: IEEPA and the Tariff Regime

- The Cases That Reached the Supreme Court

- The Constitutional Foundation: Congress Holds the Purse

- The Statutory Question: What Does Regulate Actually Mean?

- The Major Questions Doctrine

- The Dissent

- What the Ruling Does and Does Not Cover

- Aftermath: The Administration's Response

- FAQs

1. Background: IEEPA and the Tariff Regime

Shortly after beginning his second term, President Donald Trump moved aggressively on trade. He sought to address two foreign threats: the influx of illegal drugs from Canada, Mexico, and China, and what he described as "large and persistent" trade deficits. He declared a national emergency as to both, deeming them "unusual and extraordinary" threats, and invoked his authority under the International Emergency Economic Powers Act (IEEPA) to respond.

Enacted in 1977, IEEPA gives the President economic tools to address significant foreign threats. When acting under IEEPA, the President must identify an "unusual and extraordinary threat" to American national security, foreign policy, or the economy, originating primarily outside the United States, and must declare a national emergency under the National Emergencies Act.

On the drug trafficking side, the President imposed a 25% duty on most Canadian and Mexican imports and a 10% duty on most Chinese imports. On the trade deficit side, the so-called "reciprocal" tariffs imposed a duty on all imports from all trading partners of at least 10%, with dozens of nations facing higher rates.

These duties, often referred to as the "Liberation Day" tariffs, were announced in April 2025. The administration's position was sweeping: it argued it could use IEEPA to impose tariffs on imports from any country, of any product, at any rate, for any amount of time, as long as the President declared a national emergency.

The modifications that followed were rapid and far-reaching. One month after imposing the 10% drug trafficking tariffs on Chinese goods, the President increased the rate to 20%. Less than a week after imposing the reciprocal tariffs, he increased the rate on Chinese goods from 34% to 84%, and the very next day raised it further to 125%. This brought the total effective tariff rate on most Chinese goods to 145%.

2. The Cases That Reached the Supreme Court

Two separate legal challenges eventually consolidated into the case that reached the Supreme Court. The Learning Resources plaintiffs, two small businesses, sued in the United States District Court for the District of Columbia. The V.O.S. Selections plaintiffs, five small businesses and 12 states, sued in the United States Court of International Trade (CIT).

Learning Resources, an educational toy business in Illinois, faced a tariff bill of 4 million in 2025, prompting the company to sue the federal government over its use of IEEPA.

Both lower courts ruled against the government. The District Court granted the plaintiffs a preliminary injunction, concluding that IEEPA did not grant the President the power to impose tariffs. The Federal Circuit, sitting en banc, affirmed in relevant part, concluding that IEEPA's grant of authority to "regulate ... importation" did not authorize the challenged tariffs, which were "unbounded in scope, amount, and duration."

The Government filed a petition for certiorari and the Learning Resources plaintiffs filed a petition for certiorari before judgment. The Court granted the petitions and consolidated the cases. Oral arguments were heard on November 5, 2025. Court observers noted that a majority of the justices expressed skepticism towards the government's rationale during the oral session.

3. The Constitutional Foundation: Congress Holds the Purse

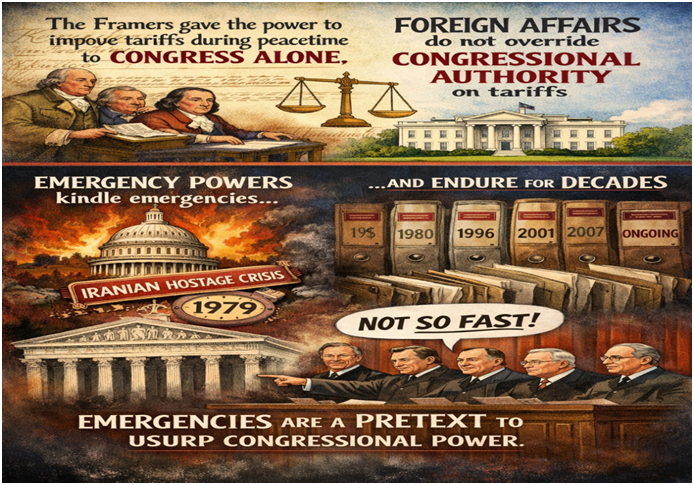

The majority opinion, authored by Chief Justice John Roberts, begins with the constitutional text. Article I, Section 8 specifies that "The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises." The Framers recognised the unique importance of this taxing power and gave Congress "alone ... access to the pockets of the people." They did not vest any part of the taxing power in the Executive Branch.

