In today's article we shall be discussing per incuriam cases in the tax domain. "Per incuriam" literally means "through lack of care". A per incuriam case is one which has ignored established judicial precedents, or statutory law and has hence laid down incorrect law. Ajudicial pronouncement is not a binding precedent if given per incuriam, i.e., it is either:

- A judgment that is passed in ignorance of a relevant statutory provision; or

- A judgment that is passed without taking into consideration any precedent of a coordinate or larger bench.

A judgment which has been held to be per incuriam does not then have to be followed as a binding precedent by a lower court.

Let's look at a few per incuriam cases along with the cases which have held them to be per incuriam.

Per Incuriam Case:

Vazir Sultan Tobacco Co. Ltd. vs Commissioner Of Income Tax | Andhra Pradesh High Court

"Whether on the facts and in the circumstances of this case, the assessee was entitled to a deduction of the expenditure incurred for raising additional capital by issue of bonus shares to the existing shareholders of the company?

Court's Answer: No. The court held that the expenditure incurred for raising additional capital by means of issuing bonus shares would be attributable to enlarging of the capital base of the company and thus, such expenditure would be capital in nature.

Held Per Incuriam in:

Commissioner Of Income Tax, Mumbai vs M-s. General Insurance Corporation of India | Supreme Court

"Whether on the facts and in circumstances of the case and in law the Tribunal was right in holding that the expenditure incurred on account of share issue is an allowable expenditure?"

Court's Answer: The Court decided that issuing of bonus shares by way of capitalization of reserves would merely be a relocation of the company's funds. It could not be said that there wasany inflow of fresh funds or increase in the capital employed.

Per Incuriam Case:

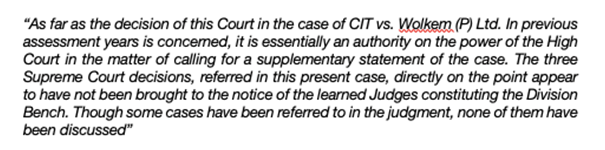

Commissioner Of Income Tax vs WolkemPvt. Ltd | HC Rajasthan

"Whether, on the facts and in the circumstances, the Tribunal was right in law in holding that refund of excise duty was not in the nature of income under s. 28(iv) or under s. 41(1) of the IT Act, 1961"

Court's Answer: The High Court ruled that refund of excise duty could not be said to be the income of the assessee. Since the same was held to not be income, it was covered by neither Section 28(iv) nor Section 41 of the Income Tax Act. Thus, it would not be considered as a revenue receipt. Hence, it was held that there would be no income tax liability as the refund amounted to only a financial transaction and nothing beyond.

Held Per Incuriam in:

Wolkem (P) Ltd. vs Commissioner Of Income Tax | HC Rajasthan

"Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in holding that the excise duty collection was a trading receipt in the year of receipt and hence excise duty refund of Rs. 1,45,752 was liable to tax in the hands of the assessee under s. 41(1) of the IT Act, 1961?"

Court's Answer: The High Court considered the refund as income for the assessee since the amount refunded was neither diverted to the customers nor paid to the Government. The court opined that this would be a case of unlawful enrichmentIf the refund were not considered as income as the assessee will have benefitted twice.

Per Incuriam Case:

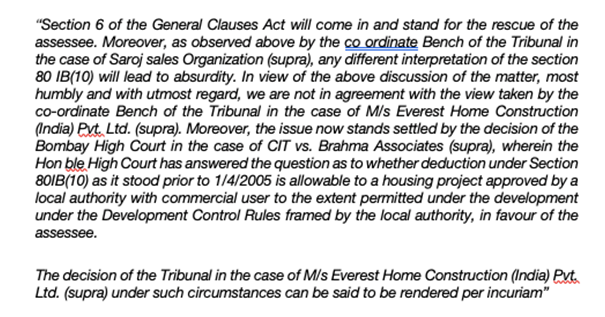

ITO vs Everest Home Construction (I) P. Ltd | ITAT Mumbai

"Whether on the facts and in the circumstances of the case, the CIT(A) erred in directing the Assessing Officer to allow deduction under section 80IB(10) even though condition laid down in the section 80IB(10)(d) is not satisfied which is applicable from A.Y. 2005-06 onwards

Court's Answer: The Tribunal denied the benefit of section 80IB(10)

Held Per Incuriam in:

ACIT vs Poonam GruhNirman | ITAT Mumbai

"Whether on the facts and in the circumstances of the case in law, the CIT(A) has erred in holding that the assessee is entitled to deduction under section 80IB(10)?"

Court's Answer: It is important to note that there are a plethora of judgments of the co-ordinate Benches of the Tribunal wherein it has been held that the law under the substituted provisions of section 80IB(10) of the Act would not be applicable for projects which had already been approved by the local authority prior to the amendment.

Written by Saili Kulkarni, Product Manager @ Riverus

About Riverus:

We are a legal tech firm that works at the intersection of law and technology. The Riverus Strategic Income Tax Research Tool offers you access to the largest income tax law database along with unprecedented insights from data analytics that help you accomplish your research more quickly and efficiently. We also offer data driven bespoke services for those problems that vex you to no end. Reach out to us at hello@riverus to know more!

Join LAWyersClubIndia's network for daily News Updates, Judgment Summaries, Articles, Forum Threads, Online Law Courses, and MUCH MORE!!"

Tags :Others