The power to impose tariffs is, as the Court put it, "very clearly ... a branch of the taxing power." A tariff is a tax levied on imported goods and services, and tariffs raise revenue -- the defining feature of a tax.

The government did not contest the basic constitutional allocation. It conceded that the President enjoys no inherent authority to impose tariffs during peacetime and did not defend the challenged tariffs as an exercise of warmaking powers. It relied exclusively on IEEPA.

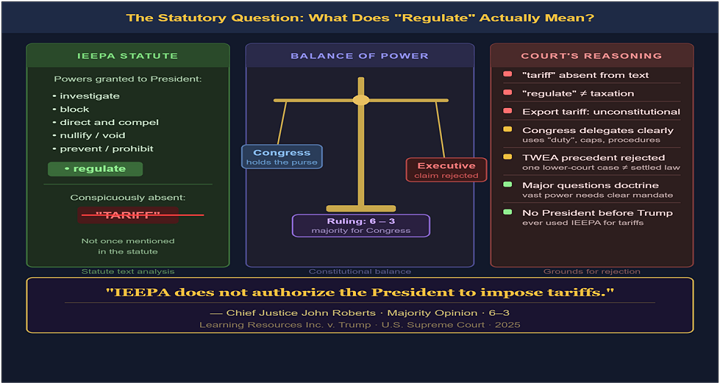

The Court was direct: the question before it was not a constitutional one but a statutory one. Did Congress, through IEEPA, validly delegate tariff-imposing power to the President? The answer, by six votes to three, was no.

4. The Statutory Question: What Does Regulate Actually Mean?

The government's entire case rested on two words in IEEPA, "regulate" and "importation", specifically the provision authorising the President to "regulate ... importation or exportation." The majority dismantled this argument on several grounds.

To begin with, the word "tariff" is simply absent from the statute. IEEPA authorises the President to "investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent or prohibit ... importation or exportation." Absent from this lengthy list is any mention of tariffs or duties. Had Congress intended to convey the power to impose tariffs, it would have done so expressly, as it consistently has in other tariff statutes.

The ordinary meaning of "regulate" does not encompass taxation. The term, as ordinarily used, means to "fix, establish, or control; to adjust by rule, method, or established mode; to direct by rule or restriction; to subject to governing principles or laws." The U.S. Code contains many statutes granting the Executive the authority to "regulate" someone or something, yet the Government cannot identify any statute in which the power to regulate includes the power to tax.

Reading "regulate" to include taxation would also create a constitutional problem. IEEPA authorises the President to "regulate ... importation or exportation," but taxing exports is expressly forbidden by the Constitution. A reading of IEEPA that grants a tariff power over imports would, by the same logic, grant a tariff power over exports.

When Congress has wanted to delegate tariff authority, it has done so in clear and bounded terms, using words like "duty," capping amounts and durations, and conditioning the tariff power on demanding procedural prerequisites such as International Trade Commission investigations and public hearings. IEEPA contains none of these features.

The government also argued that IEEPA's predecessor statute, the Trading with the Enemy Act (TWEA), had been interpreted to permit limited tariffs by a lower court in 1975, and that Congress imported that meaning into IEEPA. The Court rejected this. A single, expressly limited opinion from a specialised intermediate appellate court does not establish a well-settled meaning that Congress can be assumed to have incorporated into later legislation.

Practitioners seeking to understand how Congress delegates authority over intellectual property registration another domain where statutory language defines the precise scope of executive and administrative action may find value in the Trademark Filing Masterclass on LawyersClubIndia, which covers the procedural and statutory framework governing trademark applications in India.

5. The Major Questions Doctrine

Parts of the majority opinion, joined by Justices Gorsuch and Barrett but not the three liberal justices, went further and applied the "major questions doctrine." This doctrine holds that when an executive official claims a vast and consequential power on an ambiguous statutory basis, courts require clear congressional authorisation before accepting the claim.

The Court expressed reluctance to read into ambiguous statutory text extraordinary delegations of Congress's powers. Both separation of powers principles and a practical understanding of legislative intent suggest Congress would not have delegated highly consequential power through ambiguous language. These considerations apply with particular force where the purported delegation involves the core congressional power of the purse.

The historical record reinforced the point. In IEEPA's half century of existence, no President had invoked the statute to impose any tariffs, let alone tariffs of this magnitude and scope. Presidents had, by contrast, regularly invoked IEEPA for other purposes, and they had invoked other statutes, but never IEEPA, to impose tariffs.

The Government pointed to projections that the tariffs would reduce the national deficit by trillion and that international agreements reached in reliance on the tariffs could be worth 5 trillion. These stakes, the Court noted, dwarf those of other major questions cases. Precisely because the consequences were so large, Congress would need to have spoken clearly, and it had not.

The three liberal justices: Kagan, Sotomayor, and Jackson concurred in the outcome but not in the major questions analysis. Justice Kagan concluded that ordinary principles of statutory interpretation lead to the same result without requiring a special clear-statement rule. The government's arguments, she wrote, fail to satisfy even the normal test for statutory delegation.

Justice Gorsuch, in a lengthy concurrence, argued that the major questions doctrine is not a novel invention but a return to longstanding common law and constitutional principles requiring clear authorisation for exercises of extraordinary delegated power.

6. The Dissent

Justices Thomas, Alito, and Kavanaugh dissented. Justice Kavanaugh wrote the principal dissenting opinion, joined by Thomas and Alito. Justice Thomas also filed a separate dissent.

The dissenters argued that the foreign affairs and national security dimensions of tariff policy warranted a different interpretive approach, one more deferential to the executive. The majority answered this directly. The Framers gave the power to impose tariffs during peacetime to Congress alone, notwithstanding the obvious foreign affairs implications of tariffs. The foreign affairs character of tariff policy does not make it more likely that Congress would relinquish its tariff power through vague language or without careful limits.

The majority also rejected the government's argument that emergency statutes deserve more interpretive latitude. Emergency powers tend to kindle emergencies. Dozens of IEEPA emergencies remain ongoing today, including the first, declared over four decades ago in response to the Iranian hostage crisis. Emergencies can, the Court noted, afford a ready pretext for the usurpation of congressional power.

7. What the Ruling Does and Does Not Cover

The decision's scope is significant but not unlimited. The Court invalidated all tariffs imposed under IEEPA, including the reciprocal tariff regime imposed on goods from almost all countries and the tariffs imposed in response to the fentanyl crisis. The decision has no impact on tariffs imposed under Section 301 of the Trade Act of 1974 or those imposed under Section 232 of the Trade Expansion Act of 1962, which include the tariffs on steel, aluminum, copper, automobiles, auto parts, lumber, and semiconductors.

The ruling also opened a refund question. Penn-Wharton Budget Model economists estimated that IEEPA-based tariff collections totalled approximately 75 billion to 79 billion. Companies that paid IEEPA-based duties have legal rights to seek refunds through existing U.S. Customs and Border Protection administrative processes. The Court itself, however, did not address how refunds should be managed in practice.

8. Aftermath: The Administration's Response

The administration moved quickly. The day after the Supreme Court ruling, Trump promised to set new global tariffs under Section 122 of the Trade Act of 1974, capped at 15%. Section 122 allows the President to set such universal tariffs, limited to 150 days and requiring congressional approval for extension, to deal with serious balance-of-payments deficits.

Within hours of the decision, Trump signed a proclamation imposing a new 10% global tariff under Section 122, effective February 24, 2026, and announced his intention to increase it to 15% shortly after.

Those tariffs have already drawn further legal challenge. Multiple legal and economic experts argue that the Section 122 tariffs are also on shaky ground because the balance-of-payments deficit required by that provision does not exist, in part because the U.S. exports more services than goods. Twenty-four states filed a lawsuit challenging the Section 122 tariffs in March 2026.

The broader significance of the decision extends beyond any one statute. The Court reasserted that the power of the purse belongs to Congress, that emergency declarations do not transform ambiguous statutory language into sweeping grants of authority, and that no President before Trump had ever read IEEPA to permit tariffs at all. As the majority stated plainly: "IEEPA does not authorize the President to impose tariffs."

Legal professionals navigating the intersection of trade regulation and intellectual property protection may also benefit from the masterclass on LawyersClubIndia, a practical guide to protecting brand assets through the Indian trademark registration process.

9. FAQs

Q. Does this ruling mean all of Trump's tariffs are now illegal?

No. The ruling specifically struck down tariffs imposed under IEEPA. Tariffs imposed under other statutes: Section 232 of the Trade Expansion Act of 1962, covering steel, aluminium, and automobiles, and Section 301 of the Trade Act of 1974 remain in force. The Trump administration has also imposed new tariffs under Section 122 of the Trade Act of 1974, though those face fresh legal challenges. The ruling's reach is significant, but it does not wipe out the administration's entire tariff structure.

Q. Can businesses get refunds for IEEPA tariffs they already paid?

Potentially yes, though the path is not straightforward. The Court did not specify a refund mechanism. Businesses that paid IEEPA-based duties can file protests through U.S. Customs and Border Protection administrative processes. Estimates put total IEEPA tariff collections between 66 billion and 79 billion. The administration has signalled resistance to large-scale refunds, and litigation over the refund process is likely to continue for some time.

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others